“Crypto Is for Money Laundering”. This is a common misconception surrounding cryptocurrency.

Money laundering happens in almost all financial settings, a stain on every economic system. However, this criminal activity doesn’t define those systems entirely. The same holds for cryptocurrency, too.

While concerns that crypto is for money laundering keep growing, it’s important to separate fact from fiction.

Despite being a new way to handle money, there are worries about its misuse. This article will look at these concerns and explain the truth about how cryptocurrency is used.

Key Takeaways

Money laundering concerns cryptocurrency, but it’s not its defining feature.

Despite decreased illicit activity, criminals find new methods to launder money through cryptocurrency.

Crypto transactions are pseudonymous, not anonymous, leaving a public record that can be traced with the right tools.

Regulations like KYC and AML are implemented to improve transparency and combat money laundering.

International cooperation, standardized regulations, and technological advancements are crucial for combating cryptocurrency money laundering effectively.

Cryptocurrency in Money Laundering

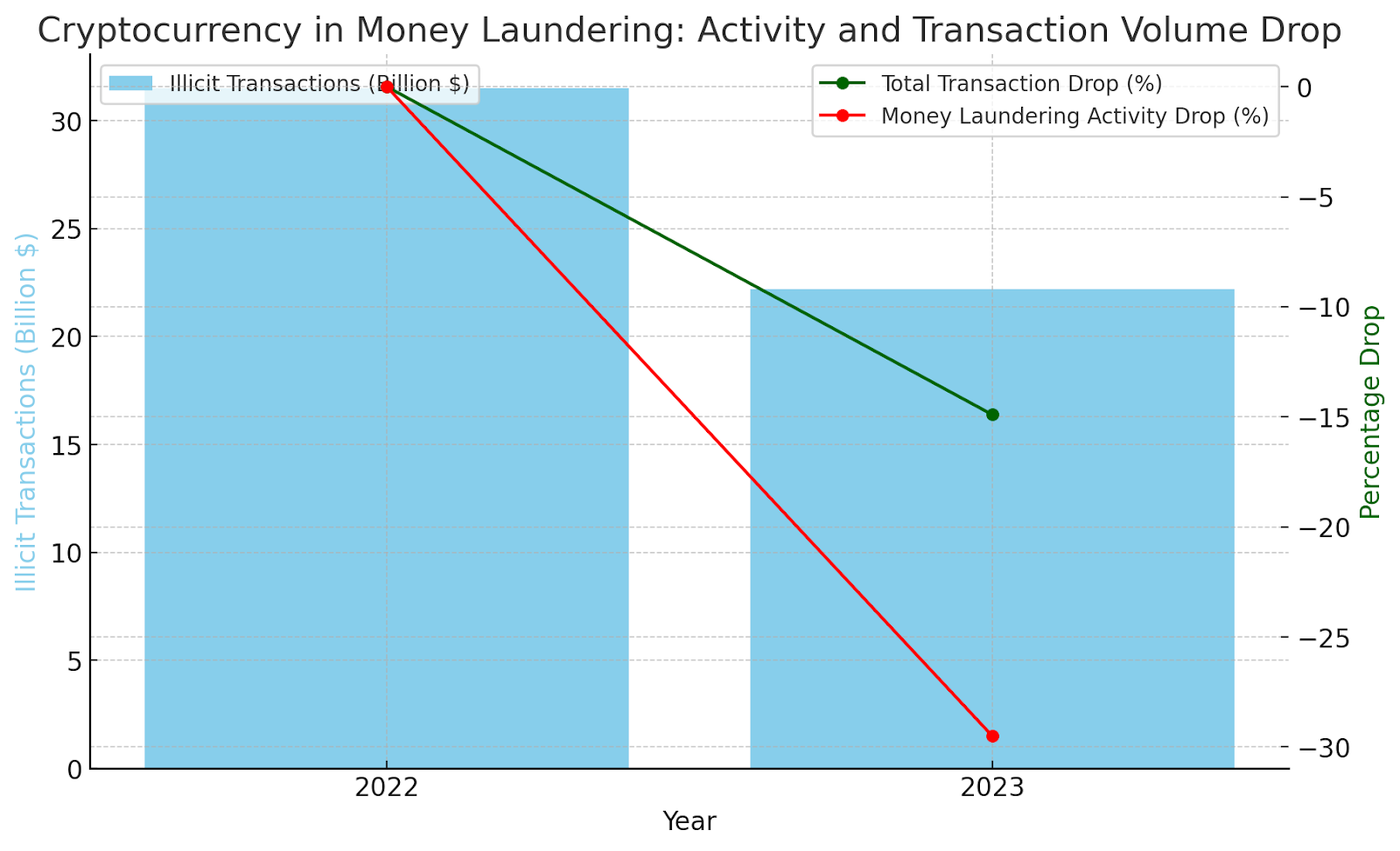

In 2023, cryptocurrency use in money laundering significantly decreased. The amount of illicit crypto transactions dropped to $22.2 billion from $31.5 billion the previous year.

