Can you think about the last time you sent money internationally.

You filled out a form, handed over your cash (or clicked through a dozen screens), and then watched a chunk disappear into a fog of wire fees, exchange rate markups, and correspondent bank charges you never agreed to.

The World Bank confirmed this is not your imagination: traditional remittance fees still average 6.49% of every transaction.

Crypto remittances flip this entirely. By routing value directly, peer-to-peer, over blockchain networks using stablecoins like USDT and USDC, you can move money across any border in minutes for a fraction of a percent.

Join UEEx

Experience the World’s Leading Digital Wealth Management Platform

This guide explains exactly how it works in 2026, which tools to use, what the compliance landscape looks like, and why over 1 million users across 110 countries are now doing this through platforms like UEEX.

Crypto Remittances and How Do They Actually Work?

Crypto remittances are cross-border money transfers that use digital assets primarily stablecoins like USDT and USDC instead of traditional banking rails.

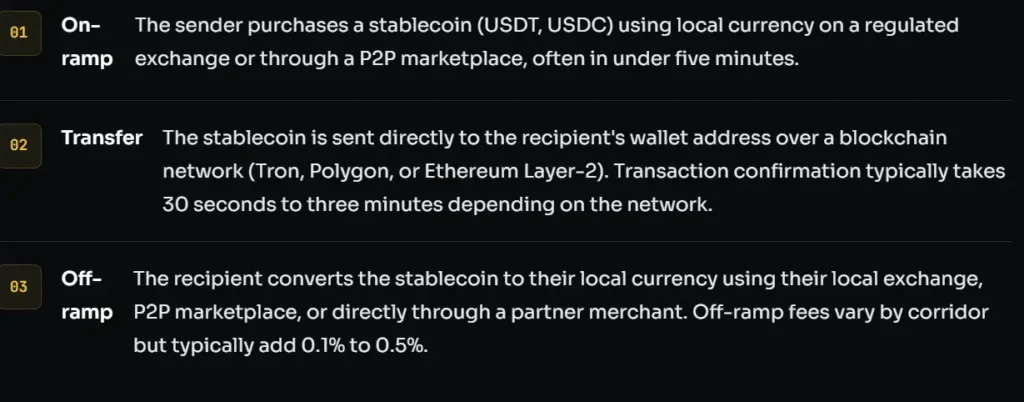

The sender converts local currency to a stablecoin, transfers it to the recipient’s wallet in seconds via a blockchain network, and the recipient converts it back to local currency.

No correspondent banks. No multi-day clearing. No hidden markups.

The traditional model for sending money abroad looks like this: your bank contacts a correspondent bank in an intermediary country, which contacts another correspondent bank in the destination country, which finally reaches the recipient’s local bank.

Each of these intermediaries takes a cut and adds settlement time. A standard international wire can take two to five business days.

The crypto remittance model eliminates the chain. Here is the actual flow:

How Much Cheaper Are Crypto Remittances Than Bank Transfers?

Traditional wire transfers average 6.49% in fees, according to the World Bank. Crypto stablecoin transfers particularly USDT on Layer-2 networks like Tron or Polygon compress those costs to under 1%.

On a $500 transfer, that is the difference between paying $32.45 to a bank versus paying under $5 to a blockchain network.

Numbers are more persuasive than percentages. Here is a real-world comparison for a $500 USD transfer across six of the highest-volume remittance corridors in 2026:

Transfer Method

Avg. Fee (%)

Fee on $500

Transfer Time

Exchange Rate Markup

Speed Rating

Traditional bank wire

6.49%

$32.45

2–5 business days

1–3% hidden

Western Union / MoneyGram

4.5–7%

$22–35

Minutes to 3 days

1–2.5% hidden

PayPal international

4–5%

$20–25

1–3 days to bank

2.5–3% hidden

USDT via Tron (TRC-20)

~0.02%

$0.10

30 seconds to 2 min

0% (stablecoin)

USDC via Polygon

~0.1%

$0.50

1–3 minutes

0% (stablecoin)

Marketplace

0–0.2%

$0–1.00

Under 5 minutes

Market rate

The math is not subtle. If you send money home monthly, switching from bank wires to USDT on Tron can save you over $380 a year on a $500/month habit.

