Managing crypto in daily life is still a challenge for many people. You can trade digital assets easily, but when it comes to paying for a coffee or booking a flight, most exchanges don’t make spending straightforward. Crypto cards solve this problem by bridging the gap between digital currencies and real-world payments. They let you use your crypto balance just like a debit or credit card, converting it to fiat instantly at checkout.

Over the past few years, the crypto card market has grown fast. With more people holding Bitcoin, Ethereum, and stablecoins, demand for simple spending tools keeps rising. Reports show that global crypto card transactions have surpassed billions in volume, and major payment networks like Visa and Mastercard now partner with crypto platforms to expand access. These products matter now more than ever because they make crypto practical—not just an investment, but something you can actually use.

BlockCard is one of the leading names in this space. It offers users an easy way to spend crypto anywhere Visa is accepted while earning rewards through its native ecosystem. It’s designed for both casual users and those who want higher cashback through staking.

In this review, we’ll break down BlockCard’s features, fees, and rewards program in detail, and we’ll also look at the best alternatives like Crypto.com, Coinbase Card, and Nexo. You’ll learn how each card works, where they differ, and which one fits your financial goals.

Key Takeaways

- BlockCard allows you to spend cryptocurrency like cash using a Visa debit card.

- You can fund the card with over 15 different cryptocurrencies.

- Cashback rewards range from 1% to 6.38%, depending on the amount of TERN you stake.

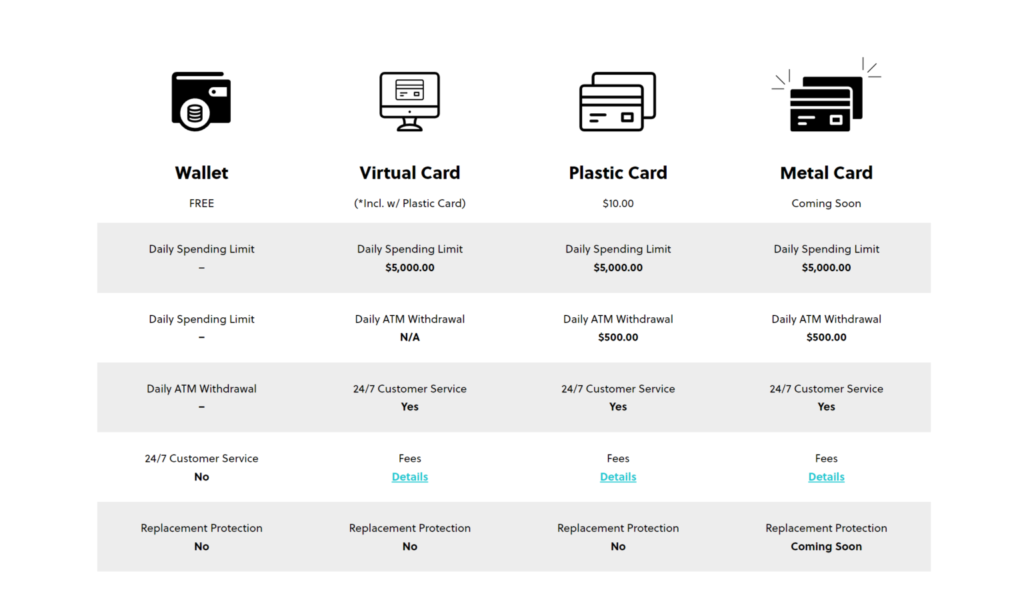

- Both virtual and physical cards are available, with issuance starting at $10.

- BlockCard is issued by Unbanked, a U.S.-based company that complies with KYC/AML rules.

What is BlockCard?

Source: Blockcard Facebook

BlockCard is a crypto debit card that lets users spend their digital assets anywhere Visa is accepted. It works like a regular debit card but draws funds from your crypto balance instead of a traditional bank account. When you make a purchase, your crypto is instantly converted into fiat currency, so you can pay seamlessly in stores or online.

BlockCard is issued by Unbanked, a U.S.-based fintech company focused on building payment solutions for the digital asset economy. The company’s mission is to make crypto practical for everyday transactions, reducing the friction between blockchain technology and traditional finance. Unbanked partners with Visa to ensure global merchant acceptance, making BlockCard usable almost anywhere that supports Visa payments.

