For businesses and startups, access to flexible credit can determine how efficiently operations scale and how well cash flow is managed. Traditional credit systems often slow this process down, requiring personal guarantees, lengthy paperwork, and rigid approval standards that don’t reflect the pace of modern companies.

That’s where the Brex Business Card steps in. It’s designed specifically for high-growth startups, e-commerce brands, and tech-driven businesses that need fast, adaptable financing tools. Brex offers a no-personal-guarantee, no-credit-check corporate card, giving companies access to instant credit based on business performance rather than personal credit scores.

In today’s market, where digital-first companies rely on automation and efficiency, Brex provides more than a spending solution. It integrates expense tracking, team management, and rewards into one streamlined platform — helping founders maintain control while scaling faster.

This review will explore how the Brex Business Card works, its core features, fees, and rewards, as well as where it performs best and where it may have limitations. You’ll also discover six strong alternatives to compare, ensuring you choose a business card that matches your operational and financial goals in 2025.

UEEx, a fast-growing cryptocurrency exchange offering global trading options and innovative tools, supports smarter financial access by connecting digital businesses to modern, efficient payment ecosystems like Brex.

Key Takeaways

- Brex Business Card offers no annual fees, no interest, and doesn’t require a personal guarantee or credit check.

- Dynamic credit limits are based on your company’s cash flow, not personal credit.

- Highest rewards are earned through daily repayments and spending in select business categories.

- Integration with accounting software and expense tracking tools enhances financial management.

- Strict eligibility requirements and inconsistent customer service may limit accessibility for early-stage startups.

What is the Brex Card?

The Brex Card is a corporate charge card built specifically for startups, tech companies, and high-growth businesses that prioritize speed, automation, and flexibility in managing their finances.

Unlike traditional business credit cards, the Brex Card does not rely on a personal guarantee, credit check, or founder liability. Instead, it determines a company’s credit limit using real-time business data such as cash flow, spending behavior, and overall financial health — giving modern businesses access to scalable credit without personal risk.

The card is issued through Emigrant Bank or Fifth Third Bank N.A., depending on the account type and repayment plan selected. While Brex itself is not a bank, it functions as a financial technology company that partners with regulated banking institutions to provide corporate credit, spending management, and financial automation tools.

Founded in 2017, Brex has become one of the most recognized fintech providers for venture-backed startups, SaaS firms, and remote-first companies seeking global spending solutions.

The Brex Card primarily targets high-growth businesses, e-commerce brands, and technology-driven organizations that need dynamic credit access and integrated expense control. It is also suitable for smaller startups that have secured funding or maintain strong cash balances, even without an established credit history.

What sets the Brex Card apart from traditional business credit cards is its charge card structure — requiring either daily or monthly repayment, depending on eligibility.

This ensures businesses avoid revolving debt while maintaining liquidity. Brex also eliminates personal credit checks and guarantees, which are typically required by banks, and instead focuses on business metrics to extend credit.

Operating on a cloud-based financial platform, Brex integrates accounting tools, real-time expense tracking, receipt management, and team-based spending controls into one centralized dashboard.

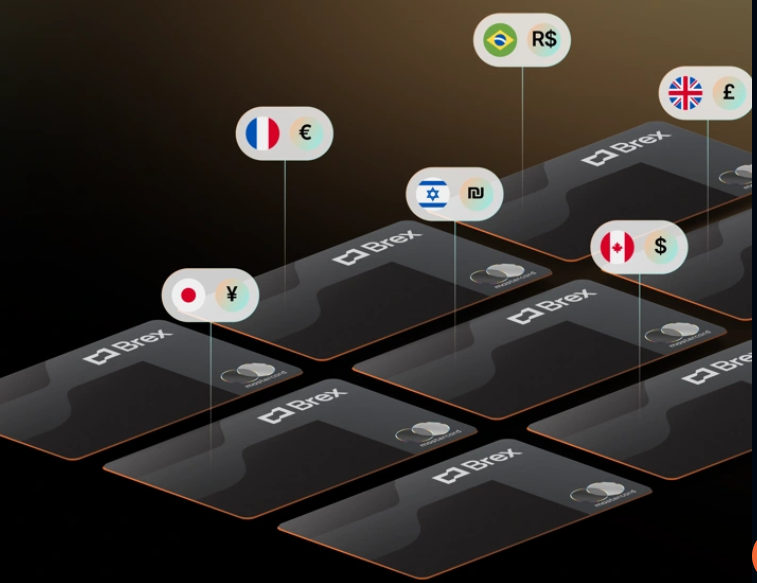

The system supports both physical and virtual cards, allowing companies to issue and manage cards for employees across 50+ countries, with the ability to reimburse team members in their local currency.

With multi-currency support in USD, CAD, EUR, GBP, BRL, INR, JPY, and more, the Brex Card makes it easier for global teams to spend locally.

In essence, Brex provides a future-focused financial infrastructure that empowers companies to spend globally, operate locally, and scale efficiently without the limitations of traditional credit systems.