That is money staying in your family’s hands instead of enriching a correspondent banking chain.

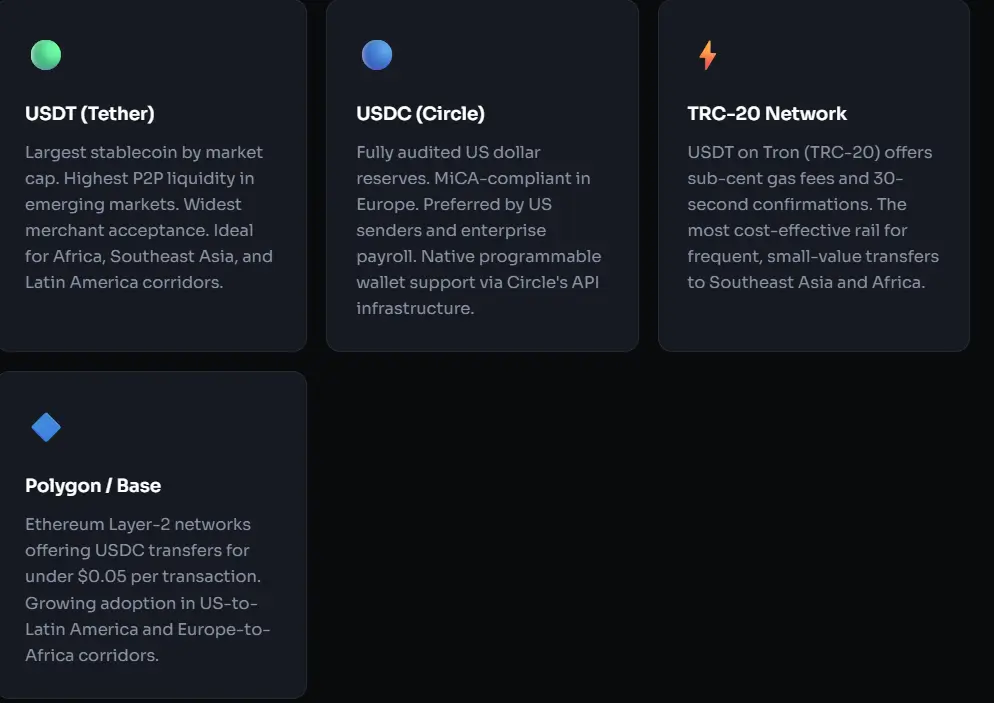

Why Are USDT and USDC the 2026 Remittance Standard?

USDT (Tether) and USDC (Circle) have become the primary rails for crypto remittances in 2026 because they eliminate price volatility, operate across multiple blockchains, and carry stablecoin market caps that exceeded $300 billion in early 2026.

Over 85% of all digital cross-border transfers now use stablecoins, up from under 60% in 2023.

Stablecoins are the practical solution to crypto’s biggest remittance problem: price volatility. Nobody wants to send $500 and have it arrive worth $420 because the market dipped.

USDT and USDC solve this by maintaining a 1:1 peg to the US dollar through a combination of cash reserves, treasury bills, and on-chain collateral.

What Is the Difference Between USDT and USDC for Remittances?

USDT (Tether) has higher global liquidity and dominates emerging market P2P corridors particularly in Africa, Southeast Asia, and Latin America making it easier to off-ramp to local currency.

USDC (Circle) offers stronger regulatory compliance, full US dollar reserve auditing, and is the preferred choice for US-based senders and business payroll transfers.

How Do Layer-2 Networks Lower Your Fees Even Further?

Layer-2 (L2) networks are scaling solutions built on top of Ethereum that bundle thousands of transactions together before settling them on the main chain.

This reduces per-transaction gas fees from the $5–$25 range seen on Ethereum mainnet to under $0.05, making micro-remittances economically viable for the first time.

If you have ever tried to send USDC on Ethereum’s main network (Layer-1), you will have been shocked by gas fees that sometimes exceed the amount you are sending. Layer-2 scaling is the fix.

These networks process transactions off the main chain in batches, dramatically reducing the computational overhead per transaction.

For remittance purposes, the practical result is this: sending $50 USDC from the UK to the Philippines over Polygon costs under $0.05 in network fees.

