A study by The National Bureau of Economic Research found that cryptocurrencies, like Bitcoin, exhibit significantly higher volatility compared to traditional assets like stocks or bonds. This tends to raise concerns about its suitability as a mainstream store of value.

The adoption of cryptocurrency in central banking can be a shocking phenomenon to the traditional financial system, forcing it to confront a new reality. These decentralized digital currencies, with their promise of borderless transactions and unshackled innovation, challenge the long-held authority of central banks in controlling money supply and monetary policy.

But is cryptocurrency a threat to be vanquished or an opportunity to be embraced? This article explores the complex and evolving role of cryptocurrency in central banking.

Key Takeaways

- Cryptocurrency in central banking presents challenges like volatility and lack of regulation, and opportunities like DeFi’s innovation and CBDCs’ potential for efficiency and control.

- Considering issuing CBDCs, rethinking monetary policy tools and potentially adopting blockchain technology for improved efficiency and transparency may help central banks keep up with the digital age.

- Financial inclusion is a potential benefit of cryptocurrency because crypto wallets are accessible with just a smartphone and internet connection.

- The future of money remains uncertain with scenarios ranging from CBDCs coexisting with private cryptocurrencies to crypto eventually dominating the financial system.

Cryptocurrency in Central Banking

Cryptocurrency in central banking presents a potential opportunity for collaboration and innovation in the centralized and decentralized financial systems.