The card is designed for people who actively hold or earn crypto and want an easy way to spend it. It fits well for freelancers paid in crypto, investors who use digital assets for daily expenses, or anyone seeking a bridge between their crypto wallet and real-world spending. Unlike credit cards, BlockCard doesn’t rely on credit checks or borrowing. Instead, you preload it with funds from supported cryptocurrencies or stablecoins, maintaining full control over your balance.

What sets BlockCard apart from traditional debit cards is its crypto-first structure. Users can deposit, hold, and spend from multiple crypto wallets within the same account, with automatic conversions handled behind the scenes. It also offers rewards through its native TERN token, giving users cashback based on their spending and staking levels a model not found in conventional banking products.

The platform operates on Unbanked’s proprietary technology, built to support both on-chain and off-chain processing for faster transactions and lower fees. It integrates easily with mobile and desktop dashboards, allowing users to monitor spending, manage crypto balances, and order physical or virtual cards.

As of now, BlockCard is primarily available to residents of the United States, with expansion plans for other regions under review as regulatory conditions evolve. International versions are expected to roll out gradually through regional partnerships.

In short, BlockCard bridges the convenience of Visa payments with the flexibility of crypto ownership. It gives users the ability to live fully in the digital economy without sacrificing real-world usability.

Quick Facts: BlockCard

| Category | Details |

| Card Network | Visa |

| Annual Fee | None (but a $5 monthly maintenance fee applies unless you spend $750+ per month) |

| APR Range | Not applicable (prepaid debit structure, not a credit product) |

| Welcome Offer | None currently offered |

| Rewards Rate | Up to 6% crypto cashback (tiered based on TERN token staking) |

| Foreign Transaction Fees | None reported for international purchases in supported regions |

| Credit Check Required | No |

| Personal Guarantee Required | No |

| Minimum Requirements | Successful KYC verification and initial crypto deposit (amount may vary) |

| Application Timeline | Instant virtual card issuance upon KYC approval; physical card typically arrives within 7–14 days (U.S. only) |

BlockCard’s setup is simple. You complete identity verification, deposit crypto into your wallet, and can start spending almost immediately with the virtual card. The absence of a credit check makes it accessible to more users, while the spending threshold for fee waivers encourages regular activity.

Its tiered reward model is linked to the amount of TERN tokens staked in your account. The more you stake, the higher your cashback rate, reaching up to 6%. Unlike credit cards, there’s no borrowing or interest just a straightforward prepaid system designed for everyday crypto use.

Currently, BlockCard is available to users in the United States, with plans for broader availability as Unbanked expands its partnerships and regulatory coverage.

Features of BlockCard

BlockCard comes with a range of features designed to make spending crypto as easy and familiar as using a traditional debit card.

1. Crypto-to-Fiat Conversion in Real Time

BlockCard’s main strength lies in its ability to instantly convert crypto into fiat at the time of purchase. You can deposit supported cryptocurrencies into your Unbanked wallet, and when you use your card, the system automatically converts what’s needed to complete the transaction. This eliminates the need to manually trade crypto before spending, making daily use fast and convenient.

2. Multi-Currency Support

Users can load a range of cryptocurrencies and stablecoins onto their account, including Bitcoin, Ethereum, Litecoin, and USDC. This flexibility allows people to manage different assets without depending on a single coin. You can also choose which asset to use as your primary funding source, making it easy to control how and when you spend your holdings.

3. Instant Virtual Card + Physical Card Option

Once your KYC is approved, you receive a virtual card that can be used immediately for online payments. If you prefer a physical card, you can order one through your dashboard. The physical card works anywhere Visa is accepted, allowing you to pay at millions of merchants worldwide.

4. Token-Based Rewards

Unlike traditional debit cards that offer fixed cashback in fiat, BlockCard’s rewards system is powered by its native TERN token. Rewards are earned and distributed in crypto, and users can increase their cashback rates by staking more TERN within the platform.