Quick Facts Table

| Feature | Details |

| Card Network | Mastercard |

| Card Type | Corporate Charge Card |

| Issued By | Emigrant Bank or Fifth Third Bank N.A. |

| Annual Fee | None |

| APR Range | Not applicable (charge card – no interest) |

| Welcome Offer | None currently available |

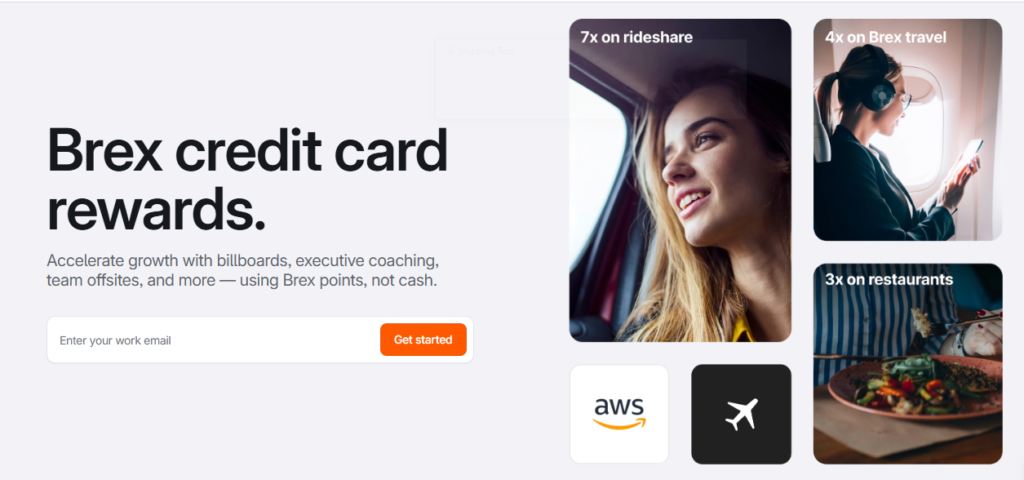

| Rewards Rate | Daily Repayment: 7x rideshare, 4x travel, 3x restaurants, 2x software, 1x all other; Monthly Repayment: 1x all categories |

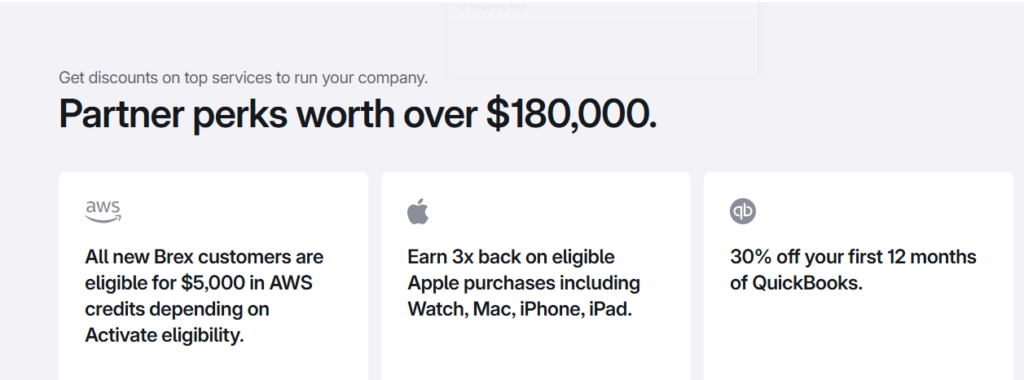

| Partner Rewards | Up to $180,000 in discounts/credits with AWS, Slack, Notion, Zoom, and others |

| Foreign Transaction Fees | $0 (no fees on international spending) |

| Credit Check Required | No |

| Personal Guarantee Required | No |

| Minimum Requirements | U.S. EIN, U.S. business bank account, $50,000+ available cash (or $1M+ if venture-backed for monthly terms) |

| Application Timeline | Instant approval for qualified businesses; virtual card available immediately; physical card in 5–7 business days |

| Repayment Terms | Daily or monthly (depending on qualification) |

| Availability | U.S.-based businesses (global usage supported) |

Features of the Brex Business Card

The Brex Business Card is packed with features that simplify financial management and support business growth.

From flexible credit limits to automation tools, here’s a closer look at what makes Brex stand out:

Credit Limits Based on Business Financials

Instead of relying on a founder’s personal credit score, Brex determines your credit limit based on your company’s cash flow, revenue, and spending habits. This allows growing businesses and startups to access higher limits as they scale, without risking personal assets or providing a personal guarantee.

No Annual Fees, Interest, or Personal Credit Checks

Brex charges no annual fees or interest. Since the card operates on a charge model (daily or monthly auto-pay), there’s no APR. It also skips personal credit checks entirely, making it ideal for founders who want to keep their personal finances separate from their business.

Real-Time Expense Tracking and Automated Accounting Integrations

Brex includes powerful tools for real-time expense management. You can categorize transactions, upload receipts via mobile, and integrate directly with accounting software like QuickBooks, Xero, NetSuite, and more. This automation saves time and improves financial accuracy for your team.

Rewards Program and Partner Discounts

With Brex, you earn points on every purchase, with bonus rewards for spending in categories like ads, travel, and software, especially when you choose daily payments. Brex also offers exclusive partner discounts with services like AWS, Slack, Zoom, and HubSpot, adding even more value for growing companies.

Virtual and Physical Card Options

You can issue both virtual and physical Brex cards for team members, with customizable spending limits and real-time visibility. This makes it easy to manage distributed teams and control business spending without waiting for a physical card to arrive.

Rewards Program

The Brex Business Card offers a rewards program tailored to companies that spend heavily in common business categories like advertising, software, and travel.

Brex rewards companies based on their payment frequency and integration with Brex’s ecosystem.

They have:

Earning Rewards

Brex rewards users with points on every purchase, but the rate depends on how often you repay. Companies enrolled in daily auto-pay earn higher point multipliers compared to those on a monthly basis.

Bonus Categories for Daily Payments

If you opt for daily repayments, you’ll earn:

- 7x points on rideshare (e.g., Uber, Lyft)

- 4x points on Brex Travel (flights, hotels)

- 3x points on restaurants

- 2x points on software subscriptions

- 1x point on all other spending

Monthly payers receive 1x point on all categories by default, making daily repayment more rewarding for companies with consistent cash flow.