This reduction was sharper than the overall decrease in crypto transactions, suggesting that efforts to hide illegal activities might improve.

Despite this general decline, there’s been a noticeable shift towards using gambling services and bridge protocols for laundering, indicating criminals are exploring new methods to avoid detection.

Additionally, the role of DeFi (Decentralized Finance) in these activities has grown due to the sector’s expansion, even though its transparency typically makes hiding transactions difficult.

High-profile legal cases have also underscored the seriousness of cryptocurrency in money laundering. Actions against individuals like Sam Bankman-Fried, the founder of FTX, for fraud and money laundering, and Nate Chastain from OpenSea, in a landmark insider trading case involving digital assets, highlight the increasing legal scrutiny and challenges in combating cryptocurrency-related crimes.

Join UEEx

Experience the World’s Leading Digital Wealth Management Platform

Anonymity and Privacy in Cryptocurrency Transactions

Cryptocurrency transactions offer pseudonymity, not complete anonymity. Here’s why:

Public Ledger: Blockchains, the technology behind most cryptocurrencies, are public ledgers. Every transaction is recorded, showing the movement of coins from one address to another.

Crypto Addresses: These addresses are like account numbers but aren’t linked to real-world identities. Anyone can see the balance and transactions associated with an address, but they can’t necessarily identify the person behind it.

However, this pseudo-anonymity is precisely what makes cryptocurrency attractive for money laundering. Criminals can leverage the disconnect between addresses and identities to obfuscate the flow of stolen funds.

Splitting ill-gotten gains into smaller amounts and transferring them through a chain of multiple addresses can make it significantly harder for investigators to track the money’s source and ultimate destination.

This creates a tangled web of transactions that can be difficult to unwind, potentially delaying or even derailing attempts to recover stolen funds and hold criminals accountable.

Regulatory Efforts

In response to the money laundering risks posed by cryptocurrency’s pseudo-anonymity, governments and regulatory bodies are taking a multi-pronged approach.

KYC regulations require cryptocurrency exchanges and other Virtual Asset Service Providers (VASPs) to verify customers’ identities.

This typically involves collecting personal information like name, address, and ID proof. By establishing who’s behind each crypto address, authorities can gain crucial insights into transaction flows and identify suspicious activity.

AML regulations are built on KYC. These rules require VASPs to monitor customer transactions for red flags that might indicate money laundering.

This includes watching for large, unexplained deposits or frequent transfers of small amounts – tactics commonly used by criminals to disguise the origin and destination of funds. VASPs are also obligated to report suspicious activity to authorities, aiding investigations and helping to disrupt money laundering schemes.

Financial institutions also play a part. By working with regulators and VASPs, they can share information on suspicious individuals or activity. This collaboration helps to create a broader, more comprehensive picture of potential money laundering networks.

Cryptocurrency’s Potential for Legitimate Use

While cryptocurrencies have garnered attention for their role in some illegal activities like money laundering, it’s important to recognize their potential for legitimate use cases that can benefit individuals and industries. One key area is financial inclusion.

Join UEEx

Experience the World’s Leading Digital Wealth Management Platform

Globally, billions of people lack access to traditional banking systems. Cryptocurrency offers an alternative. Anyone with a smartphone and internet access can set up a digital wallet to store and transfer cryptocurrencies.

This empowers the unbanked to participate in the global financial system, facilitating remittances, online payments, and even microloans.

For instance, Abra, a mobile-based cryptocurrency wallet, allows users in emerging economies like the Philippines to send and receive money internationally with lower fees than traditional money transfer services.

Revolutionizing Industries with Blockchain

Blockchain, the underlying technology behind cryptocurrencies, offers a secure and transparent way to record data. This has the potential to revolutionize various industries:

Supply Chain Management

Blockchain can track the movement of goods from origin to destination, ensuring authenticity and eliminating counterfeit products.

Walmart, for example, is using blockchain to track the authenticity of its food products through its supply chain, improving transparency and ensuring food safety.

Beyond food, companies like De Beers are using blockchain to track diamonds throughout the supply chain, ensuring ethical sourcing and preventing conflict diamonds from entering the market.

Healthcare

Blockchain can securely store and manage medical records, allowing patients to control access and share information easily with healthcare providers. This can improve efficiency and accuracy in the healthcare system.

Blockchain technology offers the potential for secure and transparent voting systems. By creating an immutable record of votes, blockchain can reduce the risk of fraud and manipulation.

While still in its early stages, countries like West Virginia have piloted blockchain voting systems in local elections.