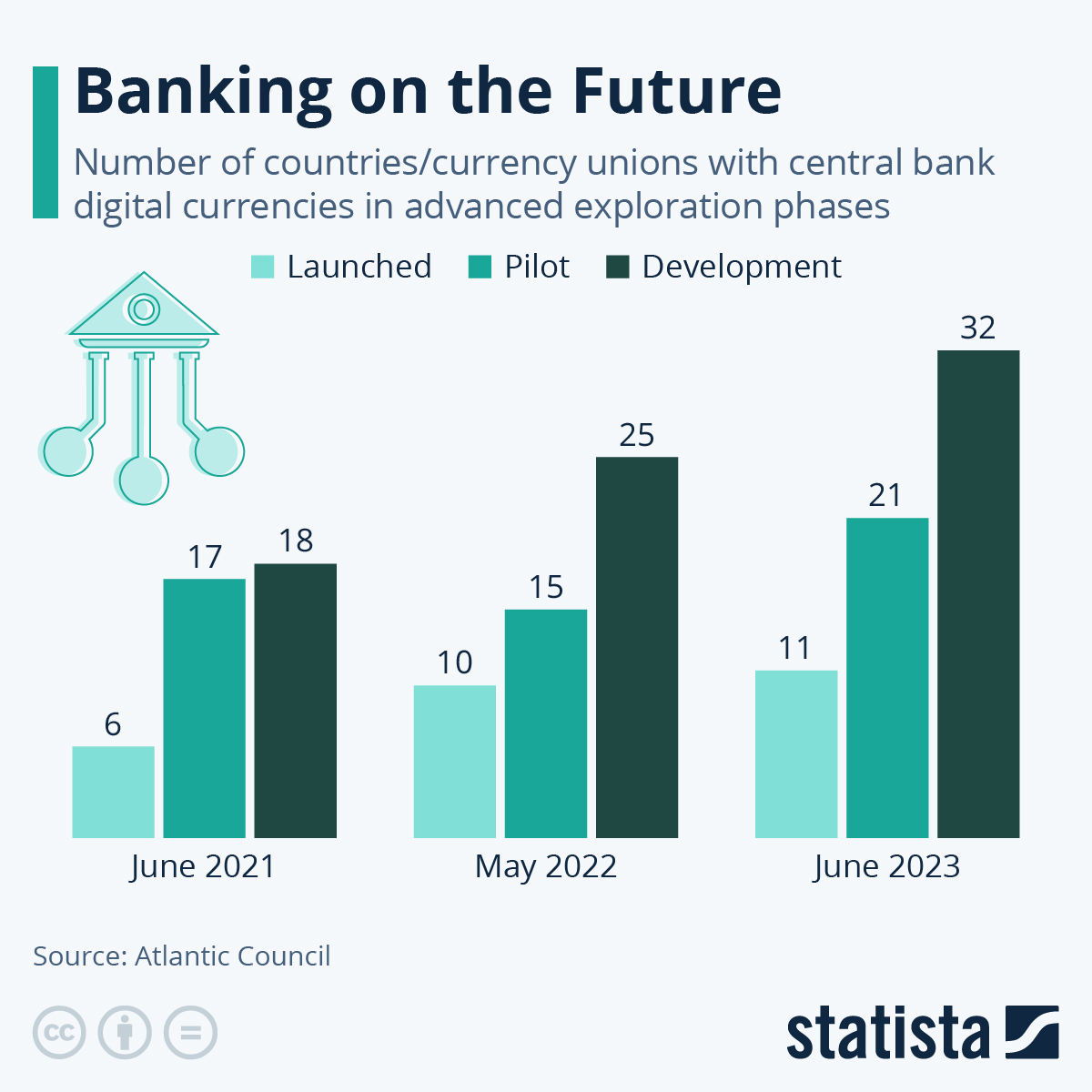

The rise of Central Bank Digital Currencies (CBDCs) as a potential response to cryptocurrency has gained significant traction all around the world. For example, in 2022, Russia’s central bank made a declaration indicating their receptiveness to the utilization of cryptocurrency for international payments.

Then, in April 2024, the Central Bank of Russia expects that full-scale integration of a Central Bank Digital Currency (CBDC) will occur beyond the year 2029.

This shows that central banks all around the world have begun to rethink their monetary policy in a world increasingly influenced by crypto, with considerations for both the potential benefits and drawbacks of these digital tokens.

How DeFi Bypasses Traditional Banking Systems

The emergence of Decentralized Finance (DeFi) marks a significant challenge to central banks’ traditional, centralized control.

As of March 2023, the total value locked (TVL) in DeFi protocols has exceeded $200 billion. This surge in TVL indicates the growing adoption and utilization of DeFi platforms by users worldwide.

DeFi applications operate on blockchain networks, effectively creating a peer-to-peer financial system that bypasses traditional intermediaries like banks.

Here is a look at how DeFi bypasses traditional banking systems:

- Loan and Borrowing: DeFi protocols allow users to lend and borrow cryptocurrencies directly from each other, eliminating the need for banks to act as gatekeepers.

- Automated Transactions: Smart contracts, self-executing code on the blockchain, automate financial transactions, reducing reliance on manual bank processes.

- Global Accessibility: Anyone with an internet connection can access DeFi applications, potentially increasing financial inclusion for the unbanked population.

Potential Risks of DeFi for Financial Stability

This decentralized nature of DeFi may also present potential risks for financial stability:

- Lack of Regulation: The absence of central oversight in DeFi can expose users to scams, hacks, and unstable investment products.

- Market Volatility: The inherent volatility of cryptocurrencies underlying DeFi applications can lead to sudden price swings and cascading loan defaults.

- Systemic Risk: The interconnectedness of DeFi protocols raises concerns about potential domino effects if one platform experiences a major failure.

Central Banking in the Crypto Age

Faced with the rise of cryptocurrency and the potential disruption of DeFi, central banks are actively exploring new strategies to maintain control and stability in the digital age.