Partner-Specific Offers

Brex also includes exclusive partner rewards and discounts for tools and services your business may already use. Offers include:

- Up to $180,000 in value through partners like AWS, Slack, Notion, Zoom, and more

- Custom deals and credits for marketing tools, cloud platforms, and CRM software

Redeeming Rewards

Brex offers multiple flexible redemption options, including:

- Travel bookings through the Brex Travel portal

- Statement credits

- Gift cards from major retailers

- Cryptocurrency redemptions, for those interested in digital assets

Rewards never expire and can be redeemed at any time through your Brex dashboard.

Rewards Potential

The Brex Card is most rewarding for:

- High-volume spenders

- Businesses that opt into daily repayments

- Companies with regular expenses in software, ads, travel, or meals

Because rewards are based on business spend and not personal use, this card delivers the highest value when fully integrated into your company’s financial operations.

Brex Card Limits and Controls

The Brex Business Card offers flexible limits and advanced control features designed to fit the financial structure of modern startups and scaling businesses.

Instead of relying on a founder’s personal credit or static limits, Brex uses a company’s cash flow, revenue, and funding activity to determine spending capacity, allowing qualified businesses to access up to 40x higher limits than traditional corporate cards.

Credit and Spending Limits

Credit limits on the Brex Card are dynamic, adjusting automatically as your company’s financial data changes. By linking a Brex business account with the card, organizations can unlock significantly higher limits based on real-time balance insights.

This model ensures that limits grow alongside your business performance rather than being restricted by outdated credit checks or guarantees.

Brex also offers daily and monthly repayment options. Companies on the daily plan have limits tied to cash balances and transactions settled each business day, while those approved for monthly repayment enjoy greater flexibility with full-cycle billing.

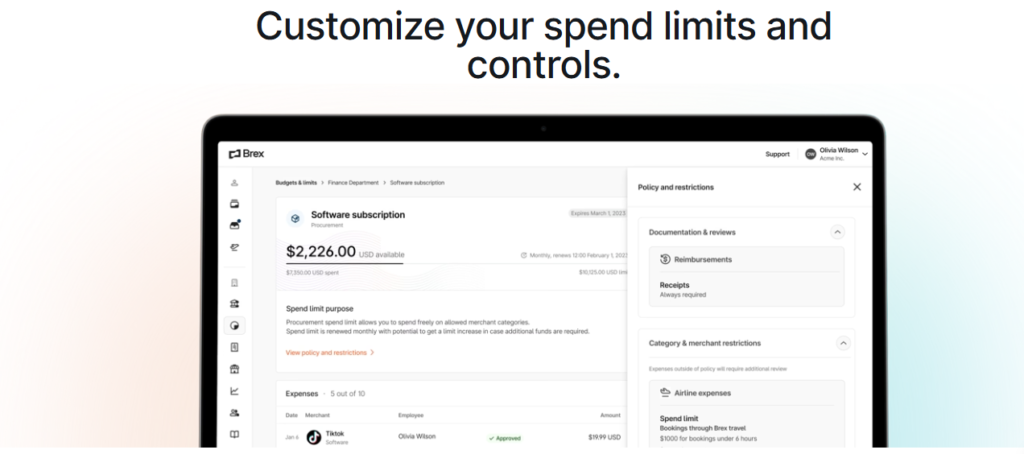

Control

Brex provides extensive spend management tools that allow businesses to maintain visibility and oversight across all corporate expenses.

Admins can:

- Set custom limits for employees, teams, or departments.

- Issue virtual and physical cards with pre-defined spending categories.

- Lock, freeze, or cancel cards instantly through the Brex dashboard.

- Track transactions in real time with automated receipt matching and categorization.

- Integrate accounting platforms like QuickBooks, NetSuite, and Xero for seamless reconciliation.

Treasury and Liquidity Integration

Through its Brex Business Account, users can also move funds between checking and treasury accounts within an hour, earning up to 4.21% APY with same-day liquidity. These integrated features give startups full control over cash management while ensuring security through FDIC insurance up to $6 million via partner banks.

Technology Integration

The Brex Card is more than just a corporate payment tool, it’s a fully integrated financial platform that combines expense management, automation, and real-time reporting across web, mobile, and API environments.

Designed for modern, tech-driven organizations, Brex simplifies how businesses track, control, and optimize spending through intelligent software and seamless integrations.

Brex Mobile App

The Brex mobile app acts as a full-featured expense and travel management assistant, allowing users to manage spending anywhere, anytime. Through the app, employees can track expenses, book travel, request spending limits, upload receipts, and make payments with just a few taps.

- Users can access their card details instantly for online or in-person purchases via digital wallets.

- The app automatically detects when receipts are needed, sends reminders, and allows for quick photo uploads.

- Managers can view real-time spending limits, transactions, and pending approvals, ensuring full visibility and compliance on the go.

- Integrated travel management tools allow users to book flights, hotels, and rentals, manage reimbursements, and modify itineraries directly from the app.

- With 24/7 global support, users can chat or call Brex Support anytime to resolve issues efficiently.

Software and Integrations

Brex integrates with a wide range of business and accounting software, helping finance teams automate data flow and reporting. These include QuickBooks, NetSuite, Xero, Sage Intacct, and major ERP and HRIS systems.

- Through continuous reconciliation, expenses and receipts automatically sync with your accounting platform, reducing manual work.

- Custom fields let companies apply rules that auto-categorize transactions, manage HR data, and synchronize records across finance and HR platforms.

- Integrations with Workato, Zapier, Slack, and Microsoft Teams enable automated alerts and workflow updates for better accountability and communication.

APIs and Developer Tools

For businesses with advanced needs, Brex offers robust APIs to automate payments, reporting, and card issuance.

- The Payments API enables programmatic ACH, wire, and check transactions.