The same transaction on Ethereum mainnet could cost $8–$20 depending on network congestion. Layer-2 makes crypto remittances viable at any amount, including the small, frequent transfers that most migrant workers actually send.

Should You Use P2P or a Crypto Exchange for Remittances?

P2P (peer-to-peer) marketplaces let you buy or sell crypto directly with another person using local payment methods — bank transfer, mobile money, or cash often at better rates than an exchange.

They are the preferred choice in corridors where banking access is limited, where local payment methods dominate, or where the recipient does not have a crypto wallet and needs to receive local currency directly from a P2P merchant.

Both methods work. The right choice depends on your corridor and the recipient’s situation.

A centralized exchange is the better path when both sender and recipient are crypto-comfortable, both have verified accounts on the same or compatible platforms, and the corridor has deep liquidity.

The experience is closest to a traditional bank transfer in terms of UX familiarity.

A P2P marketplace shines in corridors where recipients are unbanked or underbanked, where mobile money (M-Pesa, GCash, bKash) dominates the last mile, or where local bank infrastructure makes receiving international wires slow or expensive.

P2P merchants operate like local agents, they hold a USDT balance, receive your crypto, and release local currency to the recipient via the payment method that works best in their market.

How Do I Send a Crypto Remittance Step by Step?

1. Create and verify your UEEX account

Complete KYC verification (government ID plus a selfie). This typically takes 5–10 minutes for standard verification. KYC is required for VASP compliance and protects both you and the recipient.

2. Deposit or buy stablecoin

Fund your UEEX account via bank transfer, card, or use the P2P marketplace to buy USDT directly with local currency. For regular senders, a bank transfer is usually the cheapest on-ramp.

3. Choose your transfer method

Use UEEX Crypto Remittance for a guided wallet-to-wallet flow, or navigate to the P2P Marketplace if the recipient needs cash or mobile money in their local currency.

4. Select the optimal network

For most corridors involving Southeast Asia, Africa, or the Middle East, TRC-20 (USDT on Tron) offers the lowest fees.

For Europe and North America, Polygon or Base (USDC) may be preferred. UEEX recommends the optimal network automatically

5. Confirm and track

Enter the recipient’s wallet address, double-check the first four and last four characters, and confirm. You can track confirmation status in real time. Most transfers confirm within 60–180 seconds.

Are Crypto Remittances Safe, Legal, and VASP-Compliant in 2026?

Yes, when conducted through a regulated Virtual Asset Service Provider (VASP).

In 2026, regulatory frameworks including the EU’s MiCA regulation, FATF Travel Rule requirements, and equivalent legislation in the UK, UAE, and Singapore require crypto exchanges to apply KYC and AML checks identical to those of traditional banks.

The regulatory landscape for crypto remittances clarified enormously between 2023 and 2025.

The EU’s Markets in Crypto-Assets (MiCA) framework fully enforced since late 2024 established clear licensing requirements for crypto service providers operating in Europe.

The FATF Travel Rule, adopted across G20 jurisdictions, requires platforms to collect and transmit sender and recipient information for transfers above $1,000 USD equivalent.

For you as a sender, this means two things: legitimate platforms will ask for your identity documents (which is a good sign, not a red flag), and your transfers carry the same legal protections as regulated financial services.

Platforms operating outside these frameworks offer no such protection.

The majority of user funds held offline in hardware wallets, inaccessible to online attackers. Industry standard is 95%+ cold, 5% or less hot for liquidity.

2. Proof-of-Reserves

On-chain cryptographic proof that the platform holds 1:1 assets against all user balances, published and independently verifiable in real time.

3. Asset Vault Segregation

User funds held in an independent vault, legally and operationally separate from the company’s operating capital. Your money does not fund their business expenses.

3. Multi-Level Verification

Anti-phishing codes, hardware key support, withdrawal address whitelisting, and biometric confirmation for large transfers.

The Intersection of Remittance and Cryptocurrency

Cryptocurrency has the potential to change the remittance industry by offering faster, cheaper, and more secure transactions.

Additionally, cryptocurrency can provide financial inclusion to underserved populations by eliminating the need for traditional bank accounts.

One striking example of how cryptocurrency is being used for remittances is in El Salvador. El Salvador became the first country in the world to adopt Bitcoin as legal tender in September 2021.