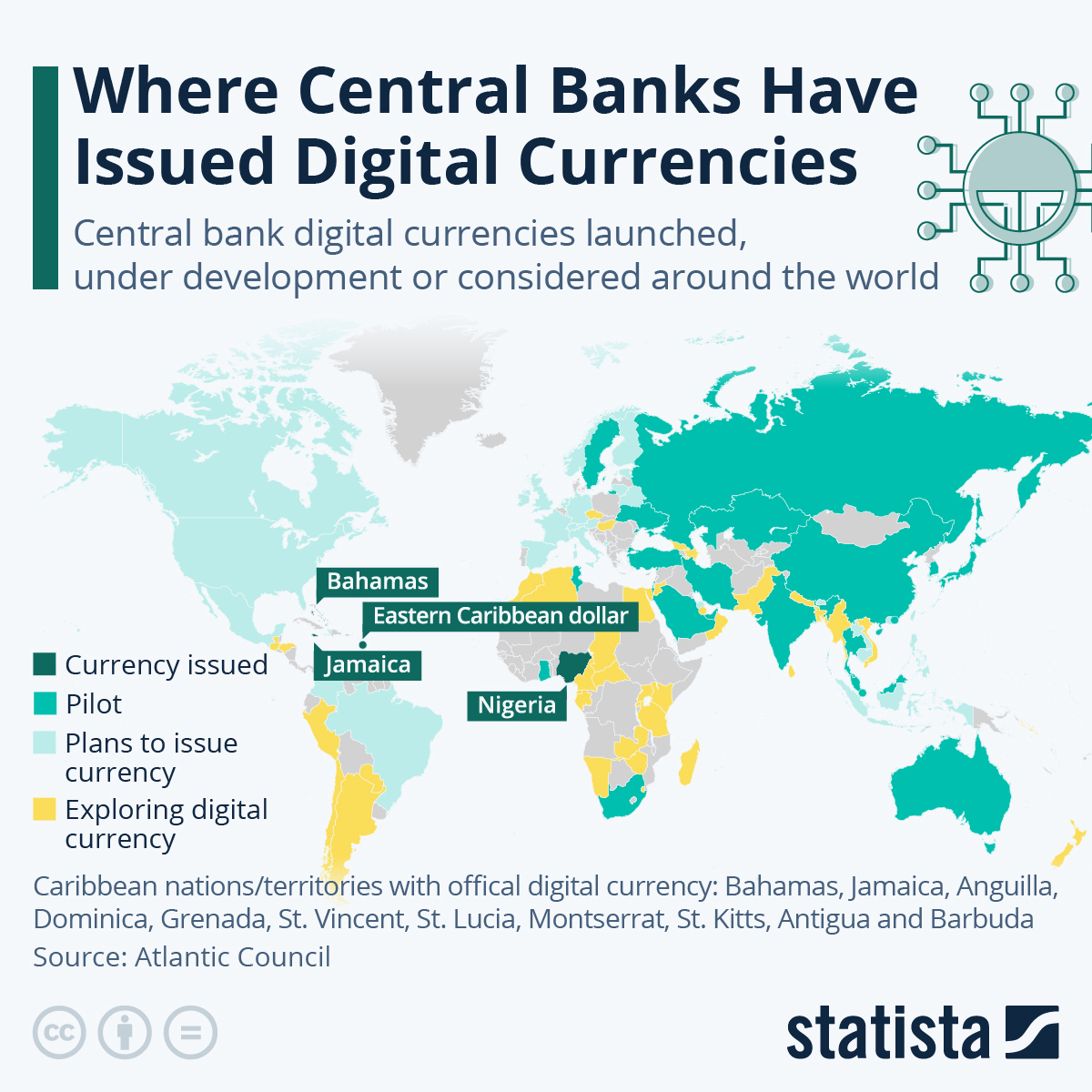

Central Bank Digital Currencies (CBDCs)

One key response has been the development of Central Bank Digital Currencies (CBDCs). CBDCs are digital versions of a country’s fiat currency, issued and backed by the central bank itself.

Benefits of CBDCs

Here are three of the benefits of CBDCs:

- Enhanced Efficiency: CBDCs can streamline cross-border payments, potentially reducing processing times and transaction costs.

- Increased Transparency: Central banks can have greater oversight and control over the flow of digital currency, potentially reducing the risk of financial crime.

- Programmable Money: CBDCs can be programmed with specific features, allowing central banks to target specific economic goals.

Drawbacks of CBDCs

Here are two of the benefits of CBDCs:

- Centralized Control: If not carefully designed, CBDCs could grant central banks excessive control over citizens’ financial activities, potentially infringing on privacy.

- Loss of Anonymity: Transactions involving CBDCs might be easily traceable, reducing the anonymity currently associated with some cash transactions.

Monetary Policy in Crypto World

Traditional monetary policy relies heavily on interest rates to manage inflation and stimulate economic activity. However, the rise of cryptocurrencies with their own dynamics raises questions about the effectiveness of these tools.

Here are two factors to consider:

- Reduced Leverage: If individuals hold a significant portion of their wealth in cryptocurrencies, they might be less responsive to changes in interest rates set by central banks.

- Competition from Crypto Interest Rates: DeFi applications often offer high-interest rates on crypto deposits, potentially rendering traditional savings accounts less attractive.

Here are alternative monetary policy tools for the digital age:

- Reserve Requirements: Central banks could adjust reserve requirements for banks holding CBDCs, influencing the money supply more directly.

- Digital Cash Limits: Limits could be placed on the amount of CBDC individuals can hold, potentially encouraging them to utilize traditional bank accounts.

- Central Bank Digital Currency Interest Rates: Central banks might consider offering interest rates on CBDCs to compete with DeFi and influence money circulation.

Blockchain Technology Adoption in Central Banking

Here are some ways in which blockchain technology adoption could enhance operations within central banking:

- Enhanced Transaction Auditing: Blockchain technology can provide central banks with a more secure and transparent audit trail for financial transactions.