5. User-Friendly Dashboard

The BlockCard dashboard provides a simple interface to manage your spending, deposits, and rewards. You can monitor real-time balances, view transactions, and transfer funds across wallets. The dashboard is accessible via both desktop and mobile browsers, offering flexibility for active users.

6. No Credit Dependency

BlockCard is a prepaid debit card, which means it doesn’t rely on a credit score. There’s no credit check during application, and users don’t accumulate debt. This setup appeals to those who want a crypto-powered card without the obligations of a traditional credit system.

7. Transparent Fee Structure

Instead of charging hidden or complex fees, BlockCard uses a straightforward system: a $5 monthly maintenance fee waived if you spend at least $750 per month. There are no foreign transaction fees, and conversion rates are clearly displayed.

Rewards Program

BlockCard’s reward system is simple but unique. Users earn up to 6% cashback on purchases, paid out in TERN tokens. The exact rate depends on how many TERN tokens you stake on the platform.

The structure is tier-based users who stake higher amounts receive larger cashback percentages. For example, a low staking level might yield around 1% cashback, while higher tiers can go up to 6%. These rewards accumulate automatically and can be redeemed or held within your account.

The TERN token acts as the foundation of BlockCard’s ecosystem. By tying rewards to staking, BlockCard encourages engagement within its network. However, it also means your effective reward value can fluctuate with the market price of TERN.

For everyday users, the program is simple enough: make purchases, earn crypto back, and grow your balance through continued use.

Limits and Controls

BlockCard offers spending and withdrawal limits that vary depending on your verification level and account activity. Basic KYC users typically have lower daily limits, while fully verified users can access higher thresholds.

The card supports daily purchase limits of up to several thousand dollars, along with ATM withdrawals capped at industry-standard amounts. Within your dashboard, you can set spending limits, freeze or unfreeze your card, and track team or family usage.

These built-in controls make the card suitable for both individuals and small teams who want oversight on spending behavior.

Technology Integration

BlockCard runs on Unbanked’s financial infrastructure, which connects blockchain technology with traditional payment networks. Transactions are processed on Visa’s rails, while crypto deposits and conversions occur through Unbanked’s secure platform.

Users can access BlockCard through a clean web dashboard, with features optimized for both desktop and mobile. The interface displays your portfolio, transaction history, and card management options.

The platform also supports API access for developers and businesses who want to integrate crypto-to-fiat payments into their own workflows. This makes BlockCard more than a simple consumer product it can function as a payment solution for projects and small companies operating in the Web3 ecosystem.

Security Features

Security is a priority for BlockCard and Unbanked. The platform uses AES-256 encryption to protect sensitive data, ensuring all communication between users and servers is secure. Account verification follows KYC and AML standards, which help prevent fraud and unauthorized access.

If your card is lost or compromised, you can instantly freeze it from your dashboard. Two-factor authentication (2FA) adds another layer of protection to all account logins and transactions. Additionally, funds are stored in custodial wallets with institutional-grade safeguards.

The partnership with Visa adds further reliability transactions are processed through Visa’s global payment network, backed by their security and fraud monitoring systems.

Additional Benefits

Beyond core functionality, BlockCard provides a few extra perks that enhance the overall experience. These include:

- No foreign transaction fees, making it friendly for travel or international spending.

- Staking rewards, offering an incentive to hold tokens and grow your cashback potential.

- Instant card replacement for lost or stolen cards.

- Ease of funding, since you can deposit a range of popular cryptocurrencies.

While it doesn’t include luxury travel perks or insurance benefits like premium credit cards, its simplicity and low fees make it a strong choice for everyday crypto users.

Fees and Costs

Source: skrumble

Before choosing a crypto card, it’s important to understand all the fees involved, both upfront and ongoing.

The platform is accessible globally and caters to accounts in over 200 countries.

