In March 2024, Nigerian authorities filed four charges of tax evasion against the cryptocurrency exchange Binance. To further intensify the investigation, they sought Interpol’s cooperation to apprehend a company official who managed to escape custody.

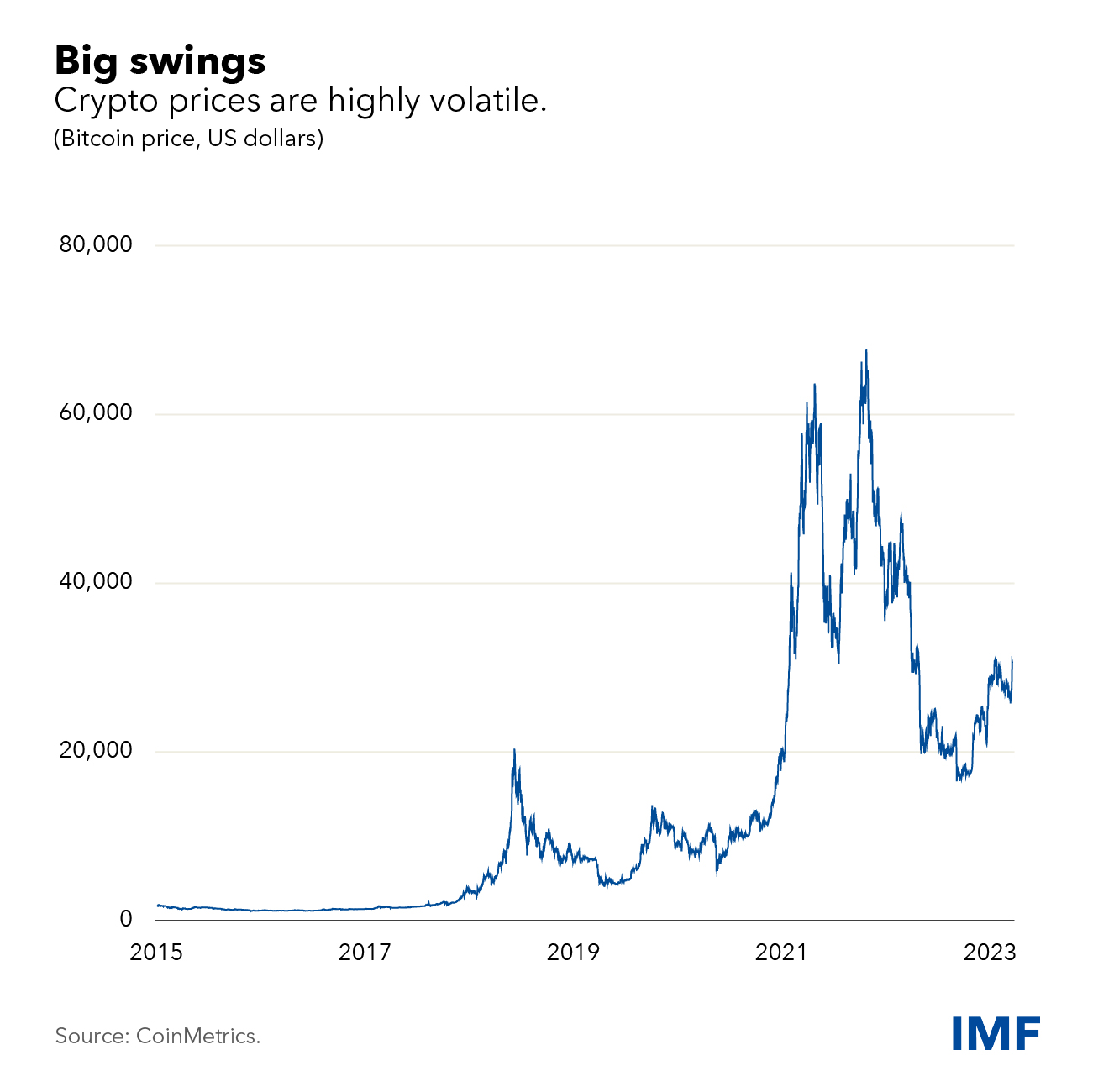

Cryptocurrency has revolutionized finance, offering new avenues for investment, transactions, and financial inclusion.