- The Transactions API provides real-time access to transaction data for analytics and reporting.

- The Team API allows automated onboarding and offboarding of users, as well as issuing virtual cards with custom spending limits.

Brex Embedded extends Brex’s card functionality directly into third-party platforms like procurement or ERP systems, enabling instant reconciliation and control.

Through these integrated technologies, the Brex Card ecosystem delivers a unified, automated, and scalable financial infrastructure, reducing manual processes, enhancing transparency, and giving companies full control over corporate spending from a single, intelligent platform.

Security Features

Source: Freepik

The Brex Business Card is built with enterprise-grade security measures that protect both your financial data and business transactions. From encryption to fraud prevention, Brex prioritizes safety at every layer of its platform.

Account Security

Brex uses TLS 1.2+ encryption for data in transit and AES-256 or better for data at rest, ensuring your information is always protected. Features like idle lockouts, iFrame protection, and a strict content security policy help prevent unauthorized access or malicious activity.

Authentication is reinforced through strong password requirements, Face ID/Touch ID, and two-factor authentication (2FA). Users must also complete device and browser verification before accessing an account, making unauthorized logins extremely difficult.

Data Privacy

Brex is committed to protecting customer privacy, with data usage policies aligned to strict regulatory frameworks. Personal and financial data is never shared without consent, and their privacy policy clearly outlines how your information is stored and protected.

24/7 Fraud Monitoring and Prevention

With real-time fraud detection, Brex uses AI-powered monitoring systems to flag suspicious behavior before it becomes a threat. Accounts are continuously observed, and any unauthorized changes—such as password resets—trigger both automated and manual reviews.

Fraud prevention measures ensure that only authorized users can make changes or approve transactions, giving businesses control and peace of mind.

Read Also: Top 10 Cryptocurrency Security Best Practices for Beginners

Compliance Standards

Brex meets a wide range of industry-leading compliance benchmarks, including:

- SOC 1 Type I and SOC 2 Type II

- PCI-DSS for payment security

- FINRA and NY Department of Financial Services requirements

These certifications validate Brex’s commitment to maintaining top-tier security standards.

Additional Benefits

Beyond credit access and rewards, the Brex Business Card delivers a suite of additional benefits designed to make financial management simpler, safer, and more efficient for modern companies.

From advanced automation to global accessibility and strong security protections, Brex gives businesses the tools to operate seamlessly at scale.

No Personal Guarantee or Credit Check

One of Brex’s most significant advantages is that no personal guarantee or founder credit check is required. Your company’s approval and limit are based solely on its financial health, not your personal score. This structure protects business owners from personal liability while still providing generous access to credit.

Global Spending with No Fees

Brex is built for global operations. Businesses can spend in over 50 countries with zero foreign transaction fees and the ability to reimburse employees in local currencies. This feature is ideal for international teams and startups managing operations across borders.

Automated Bill Pay and Expense Management

Brex simplifies financial operations through integrated bill pay and automated expense management. You can approve, schedule, and track payments from one dashboard while syncing everything directly to your accounting software.

Real-time expense tracking, automatic receipt capture, and pre-set spend limits help finance teams maintain full control with minimal manual input.

Built-In Treasury and Cash Management

Businesses that pair their Brex Card with a Brex Business Account can earn yield while maintaining liquidity. Funds can move between checking and treasury in under an hour, earning up to 4.21% APY with the security of up to $6 million in FDIC insurance through partner banks.

Fees and Pricing

| Fee Type | Cost/Policy |

| Annual/Monthly Fees | $0 – No annual or monthly fees. |

| Transaction Fees | $0 – No transaction fees on eligible purchases. |

| Cash Advance Fees | Not applicable – Brex does not support cash advances. |

| Late Payment Fees | Typically $0 – Brex may pause or review your account if payments fail but does not charge a fee. |

| Over-Limit Fees | $0 – Dynamic limits adjust automatically based on cash flow; no over-limit fees. |

| Foreign Transaction Fees | $0 – No foreign transaction fees; use globally in 50+ countries. |

| Hidden or Uncommon Fees | Minimal / Varies – Possible fees for expedited card shipping or third-party wire/ACH transfers. |

The Brex Business Card is built around transparency and cost efficiency, offering a clear fee structure with no hidden charges or surprise costs.

Annual and Monthly Fees

Brex charges no annual or monthly fees. Businesses can issue cards, add users, and access standard features, including rewards, expense management, and reporting, at no additional cost.

Transaction Fees

Brex does not charge standard transaction fees for purchases. All eligible transactions earn points under the Brex Rewards Program, and there are no extra charges for domestic spending or online payments made through the card.

Cash Advance Fees

The Brex Card functions as a charge card, not a revolving credit card, so it does not support cash advances. Because balances are paid in full daily or monthly, there’s no interest or cash withdrawal functionality, which helps prevent unnecessary borrowing costs.

Late Payment Fees

Brex typically does not charge late fees. However, if a scheduled payment fails or your linked bank account lacks sufficient funds, your account may be temporarily paused or reviewed to prevent further spending until the issue is resolved.

Over-Limit Fees

There are no over-limit fees with Brex. Credit limits are dynamically adjusted based on your company’s cash flow, spending patterns, and account balance, ensuring spending remains within your financial capacity.

Foreign Transaction Fees

All international spending through Brex is fee-free. You can use the card in 50+ countries and make payments in multiple currencies without paying foreign transaction charges, making it ideal for global teams and international operations.

Hidden or Uncommon Fees

Brex maintains a no-hidden-fee policy. The only potential third-party costs may occur for services outside Brex’s control, such as expedited card shipping or bank fees on wire and ACH transfers processed through Brex business accounts.