Comprehensive Fee Table

| Annual / Monthly fee | Typical amount | Notes |

| Annual / Monthly fee | $0 annual; $5 monthly (waived if you spend ≥ $750/month) | Monthly maintenance is common; waived with qualifying monthly spend |

| Card issuance | Virtual free; plastic ~$10; metal ~$50 (where offered) | Virtual card is usually instant. Physical plastic has a one-time issuance cost |

| Transaction (point-of-sale) fees | Typically $0 for swipes; $1 domestic PIN; $2 international PIN | POS swipe purchases are usually free, but PIN-based transactions can carry small fixed fees |

| Cash advance / ATM withdrawal | $3.00 domestic; $3.50 international; ATM operator fees may apply | Daily ATM limits apply (commonly ~$500/day). Check local ATM operator charges. |

| Foreign transaction fee | Often built into ATM/international PIN fees; no separate percentage for card swipes reported | International PIN fee covers cross-border PIN transactions; card swipe FX pricing can vary by processor. |

| Late payment / Over-limit fees | Not applicable (prepaid/debit model — no credit line) | Since this is not a credit product, there is no APR, late fee, or over-limit fee typical of credit cards |

| APR | Not applicable | Prepaid/debit style — you are spending your own funds rather than borrowing |

| Hidden/uncommon fees | Small conversion spreads, staking requirements to unlock top rewards, and occasional promotional fees | Some rewards require staking or holding native tokens. Conversion spreads may apply at swap time |

| Application / KYC timeline | Virtual card instant after KYC; physical delivery varies (days to weeks) | Activation and KYC usually quick; mailing time depends on your region. |

What This Fee Picture Actually Looks Like

These cards behave like prepaid debit accounts that use crypto as the source of funds. That changes which fees matter. You do not get an APR or late fee because you are not borrowing money. Instead you face maintenance, ATM, PIN and occasional issuance fees. The most consistent cost across reviewers is a $5 monthly maintenance fee that users can avoid by spending at least $750 in a calendar month. That effectively turns the card into a low-cost option for regular spenders, but it feels like a $60 annual cost if you don’t meet the spend threshold.

ATM and PIN fees are fixed amounts rather than percentage slices. Domestic ATM withdrawals are commonly around $3.00 and international withdrawals around $3.50. Local ATM operators may still tack on their own fee, so the total cash out cost can be higher. For card purchases, most swipe transactions are free, but PIN transactions can carry a $1 or $2 fixed charge depending on location.

Finally, rewards and pricing interact. To earn the highest crypto cashback you often must stake or hold a native token. That creates an implied cost: staking ties up capital and exposes you to token price swings. There can also be small conversion spreads when the platform liquidates crypto at the point of sale. These are less visible but matter when you analyze effective cost and net rewards. If you want, I can pull the latest terms and fee screenshots from the issuer so we can cite exact lines in the T&Cs.

Only TERN, the card’s native token, can be staked to earn rewards, and in funding

Eligibility and Application Process

Source: CaptainAltcoin

Who Can Apply

BlockCard is aimed mainly at individual consumers who hold cryptocurrency and want to spend it like fiat. The product is widely available to residents of the United States, though other regions have seen limited or partner-based rollouts.

It is not a traditional credit product, so typical credit score checks are not required for a standard consumer card. Business or corporate card options exist in some partner programs, but those often follow different onboarding rules and may need additional paperwork.

Required Documents

To open an account, you will need standard KYC documents. Expect to provide a government ID such as a passport or driver’s license, a selfie or live video for identity verification, and a proof of address like a recent utility bill or bank statement.

Some flows may also ask for a Social Security number for US customers to complete identity checks. If you apply as a business, you should be ready with company formation documents, an employer identification number, and proof of beneficial owners.

Step-by-step application guide

- Go to the BlockCard signup page and create an account with your email.

- Complete your profile and enter the personal details the app requests.

- Upload ID and proof of address when prompted. Follow the on-screen selfie or video step for identity verification.

- Fund your BlockCard wallet with crypto or stablecoin. Many users report a small minimum deposit is required to activate the virtual card.

- Once KYC is approved, you will receive a virtual card instantly. Order a physical card from the dashboard if you want plastic.

Approval Timeline

KYC approval and virtual card issuance can be immediate when your documents pass automated checks. That means you can often spend online the same day you sign up. The physical card is mailed and typically arrives within one to two weeks, depending on shipping and your location. If verification fails, expect extra review time or requests for more documents.

What Happens After Approval

After approval, you get instant access to a virtual card to use online. You should link a funding source and deposit crypto into your in-app wallet to make purchases. If you ordered a physical card, it will ship, and you can activate it in the app when it arrives.