However, this innovation presents a unique challenge for traditional tax systems. Features that empower cryptocurrency, like anonymity, decentralization, and borderless transactions, can also be exploited for tax evasion.

Explore the intricate link between cryptocurrency and tax evasion.

Key Takeaways

- Cryptocurrencies pose challenges for tax authorities because decentralization and anonymity features can be exploited for tax evasion.

- Common crypto tax evasion techniques include using anonymity services, unregulated exchanges, and exploiting loopholes in tax regulations across different countries.

- Governments are implementing regulations and collaborating with crypto exchanges to curb crypto tax evasion. Blockchain technology also offers secure and transparent record-keeping solutions and potentially automated tax reporting.

- Crypto users can contribute to a more transparent ecosystem by keeping accurate records, utilizing crypto tax tools, and seeking professional guidance.

Cryptocurrency and the Challenge of Tax Evasion

The emergence of cryptocurrency has disrupted traditional financial systems and presents both exciting opportunities and significant challenges for tax authorities.

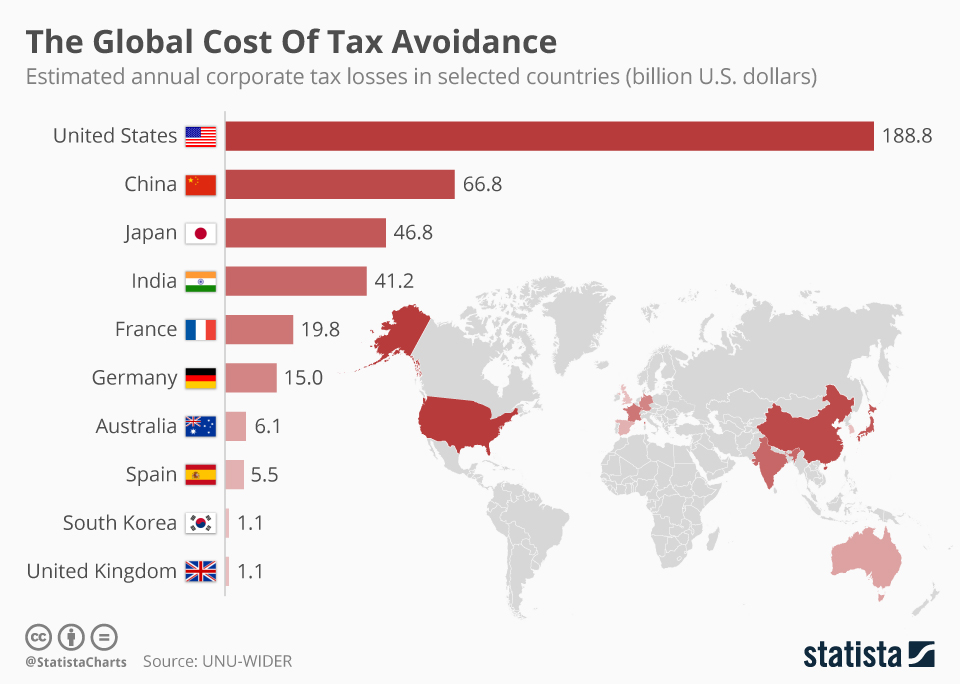

A report from 2022 suggests that the Internal Revenue Service (IRS) might be losing out on a substantial amount of tax revenue due to crypto traders not fulfilling their tax obligations. The report estimates that the IRS could be missing out on over $50 billion annually as a result of this issue.

Cryptocurrency, often referred to as “crypto,” is a digital asset designed to work as a medium of exchange. Unlike traditional currencies, it operates on a decentralized ledger called a blockchain, eliminating the need for a central bank or intermediary.