Eligibility and Application Process

Getting the Brex Business Card is a simple, fully digital process — designed to help companies access flexible credit quickly without the traditional banking hurdles. However, approval depends on your business structure, cash flow, and financial profile.

Who Can Apply

The Brex Card is available exclusively to U.S.-registered businesses with established operations or predictable revenue streams.

Eligible entities include:

- C-Corporations, S-Corporations, and LLCs

- Venture-backed startups and digitally operated companies

- Businesses with consistent revenue or strong cash reserves

Currently, sole proprietors and unincorporated businesses are not eligible.

Brex does not require a personal credit check or a personal guarantee. Instead, it bases approvals and limits on your company’s financial health, cash balance, and spending history, making it ideal for founders who want to separate personal and business finances.

Required Documents

To apply successfully, your company should have the following:

- Employer Identification Number (EIN): Required to verify your U.S. business registration.

- U.S. Business Bank Account: Brex connects directly to your bank via a secure, read-only link to assess cash flow.

- Proof of Funds: Startups typically need at least $50,000 in available cash, while venture-backed companies applying for monthly terms may need $1 million or more.

- Basic Company Details: Such as your business name, industry, website, and structure (LLC, C-Corp, etc.).

Step-by-Step Application Guide

- Visit the Brex website and click “Get Started.”

- Create an account using your business email address.

- Connect your business bank account securely to verify financial data.

- Enter company information including EIN, structure, and operational details.

- Select a repayment plan — daily or monthly (if qualified).

- Review and submit your application.

- Issue virtual and physical cards once approved.

- The entire process typically takes under 10 minutes and is fully online.

Approval Timeline

Brex offers instant approval for most qualified applicants after reviewing financial data from your linked bank account. If approved, you’ll receive a virtual card immediately for instant use, while your physical card arrives within 5 to 7 business days.

What Happens After Approval

Once approved, you can:

- Start spending instantly with your virtual Brex Card.

- Invite team members and issue virtual or physical cards with custom limits.

- Set up integrations with accounting tools and expense management systems.

- Access your Brex dashboard to manage rewards, payments, and reports in real time.

Pros and Cons of Brex Business Card

The Brex Business Card offers an innovative approach to business credit, one that prioritizes company performance over personal guarantees.

It’s built for fast-growing startups, tech firms, and digital businesses that value automation, control, and transparency.

However, like any financial product, it has its advantages and limitations depending on your company’s stage and needs.

Pros

High Credit Limits Based on Cash Flow

Brex determines your credit limit using real-time business data, such as revenue, cash balance, and spending habits, rather than your personal credit score. This allows startups with strong cash reserves but limited credit history to access significantly higher limits (up to 40x more) than traditional business cards.

Valuable Rewards on Core Business Spending

The Brex Rewards Program offers 7x points on rideshare, 4x on travel, 3x on restaurants, and 2x on software subscriptions. For example, a startup spending heavily on SaaS tools and travel can easily rack up rewards without changing its spending habits.

No Personal Guarantee or Credit Check

Founders aren’t personally liable for the company’s debts, Brex approvals are entirely business-based. This protects personal credit and eliminates the risk associated with traditional guarantees required by banks.

Real-Time Expense Tracking and Integrations

Brex integrates seamlessly with QuickBooks, NetSuite, and Xero, automatically categorizing transactions and syncing data. Finance teams can track expenses in real time and close books faster with continuous reconciliation.

Transparent, No-Fee Structure

With no annual fees, no foreign transaction fees, and no interest, Brex offers one of the most transparent fee structures in the industry. Daily repayments ensure businesses don’t accumulate debt or pay unnecessary interest.

Access to Exclusive Partner Perks

Brex users can unlock over $150,000 in partner rewards from companies like AWS, Slack, Notion, and Zoom, making it ideal for startups building their tech stacks efficiently.

Cons

High Minimum Cash Requirement

Startups must maintain at least $50,000 in available cash (or $1 million for venture-backed companies applying for monthly terms). This can be restrictive for smaller or early-stage businesses.

No Traditional Financing or Carry-Over Option

Since Brex is a charge card, balances must be paid in full daily or monthly. It doesn’t offer 0% intro APRs or financing options, limiting flexibility for companies that rely on short-term borrowing.

Fluctuating Credit Limits

Brex’s limits adjust dynamically with your company’s financial health. A sudden dip in revenue or cash balance could lower your spending capacity.

Not Available to Sole Proprietors

Freelancers and unincorporated entrepreneurs currently don’t qualify, as Brex focuses on incorporated U.S. businesses.

User Reviews and Feedback

Here’s what real users are saying about the Brex Business Card, highlighting both the strengths and areas needing improvement.

Positive Feedback

- G2 (Maria Pradeep I., Mid-Market, 51-1000 employees):

“Brex is very easy to use in terms of corporate spending – both from an approval standpoint and how easy it is to use as a user.”

- Capterra (Phillip K., Software Engineer, 2 – 10 employees):

“Favorite feature is that you can text them your receipts with basically a 99% chance that it works. It’s stupid how simple the features are so it’s amazing that other companies can’t catch on.”

- G2 (Sean B., Mid‑Business, 51-1000 employees):

“Brex is a great company credit card to use!! Easy set up, and great app interface”

Constructive Criticism

- Capterra (John L., CEO, 11 – 50 employees):

“Delay in reflecting payment after account has been debited.“

WalletHub reviews:

- Ryan B. (July 15, 2022): “50K is the requirement. I linked my account with 120K in it. I was denied and they will not give me an explanation. What’s the point of offering a card for start ups if you’re not going to assist them?”

- Ali J. (June 16, 2022): “Poor service and non‑startup friendliness… Do not trust or use Brex.”