Content Creation and Copyright Protection

For creators like artists and musicians, cryptocurrency allows for direct monetization of their work.

Platforms built on blockchain technology can automatically distribute royalties to creators whenever their work is used, eliminating the need for intermediaries and ensuring fair compensation.

Cryptocurrency’s potential for anonymity and rapid transactions presents significant challenges for regulators and law enforcement agencies trying to combat money laundering. Here are the key issues and potential solutions:

While not completely anonymous, cryptocurrency transactions are often linked to pseudonymous addresses, making it difficult to identify the individuals or entities behind them. Criminals can leverage this pseudonymity to obfuscate the origin and destination of funds.

Borderless Transactions

The global nature of cryptocurrency allows criminals to easily move funds across borders, evading regulations in specific jurisdictions with stricter AML/KYC requirements. This creates a complex environment for international cooperation and tracking illicit activity.

Solutions

Combining these solutions can create a more robust system for combating cryptocurrency-related money laundering.

International Collaboration

Effective regulation hinges on international cooperation among governments and financial institutions. The Financial Action Task Force (FATF) establishes international standards.

FATF has issued guidelines for regulating cryptocurrency exchanges, requiring them to implement Anti-Money Laundering (AML) and Know Your Customer (KYC) procedures.

These guidelines aim to establish a global baseline for combating money laundering in the cryptocurrency space.

Standardized Regulations

Standardizing AML and KYC regulations across different countries is critical. Currently, varying regulations create a patchwork system that criminals can exploit.

By implementing consistent AML/KYC standards, loopholes in specific jurisdictions can be closed, making it significantly more difficult for criminals to launder money through the cryptocurrency system.

Technological Advancements

Blockchain analysis tools are emerging as powerful weapons in the fight against cryptocurrency money laundering.

These tools can analyze vast amounts of blockchain data to identify suspicious transaction patterns associated with money laundering activities.

For instance, companies like Chainalysis offer software that helps trace cryptocurrency transactions, flag unusual activity, and identify potential money laundering attempts. Using these tools, law enforcement can track illicit funds and disrupt criminal operations.

Join UEEx

Experience the World’s Leading Digital Wealth Management Platform

Collaboration between public authorities and private companies in the cryptocurrency space is essential.

Law enforcement agencies can benefit from the expertise of blockchain analysts and cryptocurrency firms to develop more effective strategies for identifying and combating money laundering.

Open communication and information sharing can create a more robust environment for cryptocurrency transactions.

Public Perception and Education

Cryptocurrency is often viewed negatively because it’s sometimes used for money laundering. This is due to its digital nature and the anonymity it can provide.

However, it’s crucial to understand that cryptocurrencies have many legitimate uses. They offer fast, efficient, and secure transactions for users worldwide, making them an important innovation in financial technology.

Educating the public about these legitimate uses is essential. People need to know that cryptocurrencies are not just tools for illegal activities but have genuine, beneficial applications.

These include enabling remittances, providing financial services to those without access to traditional banking, and facilitating secure and transparent transactions.

Several initiatives and campaigns are working towards changing the public’s perception of cryptocurrencies.

These efforts focus on promoting the responsible use of digital currencies, highlighting their potential benefits, and educating users on how to use them safely.

For example, blockchain companies and crypto exchanges often hold educational seminars, publish informative content, and support research exploring cryptocurrency’s positive aspects.

Additionally, some organizations collaborate with regulators to develop guidelines that ensure the safe use of cryptocurrencies, aiming to build trust among the public and encourage its adoption for legitimate purposes.

Conclusion

So, for the statement “Crypto is for money laundering,” the answer is NO. While cryptocurrencies can be misused for illegal activities, they also hold immense potential for legitimate purposes.

By implementing stricter regulations, fostering international cooperation, and leveraging technological advancements, we can create a more secure and transparent environment for cryptocurrency transactions.

By focusing on education and responsible use, we can unlock this technology’s potential for financial inclusion, innovation, and a more efficient global financial system.

Join UEEx

Experience the World’s Leading Digital Wealth Management Platform

Orebiyi Eniola is a writer whose soul work is content marketing with a focus on the cryptocurrency industry. Equipped as a marketing storyteller and driven by a passion for crafting impactful stories, she helps businesses connect with their audiences via strategic and thought-provoking writing. Orebiyi assists businesses in projecting their stories and actualizing their ambitions through the force of words. She likes to settle in with her favorite fiction novels when not pounding on her keyboard.

Disclaimer: This article is intended solely for informational purposes and should not be considered trading or investment advice. Nothing herein should be construed as financial, legal, or tax advice. Trading or investing in cryptocurrencies carries a considerable risk of financial loss. Always conduct due diligence before making any trading or investment decisions.