Benefits of Decentralization

This decentralized nature offers several benefits, including:

- Security: Transactions are cryptographically secured, making them highly resistant to fraud.

- Transparency: All transactions are publicly recorded on the blockchain, providing a level of auditability.

- Accessibility: Anyone with an internet connection can participate in the crypto ecosystem.

However, this very decentralization creates complications for taxation.

Decentralized Finance (DeFi) and its Impact on Taxation

In 2021, research revealed that crypto crime reached a historic high of $14 billion. Decentralized Finance (DeFi) is a rapidly growing sector within the crypto ecosystem that offers financial services without traditional intermediaries.

This includes activities like lending, borrowing, and trading, all conducted through code on the blockchain. DeFi presents additional complexities for tax authorities:

- Evolving DeFi protocols: The rapid innovation in DeFi creates new instruments and activities that may not have clear tax classifications.

- Yield generation: DeFi allows for earning interest on crypto holdings through staking, liquidity pools, and other mechanisms. Tax authorities need to determine the appropriate way to tax these earnings.

Traditional Tax Systems and Their Struggle with Crypto

Traditional tax systems were designed for a world of centralized finance.

Cryptocurrencies, with their decentralized nature and anonymity features, pose several challenges:

- Pseudonymous transactions: While blockchain transactions are publicly viewable, they are linked to wallet addresses, not necessarily individuals. This makes it difficult to identify the owner of a wallet and track their crypto activity.

- Mixing services: Some users employ anonymizing services to further obscure the origin and destination of their crypto transactions, further hindering tax traceability.

- Multiple wallets and exchanges: Users may hold crypto across different wallets and exchanges, making it challenging for tax authorities to get a complete picture of their crypto holdings and transactions.

- Peer-to-peer transactions: Crypto can be traded directly between individuals without using a centralized exchange, making these transactions even more difficult to track.

- Lack of standardized regulations: Crypto regulations are still evolving around the world, leading to inconsistencies in how different countries approach crypto taxation.

- Varying tax treatment: The tax treatment of crypto can differ significantly across jurisdictions, creating confusion and potential loopholes for tax evasion.

How Cryptocurrencies Can Be Used for Tax Evasion

According to the IRS, in the United States alone, over $1 billion in tax revenue was lost due to unreported crypto transactions in 2020.

While cryptocurrency offers numerous benefits, its attractive features can also be exploited for tax evasion. Here, we explore some common techniques employed to avoid reporting crypto-related income to tax authorities:

Obscuring Transactions Through Anonymity Services

These services aim to break the link between the origin and destination of crypto transactions by mixing them with a pool of other funds before sending them out. This makes it difficult for tax authorities to track the flow of funds and identify the owner.

Utilizing Unregulated Exchanges and Peer-to-Peer Trading

Some crypto exchanges operate outside of regulatory frameworks, offering anonymity and limited reporting requirements. Users may exploit these platforms to conduct transactions without generating a record for tax purposes. Similarly, peer-to-peer trading directly between individuals bypasses centralized exchanges and their potential reporting obligations.

Misreporting Income from Crypto Activities

Crypto users can engage in various income-generating activities like mining, staking, and trading. However, some may deliberately underreport or completely fail to report these earnings on their tax returns, attempting to evade tax liabilities.

Exploiting Loopholes in Different Tax Jurisdictions

Crypto’s global nature allows users to take advantage of varying tax regulations across different countries. Some may move their crypto holdings to jurisdictions with more lenient crypto tax laws or exploit loopholes in specific tax codes to minimize their tax burden.

Mitigating Tax Evasion in the Crypto Space

Combating crypto tax evasion requires a multi-pronged approach involving collaboration between governments, the crypto industry and individual users.

Regulatory Efforts

Governments are implementing regulations that require crypto exchanges to collect user information (Know Your Customer – KYC) and report transactions exceeding certain thresholds to tax authorities.