Top 6 Alternatives to Brex Business Card

Choosing the right business card can significantly affect how smoothly your company handles expenses, cash flow, and payments.

While the Brex Business Card offers a strong package, especially for startups with high cash flow, it may not be the best fit for every business.

The options below give you a clear view of what else is out there and why you might pick one over Brex.

Ramp Business Card (Issuer: Ramp Business Corporation)

Best For: Businesses focused on cost control and automation

Founded as a modern corporate charge card + expense-management platform, Ramp positions itself as a direct competitor to Brex. The Ramp card requires linking to your business bank and pays off the balance monthly (charge-style), but emphasises automation, real-time spend analytics, and no annual fee.

Key Differentiators

- $0 annual fee, no foreign transaction fee.

- Built-in analytics and automation for expense tracking, vendor management and accounting integration.

- Real-time savings insights (claims 5%+ savings on vendor contracts) and unlimited virtual/physical cards.

Pricing

- Annual fee: $0.

- Main costs: You must pay your balance in full each month (charge card).

- No interest or revolving APR.

Pros

- No annual or foreign transaction fees — helps control cost.

- Excellent expense-management and integration features for finance teams.

- No personal credit check or personal guarantee required, underwriting based on business cash flow.

Cons

- Still requires strong cash flow and likely significant minimums (e.g., $25K+ linked bank balance).

- Must have most of your operations and corporate spend in the US (though international purchases are supported with no foreign transaction fees).

Why Choose Over Brex:

If you prioritise lower fees and strong automation/analytics rather than ultra-high reward multipliers, Ramp may deliver more net value and fewer surprises.

Capital One Spark Cash Plus (Issuer: Capital One)

Best For: High-spend businesses seeking no preset spending limit

The Spark Cash Plus card from Capital One offers unlimited 2% cash back on all purchases, a generous welcome bonus and no preset spending limit (charge card model).

Key Differentiators

- Unlimited 2% cash back everywhere, no category restrictions.

- Offers welcome bonus: $2,000 cash back when you spend $30,000 in first 3 months; plus additional $2,000 for each $500K spent in year one.

- Refundable annual fee of $150 if you spend $150K in a year.

Pricing:

- Annual fee: $150 annual fee

- No interest since it’s a charge card

- Foreign transaction fee: $0.

Pros

- Very generous welcome bonus and strong flat-rate cash-back.

- Free employee and virtual cards; strong integration with accounting tools.

- No foreign transaction fees — good for global spend.

Cons

- Annual fee is significant unless you hit the $150K spend to get refund.

- Because it’s a traditional bank charge card, you may need strong credit and history (versus purely cash-flow underwriting).

Why Choose Over Brex:

If your business spends broadly and wants simplicity (flat cash-back) rather than category-based rewards and you’re comfortable with a $150 fee, this is a strong high-tier alternative.

BILL Spend & Expense (formerly Divvy)

Best For: Cost-sensitive or mid-sized teams needing strong spend controls

BILL Spend & Expense is cited as a budget-friendly alternative to Brex, especially for businesses who may not meet high minimums.

Key Differentiators

- Minimal bank minimums compared to Brex and Ramp.

- Focus on budget control: virtual cards with custom limits, subscription tracking, and granular spend visibility.

- Free virtual cards for teams, tailored for SMBs rather than high-growth venture-backed firms.

Pricing

- Many basic plan features have $0 annual fee; however, specific benefits may cost.

Pros

- Lower barrier to entry for smaller companies or those not yet venture-backed.

- Strong spend-control features (virtual cards, employee controls).

- Affordable and scalable for mid-sized teams.

Cons

- Rewards and perks are less generous compared to Brex or premium cards.

- May not support ultra-high spend or complex multi-entity/global use cases as well.

Why Choose Over Brex:

If you don’t meet Brex’s high minimums (e.g., $50K+) or your spend/reward needs are simpler, BILL offers a more accessible alternative without sacrificing core controls.

UPay Card

Best For: Users focused on global payments

UPay is a crypto-card + wallet solution oriented to global payments, offering ultra-low fees, real-time FX rates, no cross-border fees and fast onboarding.

Key Differentiators

- Zero cross-border fees and real-time exchange rates to reduce hidden costs.

- Asset-backed spending limits: using crypto assets or collateral in the wallet to enable spending.

- Simpler fee structure with low ATM/withdrawal fees and global merchant acceptance.

Pricing

- No annual fee

- Low transaction fees (1% + no FX markup).

- ATM withdrawals around 2% in many cases.

Pros

- Ideal for global teams/travel or companies making cross-border purchases.

- Supports crypto-backed spending, which may appeal to fintech/crypto firms.

- Transparent fee structure, less hidden FX/spread cost.

Cons

- Because it’s crypto-centric, may lack established financing/traditional underwriting for some businesses.

- Not yet as widely adopted for large-scale enterprise spend/expense workflows as mainstream cards.

Why Choose Over Brex:

If your team spends internationally, has cross-currency needs, or deals in crypto, UPay offers cost advantages and global flexibility that Brex’s more US-centric model may not match.

Chase Ink Business Preferred® Credit Card

Best For: Established businesses with a traditional bank relationship and travel-heavy spend

This card from Chase offers strong travel rewards and robust benefits, suitable for businesses already banking with Chase.

Key Differentiators

- Strong travel bonus categories: e.g., high points on travel & shipping via Chase portal.

- Traditional bank backing with broad institutional support, many branches & services.

- Familiar underwriting and bank relationship benefits — ideal for mature businesses.

Pricing

- No Annual Fee

- No Foreign Transaction Fee

- 0% Intro APR

Pros

- Travel perks and broader reward flexibility for more mature companies.

- Strong service and bank infrastructure (branches, lending relationships).