You can set your PIN, enable card controls, view limits, and opt into staking or rewards tiers if you want higher cashback. Keep an eye on the app for any limits tied to your KYC level and for messages about eligibility for higher transaction thresholds.

Pros of BlockCard

Here are some of the key advantages that distinguish BlockCard in the rapidly evolving cryptocurrency space.

1. Real‑Time Spending from Crypto

BlockCard lets you spend your crypto instantly without needing to manually convert it into fiat on an exchange. When you swipe the card, the platform automatically converts your crypto into U.S. dollars in real time.

This means you can use it at any place that accepts Visa, whether it’s a coffee shop, grocery store, or online merchant.

For crypto users who want to make everyday purchases directly from their wallets, this is a practical and smooth experience.

2. Cashback Program

With BlockCard, you can earn up to 6.38% in crypto cashback (known as “CryptoBack”) on all eligible purchases. The reward you earn depends on how much of the TERN token you stake on the platform.

For example, if you stake enough TERN to reach the highest tier, you can earn 6.38% back on every transaction. So, if you spend $1,000 a month, you could get back over $60 in crypto rewards. There’s no upper limit, so the more you spend, the more you earn.

3. Multi‑Currency Flexibility

BlockCard supports a variety of popular cryptocurrencies, including Bitcoin (BTC), Ethereum (ETH), Litecoin (LTC), USDC, and several others. You can fund your account using any of these, and they will be automatically converted into TERN for spending.

This gives users the flexibility to manage their preferred crypto assets while still using one unified card.

BlockCard also works with mobile payment platforms like Apple Pay, Google Pay, and Samsung Pay, adding another layer of convenience.

4. Low Conversion Fees (If Applicable)

One of BlockCard’s biggest benefits is its low fee structure for everyday usage. There are no deposit fees, no crypto exchange fees within the platform, and no transaction fees for regular point-of-sale purchases.

This makes spending crypto much more efficient since you’re not constantly losing money to small charges. The only fees you might encounter are for ATM withdrawals or PIN-based transactions, which are clearly listed and reasonable.

Cons of BlockCard

While BlockCard offers several useful features, it also comes with a few weaknesses users should be aware of.

1. Monthly Maintenance Fee

BlockCard charges a $5 monthly maintenance fee if you spend less than $750 per month using the card. This means that unless you’re an active user, the fee can eat into your cashback rewards.

For casual or low-volume users, this is something to watch out for. It can make the card less cost-effective if you only plan to use it occasionally or for small purchases.

2. Limited Jurisdictions

At the moment, BlockCard is only available to users in the United States. While the company has expressed plans to expand to other regions like Europe, there is no clear timeline for this rollout.

This makes the card inaccessible to a large portion of global crypto users who are looking for crypto debit card options. If you’re based outside the U.S., you’ll need to consider alternatives until international support is added.

3. TERN Token Dependency

To use BlockCard effectively and earn rewards, your crypto is automatically converted into TERN, the native utility token of the platform.

This introduces added risk because if the price of TERN drops, the value of your balance may also fall, even if the crypto you originally deposited has gained value.

Also, higher cashback rewards require you to stake a large amount of TERN, which ties up your funds and increases your exposure to that single token’s market fluctuations.

User Reviews and Feedback Analysis

Aggregated Rating

On Trustpilot’s page for “getblockcard.com,” the card has a TrustScore of 2.0 out of 5, based on 29 reviews.

Some users also reference negative sentiment on crypto forums and user aggregators.

Because BlockCard is often discussed in crypto communities, reviews tend to be polarized. Some users praise the concept, others report serious problems.

Common Praise Themes

- App / Interface potential

“The app seems excellent and will perfectly suit my needs, but the support team takes very long to respond.” Trustpilot Several users appreciate the design, usability, and concept behind the wallet + card integration. - Ambitious feature promises

Some early adopters were excited by the idea of spending crypto everywhere with cashback rewards tied to native tokens. BlockCard and Unbanked claim support for 50+ million merchants globally via Visa rails.

In other words, the vision and possibility resonate with users who want crypto to function like traditional money.