Since then, cryptocurrency remittances to El Salvador have increased significantly. Cryptocurrency remittances to El Salvador totalled $42 million in 2021, up from just $1.5 million in 2020.

Join UEEx

Experience the World’s Leading Digital Wealth Management Platform

The increase in cryptocurrency remittances to El Salvador has had a positive impact on the country’s economy. It has helped to reduce the cost of remittances, and it has also boosted economic activity.

How Does UEEX Make Crypto Remittances Faster and Cheaper?

1. Log in to UEEX

Navigate to the Remittance or P2P Marketplace section. If the recipient needs local currency, filter P2P merchants by GCash or bank transfer, two of the most widely used payout methods in the Philippines.

2. Initiate the transfer

Enter $400 USDT. The platform suggests TRC-20 network based on real-time gas analysis — fee displayed clearly as $0.10 before you confirm

3. Funds delivered

The recipient receives a GCash notification or bank credit within three to seven minutes. No correspondent banks. No two-day wait. No hidden currency markup.

Beyond remittances, UEEX users often grow into the platform’s broader financial ecosystem: Spot Trading, Futures with up to 125x leverage for experienced traders, Copy Trading to mirror top performers, and UEEX Savings for passive yield on stablecoin balances between transfers.

Many users arrive for the remittance and stay for the financial tools that most banks simply do not offer.

Join UEEx

Experience the World’s Leading Digital Wealth Management Platform

Cryptocurrency has emerged as a compelling alternative to traditional remittance methods, offering a host of advantages for both senders and recipients.

Cost Reduction

One of the most significant benefits of using cryptocurrency for remittances is the potential for substantial cost savings

Lower transaction fees: Unlike traditional remittance services that often impose hefty fees, cryptocurrency transactions typically involve significantly lower costs. This allows more of the sent money to reach the recipient.

Elimination of intermediaries: Cryptocurrency transactions are peer-to-peer, bypassing the need for banks or other financial institutions. This cuts out intermediary fees and reduces overall costs.

Speed and Efficiency

Cryptocurrency transactions are renowned for their speed and efficiency compared to traditional remittance methods.

Faster transaction processing: Crypto transactions can be processed within minutes or even seconds, drastically reducing waiting times for recipients. This is particularly beneficial for time-sensitive transfers.

Real-time tracking: Blockchain technology enables real-time tracking of cryptocurrency transactions, providing transparency and peace of mind for both senders and recipients.

Accessibility and Inclusion

Cryptocurrency has the potential to revolutionize financial inclusion by expanding access to remittance services.

Unbanked and underbanked populations: Millions of people worldwide lack access to traditional banking services. Cryptocurrency offers a viable alternative, allowing them to send and receive money without the need for a bank account.

Global reach: Cryptocurrency transcends geographical boundaries, enabling remittances to be sent and received virtually anywhere in the world with an internet connection. This is particularly beneficial for migrant workers sending money home to their families.

Transparency and Security

Cryptocurrency leverages blockchain technology to provide a high degree of transparency and security.

Blockchain technology and immutability: Transactions are recorded on an immutable blockchain, creating a transparent and auditable record. This reduces the risk of errors, fraud, and disputes.

Reduced fraud risk: The decentralized nature of cryptocurrency and the use of cryptographic techniques make it significantly more difficult for fraudsters to manipulate transactions or steal funds.

Cryptocurrency is rewriting the remittance rulebook. By slashing costs, accelerating transfers, and expanding financial access, it’s poised to revolutionize how we send money across borders.

While challenges like volatility and regulation persist, the potential benefits are undeniable. As the digital market expands, cryptocurrency’s role in remittances is a story far from over.

Hello, welcome to my Profile. I am a passionate content writer, copywriter and fiction writer. I have a zeal to always deliver engaging and high quality content. I’ve perfected the art of blending imaginative thoughts with relatable themes crafting stories that captivates and connects with various audiences.

Disclaimer: This article is intended solely for informational purposes and should not be considered trading or investment advice. Nothing herein should be construed as financial, legal, or tax advice. Trading or investing in cryptocurrencies carries a considerable risk of financial loss. Always conduct due diligence before making any trading or investment decisions.