- Free foreign transaction fee (per some versions) and broad acceptability.

Cons

- Requires personal guarantee and credit check — not purely business-based underwriting as Brex.

- Lower ceiling for spending and less built-in automation compared to fintech peers.

Why Choose Over Brex:

If your business has a strong bank relationship, significant travel spend, and you prefer a more traditional credit-card model, the Chase Ink may align better than Brex’s startup-oriented model.

Mercury IO Corporate Charge Card (Issuer: Mercury Technologies Inc.)

Best For: Startup or fintech-friendly businesses using a modern banking platform

Mercury is a fintech banking platform targeted at startups. Its corporate charge card fits businesses that want modern banking + card together.

Key Differentiators

- Banking + card integrated: Mercury offers business bank accounts for startups and now a charge card tied in.

- Startup-friendly fintech design: modern UI, integrated tools for tech-first companies.

- Flexible deposit protections via sweep network across partner banks — may appeal to fintech-savvy founders.

Pricing

- Specific annual fee details vary widely (depending on plan) — many early-stage fintechs offer no annual fee or low cost for early accounts.

- Mercury plus: $29.90/month

- Mercury pro: $299/month

Pros

- Well suited for startups who already use Mercury for banking — unified platform.

- Modern fintech features, developer-friendly integrations.

- Good for companies that may outgrow traditional small business cards but aren’t yet spending millions.

Cons

- May not yet have the full depth of automation, rewards or partner ecosystem compared to Brex or Ramp.

- As a newer product, financing limits and underwriting terms may be less predictable.

Why Choose Over Brex

If your company is a tech startup already with Mercury banking, this may offer smoother integration and simpler operations than splitting banking and card providers.

Comprehensive Comparison Table

| Card Name | Annual Fee | Rewards Rate | Welcome Bonus | Credit Check Required | Best For (Use Case) | Key Feature | Major Limitation | Overall Rating (out of 5) |

| Brex Business Card | $0 | Up to 7x points (rideshare), 4x travel, 3x restaurants, 2x software, 1x all other | None (but up to $180,000 in partner offers and discounts) | No personal credit check | High-growth startups with large, recurring spend | No personal guarantee; tailored rewards for business categories | Requires at least $50K–$1M in cash reserves; not available to sole proprietors | 4.5 |

| Ramp Business Card | $0 | Flat-rate 1.5% savings equivalent (via discounts and automation) | None | No personal credit check | Businesses focused on cost control and automation | Expense automation, real-time analytics, unlimited virtual cards | Requires strong cash flow (typically $25K+ balance) | 4.4 |

| Capital One Spark Cash Plus | $150 (refundable if $150K spend/year) | 2% unlimited cash back on all purchases | Up to $4,000 total bonus in first year | Yes | High-spend companies seeking no preset limit | Flat-rate rewards + huge welcome bonus | Requires strong credit; fee only waived with heavy use | 4.3 |

| BILL Spend & Expense (formerly Divvy) | $0 (base plan) | 1.5x–7x (depending on category and repayment terms) | Varies by partnership or referral | Yes (soft pull) | Mid-sized teams needing budget controls | Advanced spend controls, unlimited virtual cards | Limited rewards; less suited for high-volume corporate use | 4.1 |

| UPay Business Card | $0 | 1% fee structure (crypto + fiat hybrid) | None (transparency-based pricing) | No (crypto wallet verification only) | Users focused on global payments and crypto integration | Zero FX fees, real-time exchange rates, crypto-backed spending | Limited adoption in traditional finance ecosystems | 4.5 |

| Chase Ink Business Preferred® | $95 | 3x points on travel, shipping, internet, phone, and advertising (up to $150K/year) | 100,000 bonus points after $8,000 spend in 3 months | Yes | Traditional businesses with travel-heavy expenses | Strong travel perks and transfer partners (via Chase Ultimate Rewards) | Requires personal guarantee and credit check | 4.2 |

| Mercury IO Corporate Charge Card | Varies (often $0–$299 depending on plan) | No standard rewards (focus on spend insights) | None | No personal credit check | Tech startups using Mercury’s banking platform | Integrated banking + charge card for startups | Newer product; limited rewards/perks vs Brex/Ramp | 4.0 |

How to Choose: Decision Framework

Selecting the right business card is more than just comparing reward rates, it’s about aligning the card’s structure with your company’s financial behavior, growth stage, and operational needs.

Below is a strategic decision framework to help you determine which option fits your business best.

Risk Management and Liability

Understanding how much personal risk or liability you’re willing to take can be a decisive factor. Brex, Ramp, and Mercury IO all eliminate personal liability, meaning your business, not you, is responsible for repayment. This is ideal for founders who want to protect personal credit while scaling.

Traditional cards like Chase Ink or Capital One Spark usually require personal guarantees, which could affect your personal credit if payments lapse.

For companies managing multiple subsidiaries or teams, corporate-level liability (as with Brex or Ramp) provides clearer accountability and less administrative burden.

If maintaining a clean separation between personal and business credit is vital, prioritize modern fintech cards over traditional banking options.

Business Size Considerations

The size and structure of your business play a key role in determining the ideal card. Startups and early-stage ventures typically benefit from cards like Brex or Mercury IO, which don’t require a personal guarantee or founder credit check.

These cards assess eligibility based on company cash flow, not personal credit, making them perfect for founders who prefer to separate business and personal finances early.

Mid-sized companies often lean toward BILL Spend & Expense, which provides granular budget controls and multi-user management features. It’s more accessible for firms that may not meet Brex’s $50K minimum but still need strong oversight.

Large or established corporations may find Capital One Spark Cash Plus or Chase Ink Business Preferred® more suitable. These cards offer high spending limits, traditional financial backing, and broad support for enterprise-scale accounting systems.