Frequent Complaints

- Funds not appearing / conversion loss

Many users state that when they deposited crypto, the credited amount was far less than expected. One user said:

“I deposited 5000 USDT, credited 4320 USDT. BlockCard is a complete scam.” Trustpilot

Others say their balances were converted into the TERN token at unfavorable rates without clear disclosure.

- Unresponsive or poor customer support

Many complaints center on support being slow or ignoring users:

“After depositing your BTC, you never get the funds in your account. When you contact support they just tell you that they sent it to technical and then ignored all your subsequent emails.”Trustpilot This is echoed in reviews about Unbanked (the backend):

“The app seems excellent … but the support team takes very long to respond. I submitted questions a week ago and still no reply.”Trustpilot

- Geographic limitations and service availability

Some users from outside the U.S., especially in Europe, complain they couldn’t get the physical card or even activate the account:

“I opened an account and made the requested deposit to order the card. Only to understand that no card is available here in Europe. Since then I can not login anymore.”

Customer Service Feedback

Based on user reviews, customer service is a major weak point. Many say support tickets go unanswered or that response times stretch for days or weeks. In some cases, users say their accounts were locked or access was lost after depositing funds with no further follow-up.

One user acknowledged a quick initial support response about a deposit issue, but said they were never given full clarity on how their funds were allocated or converted.

Top 8 Alternatives to BlockCard

Here’s the thing. BlockCard is a solid crypto debit option, but it is not the only way to spend crypto in the real world. You might want lower fees, better rewards, wider global support, bank-grade features, or simpler tokenless rewards. This section covers eight practical alternatives across different categories: direct competitor, premium, budget, fintech/bank, niche, and a neutral look at UPay.best.

Each pick includes what it’s best for, what makes it different, the main pricing points, three pros, two cons, and why someone might pick it over BlockCard.

Coinbase Card Issuer: Coinbase / Cardless, Inc.

Best for

Users who want simple, tokenless crypto rewards and tight integration with a major exchange.

Key differentiators

Coinbase pays rewards in crypto (bitcoin or other assets) without requiring token staking. It integrates directly with your Coinbase account and supports instant virtual card issuance for online spending. The program aims to avoid foreign transaction fees and leans on Coinbase’s compliance and fiat onramps.

Pricing

No annual fee for many versions; no foreign transaction fees claimed on some card products; specific reward tiers vary by region and Coinbase account holdings. Check Coinbase’s card page for the latest launch terms and issuer notices.

Pros

- Clear, exchange-backed onboarding and fiat rails.

- Crypto rewards paid in established assets, not a volatile native token.

- Virtual card often available instantly after approval.

Cons

- Reward rates tend to top out lower than token-staking models.

- Some features and issuer partners differ by country.

Why choose over BlockCard

If you want rewards paid in mainstream crypto without staking and prefer the safety of a top exchange, Coinbase gives that cleaner path.

Crypto.com Visa: Issuer: Crypto.com / Visa

Best for

Power users who want high-tiered rewards, travel perks, and bundled app services.

Key differentiators

Crypto.com uses a tiered model tied to CRO staking to unlock higher cashback, airport lounge access, and subscription rebates. It has historically offered premium metal cards and travel benefits that resemble higher-end rewards cards in traditional finance. The platform bundles exchange, staking, and card services into one app.

Pricing

No annual fee on base tiers; higher tiers require staking CRO, which is an opportunity cost. ATM and conversion fees vary by tier and country. Card issuance may have a one-time fee for physical metal cards.

Pros

- Very high advertised cashback for top stakers.

- Travel-focused perks and subscription rebates.

- Strong global presence in many markets.

Cons

- Requires staking a native token to get the best perks.

- Program complexity can hide effective costs (staking risk, lock-ups).

Why choose over BlockCard

Pick Crypto.com if you want travel benefits and you are comfortable locking CRO for higher rewards.

BitPay Card: Issuer: BitPay / Visa or Mastercard partners

Best for

Users who want a simple, low-fee US-focused crypto debit experience.

Key differentiators

BitPay emphasizes straightforward spend-from-wallet mechanics and a simple fee structure. It supports many major coins and offers easy top-ups from your wallet to a card balance. Historically, it had low to no monthly fees and clear POS mechanics. Note: product availability and terms can change.