For example, in August 2021, Binance implemented a new policy requiring KYC information from all users. This enhances transparency and makes it easier to track crypto activity.

Collaboration

Tax authorities are increasingly collaborating with crypto exchanges to share information and streamline the reporting process. This allows for better identification of taxable crypto activity.

Tracking and Tax Reporting of Crypto Transactions

Research is ongoing exploring the development of specialized tools for tracking crypto transactions and facilitating automated tax reporting.

Enhancing Tax Compliance: The Role of Blockchain

Ironically, the very technology that powers cryptocurrency, blockchain, also holds the potential to improve tax compliance:

Secure and Transparent Records

Blockchain transactions are immutable and publicly verifiable, providing a tamper-proof record of all crypto activity. Tax authorities can leverage this to track transactions and ensure their accuracy.

Automated Tax Reporting

Innovation in blockchain technology could lead to the development of automated tax reporting tools that integrate seamlessly with crypto wallets and exchanges. This would significantly simplify the tax reporting process for users.

The Role of Individual

While governments and the crypto industry work towards solutions, individual users also play a crucial role in promoting transparency:

- Keeping Accurate Records of Crypto Transactions: Maintaining detailed records of all crypto purchases, sales, trades, and mining rewards is essential for accurate tax reporting.

- Utilizing Crypto Tax Calculation and Reporting Software: Several software tools specialize in calculating and reporting crypto taxes. These tools can save time and ensure accurate reporting.

- Seeking Professional Guidance from Tax Advisors Specializing in Crypto: Consulting with a tax advisor experienced in crypto taxation can provide valuable guidance and ensure compliance with complex regulations.

The Future of Crypto Taxation in the Digital Age

The world of crypto taxation is still evolving, but several potential solutions hold promise for a more seamless and efficient system in the digital age:

Standardization of Crypto Tax Regulations Across Jurisdictions

The current patchwork of crypto tax regulations across different countries creates confusion and opportunities for exploitation. International collaboration to establish standardized rules and reporting requirements would significantly improve tax collection and reduce evasion attempts.

Integration of Blockchain Technology with Tax Reporting Systems

Harnessing the power of blockchain technology offers exciting possibilities. Imagine a future where tax authorities can access secure and immutable records of crypto transactions directly from the blockchain, streamlining the reporting process and enhancing accuracy.

Development of User-Friendly Crypto Tax Tools and Platforms

User-friendly crypto tax tools can significantly ease the burden on individual users. These tools could automatically track transactions across wallets and exchanges, calculate tax liabilities, and seamlessly integrate with tax filing systems.

Impact of Future Crypto Regulations on Tax Evasion Attempts

As regulations evolve and the aforementioned solutions become implemented, the landscape of crypto tax evasion is likely to change:

- Increased Difficulty for Tax Evasion: Standardized regulations, improved tracking capabilities, and user-friendly reporting tools will make it significantly more difficult for individuals to conceal crypto-related income.

- Focus on New Evasion Techniques: New evasion tactics may emerge as traditional methods become less viable. Continued collaboration between governments and the crypto industry will be crucial to stay ahead of these evolving attempts.

- Greater Transparency and Accountability: Ultimately, a future with clear regulations, robust tracking systems, and user-friendly reporting tools will foster a more transparent and accountable crypto ecosystem, benefiting both governments and responsible crypto users.

Conclusion

The rise of cryptocurrency presents unique challenges for tax authorities. While some may exploit the anonymity features of cryptocurrency for tax evasion, a collaborative effort is underway to establish a sustainable framework for crypto taxation in the digital age.

Governments are actively implementing regulations, enhancing collaboration with the crypto industry and exploring technological solutions. Blockchain technology, the very foundation of crypto, holds the potential to become a powerful tool for enhancing tax compliance.

However, individual responsibility remains crucial. Cryptocurrency users can contribute to a more transparent ecosystem by maintaining accurate records and utilizing available tools.

")