Industry-Specific Needs

Different industries have different spending patterns and operational priorities. Tech startups and SaaS companies tend to favor Brex and Ramp, which offer rewards on software, digital advertising, and travel — the top three categories for most tech-driven businesses.

E-commerce and logistics firms might benefit from Chase Ink Business Preferred®, thanks to its high rewards for shipping, internet, and advertising expenses.

Fintech and crypto-related businesses can look to UPay Card, which integrates crypto-backed spending and zero cross-border fees, reducing friction for global operations.

Cash Flow Situations

How your company manages liquidity — daily, weekly, or monthly — will strongly influence your choice. Businesses with steady cash flow (like venture-backed startups or SaaS firms) thrive with Brex’s daily auto-pay model, which offers up to 7x rewards but requires automatic repayment.

If your company prefers monthly flexibility, Ramp or Capital One Spark Cash Plus provide charge-style models with no interest and generous repayment terms.

Cash-sensitive firms, especially small and mid-sized ones, benefit from BILL Spend & Expense, which enables tighter cash management through controlled virtual cards and spending limits. Your ideal card should complement your payment rhythm — not complicate it.

International vs. Domestic Use

For companies operating globally, cross-border compatibility and FX transparency are crucial. UPay Card stands out with its zero foreign transaction fees and real-time currency conversion make it ideal for international teams or global suppliers.

Brex and Ramp also charge no FX fees, but their reward categories and systems are more U.S.-centric, limiting value for global purchases.

Chase Ink Business Preferred® provides robust travel protection, insurance, and international acceptance, making it a practical choice for executives who travel frequently.

If your team transacts primarily abroad, prioritize cards with FX fee waivers, multi-currency support, and transparent exchange rates.

Technology Requirements

Modern finance teams rely heavily on automation, integrations, and data analytics. Ramp excels in this area, offering automated expense reporting, vendor optimization, and real-time insights that can save up to 5% on company spending.

Brex also integrates seamlessly with major accounting platforms like QuickBooks, Xero, and NetSuite, syncing transactions in real-time.

Mercury IO and UPay cater to tech-first firms that value API access and integration with digital wallets, payroll systems, and global payment platforms.

If your organization emphasizes efficiency and digital transformation, choose a card with strong automation, analytics, and integration capabilities.

Rewards and Perk Optimization

Lastly, consider whether you prioritize cash-back simplicity or category-based multipliers. Brex shines with its up to 7x points in select business categories — perfect for high spenders on travel, software, and meals.

Capital One Spark Cash Plus delivers 2% flat cash back, simplifying management for companies with diverse expense types.

BILL Spend & Expense and Ramp trade high rewards for operational savings and automation — better for cost-conscious teams than perk seekers.

UPay introduces crypto-based flexibility for international teams — turning digital assets into usable funds seamlessly.

Businesses aiming for simplicity and predictability might prefer flat-rate cash-back cards, while growth-oriented startups seeking to maximize return on specific expense types will gain more from structured rewards like Brex’s.

Final Thoughts

The Brex Business Card continues to position itself as one of the most forward-thinking financial tools for startups in 2025. With no annual fees, no personal guarantee, and category-based rewards on everyday business expenses, it’s built for companies that value automation, transparency, and fast scaling.

Its ecosystem, including smart integrations, real-time expense tracking, and seamless accounting sync, makes it more than just a corporate card; it’s a complete spend-management solution.

It’s a perfect match for funded startups, tech-driven firms, and digital-first businesses that maintain steady cash flow and prefer to keep founders’ personal credit completely separate from company operations.

The combination of automation, global accessibility, and up to 7x rewards on common business categories gives Brex a meaningful edge for companies moving quickly and spending strategically.

Still, Brex isn’t ideal for every business model. Companies with fluctuating cash reserves, those seeking traditional financing flexibility, or sole proprietors who don’t meet Brex’s eligibility requirements may find better options elsewhere.

For example, BILL Spend & Expense offers broader accessibility for smaller teams, while Capital One Spark Cash Plus provides a flat 2% cash back and predictable rewards for established businesses with higher spend capacity.

If we had to name the top alternative, Ramp Business Card would take that spot. It mirrors Brex’s modern, fee-free structure but places stronger emphasis on cost control, automation, and analytics.

Ramp’s commitment to helping businesses reduce unnecessary expenses — rather than just reward spending — makes it an attractive, data-driven option for finance teams seeking efficiency over perks.

Frequently Asked Questions

Is Brex a Good Business Card?

Yes, the Brex Business Card is a good option for well-funded startups and tech-savvy businesses seeking no fees, flexible credit limits, and strong expense management tools, though it’s less ideal for smaller or early-stage companies due to strict eligibility and limited customer support.

Is It Hard To Get a Brex Credit Card?

Getting a Brex credit card isn’t necessarily hard, but it is selective. Brex evaluates your business’s financial health, focusing on factors like revenue, funding, cash reserves, and your bank-linked data, rather than personal credit scores.

What Credit Score Do You Need for Brex?

You don’t need a specific personal credit score to qualify for the Brex Business Card — Brex evaluates your company’s financial health (like cash balance and revenue), not your personal credit score.

What Is Brex Credit Limit?

The Brex Business Card offers dynamic credit limits determined by your company’s financial health, rather than personal credit scores. For monthly payment plans, your credit limit is typically set between 5% and 20% of your aggregate bank balance, based on real-time data from connected accounts .

If you have a Brex business account, your limit can be up to 30% of your account balance. For daily payment plans, limits are based on the cleared balance in your primary Brex business account .

Is Brex a Visa or Mastercard?

Brex is a Mastercard business credit card.