- Improved Efficiency in Financial Processes: Streamlining back-office operations through blockchain can lead to significant cost savings and faster settlement times.

- Faster Settlement: Blockchain-based systems can potentially revolutionize cross-border payments by enabling near-instantaneous settlements and reduced transaction fees.

- Increased Financial Inclusion: The efficiency and accessibility of blockchain technology could extend financial services to currently unbanked populations.

- Lower Barriers to Entry: Cryptocurrency wallets can be accessed with a smartphone and internet connection, potentially bypassing traditional banking infrastructure limitations.

- Global Accessibility: Cryptocurrencies operate on a global network, potentially offering financial services to individuals in regions with limited access to traditional banking systems.

Can Cryptocurrency be Trusted in Central Banking?

The trustworthiness of cryptocurrency within central banking remains a complex question. While the decentralization and innovation of crypto offer exciting possibilities, concerns about volatility, money laundering and lack of central oversight pose significant challenges.

Price Fluctuations and Impact on Economic Stability

The value of many cryptocurrencies can fluctuate dramatically, raising questions about their suitability as a reliable store of value and medium of exchange. High volatility in cryptocurrency prices can create uncertainty for businesses and consumers. This can potentially hinder economic growth.

Sudden price swings can exacerbate market panics and financial crises if cryptocurrencies become more widely adopted.

Concerns About Money Laundering and Illegal Activity

The pseudonymous nature of some cryptocurrencies can make them attractive for money laundering and other illegal activities. Difficulty in tracking and tracing transactions on certain blockchains can also pose challenges for law enforcement.

Financial Literacy Gap and Digital Divide

Limited access to internet connectivity and smartphones in certain regions could hinder widespread crypto adoption.

Also, understanding the complexities of cryptocurrency markets and managing digital wallets requires a certain level of financial literacy, which might be lacking in some populations.

The Future of Cryptocurrency in Central Banking

The future relationship between cryptocurrency and central banking remains uncertain. Here are some possible scenarios:

CBDCs as the Dominant Form of Digital Money

This scenario envisions a future where central banks issue and control their own CBDCs, existing alongside private cryptocurrencies. This could create a more diverse and competitive financial ecosystem.

CBDCs might become the primary method for digital payments, with private cryptocurrencies relegated to niche uses or investment vehicles.

According to a report from Bison Trails, a blockchain infrastructure company, a significant proportion of central banks are investigating applications for central bank digital currencies (CBDCs). Approximately 40% of these banks have embarked on proof-of-concept projects, and approximately 80% are evaluating various use cases involving CBDCs.

Private Cryptocurrencies as a Viable Alternative

Cryptocurrencies could continue to evolve, offering features or functionalities not available with CBDCs. This can attract a dedicated user base.

Cryptocurrency Dominance

In a more extreme scenario, cryptocurrencies could potentially become the dominant form of money, gradually replacing traditional fiat currencies. This would represent a significant shift in the global financial system.

Cryptocurrencies might become the go-to method for everyday purchases, displacing traditional cash and credit cards. The widespread use of cryptocurrencies could significantly diminish the ability of central banks to influence economic activity through traditional monetary policy tools.

Finding Common Ground

The future of cryptocurrency and central banking likely lies in finding common ground through collaboration and effective regulation.

- Regulation: One crucial aspect is establishing a clear regulatory framework for the cryptocurrency market. This framework needs to strike a balance between innovation and maintaining financial stability.

- Defining Crypto Assets: Clear classification of cryptocurrencies and tokens as commodities, securities, or something else is essential for applying appropriate regulations.

- Anti-Money Laundering (AML) and Know Your Customer (KYC) Rules: Implementing KYC and AML protocols for cryptocurrency exchanges and service providers can help combat financial crime.

- Consumer Protection Measures: Regulations should protect consumers from scams, fraud and excessive market volatility in the crypto space.

Conclusion

The rise of cryptocurrency has undoubtedly made traditional financial systems and central banks confront a new reality.

There are complexities involved in this evolving relationship of cryptocurrency in central banking, including the disruptive potential of DeFi, the challenges posed by crypto volatility and the potential of Central Bank Digital Currencies (CBDCs) as a response.

Central banks might need to adapt their monetary policy tools and collaborate with the cryptocurrency ecosystem to ensure an overall financial stability for economic growth.

The future of money remains uncertain. Will central banks and cryptocurrencies coexist or will one eventually dominate the other?

Central banks can leverage the transparency and efficiency of blockchain technology, while the cryptocurrency space can benefit from clear regulations and consumer protection measures.