Pricing

Historically low/no monthly fees and predictable ATM withdrawal charges. Conversion fees and certain transaction fees may apply; check BitPay’s pricing page for the latest.

Pros

- Simple, well-documented fee model.

- Wide coin support and easy wallet linking.

- Good option for US residents who need a basic spend card.

Cons

- Availability varies regionally, and features have paused or shifted in the past.

- Rewards are modest compared with tokenized models.

Why choose over BlockCard

If you want a no-frills prepaid card with predictable costs and wide coin support, BitPay is a straightforward alternative.

UPay.best Card: Issuer: UPay Technology Ltd.

Best for

Users looking for a global, low-fee crypto card with collateralized credit and regional currency support.

Key differentiators

UPay.best positions itself as a global crypto card solution that supports multiple fiat currencies, instant collateralized spending (use crypto as collateral to gain spending limits), and a mix of virtual and physical tiers. It targets users who want basic loans, savings, and card spending in one app. The platform has grown marketing and product pages since 2024 and emphasizes low ATM and transaction fees.

Pricing

UPay advertises low transaction fees and modest ATM fees (site claims around 2% for ATM withdrawals). Card issuance and tiered limits vary by region and selected card type. Confirm regional specifics on UPay’s official pages.

Pros

- Instant collateralized spending keeps users from liquidating long-term positions.

- Multiple fiat currency-support for international travel.

- Competitive-fee messaging and flexible card tiers.

Cons

- Newer player with less transparent global licensing history compared with major exchanges.

- Regional support and protections may not match established incumbents.

Why choose over BlockCard

If you want a newer option that emphasizes collateralized credit and low fees for global travel, UPay is worth evaluating, just confirm compliance and local support first.

Wirex: Issuer: Wirex / Visa or Mastercard partners

Best for

Users seeking steady cryptoback rewards and fee-free ATM access in modest monthly bands.

Key differentiators

Wirex offers Cryptoback rewards that are straightforward and not strictly tied to a volatile native token for baseline plans. It often provides fee-free ATM withdrawals up to a monthly limit and has multiple fiat rails for global spending. The app supports multiple tiers and a user-friendly card control suite.

Pricing

Free base plan with optional paid plans that increase Cryptoback rates and benefits. ATM fee-free band and tiered subscription options. Exact fees and perks vary by region and plan.

Pros

- Hands-on app controls and in-app exchange.

- Clear cryptoback mechanics and a monthly fee-free ATM allowance.

- Multiple currency support for travelers.

Cons

- Top rewards often tied to paid plans.

- Regional features and limits can vary, complicating comparison.

Why choose over BlockCard

Wirex is a good pick if you want predictable cryptoback and low ATM costs without complex staking requirements.

Nexo Card: Issuer: Nexo

Best for

Users who want credit-like flexibility and cashback tied to asset-backed credit lines.

Key differentiators

Nexo offers a hybrid model where your assets can underwrite a credit line, enabling card spending in credit mode while preserving long-term positions. Cashback is often paid in NEXO token or major cryptos, and higher balances unlock better rates. The card is attractive for those who want borrowing options instead of immediate liquidation.

Pricing

No annual fee for many base use cases; cashback and borrowing costs vary with mode selected (debit vs. credit). Terms include credit line interest if you borrow against collateral.

Pros

- Ability to spend without liquidating assets via credit mode.

- Rewards paid in crypto with flexible redemption options.

- Strong integration with Nexo borrowing and savings products.

Cons

- Using credit mode creates interest obligations and complexity.

- Top benefits require holding a significant asset balance on the platform.

Why choose over BlockCard

If you want to keep long-term positions while still accessing liquidity via a card, Nexo offers a distinct asset-backed credit route.

Binance Card: Issuer: Binance / Visa or Mastercard

Best for

Active exchange users who want to spend exchange balances directly and earn modest cashback.

Key differentiators

Binance lets you spend many exchange-supported assets directly. It’s designed for heavy exchange users and ties card rewards and limits to your Binance account status. The card often supports several stablecoins and native tokens for seamless on-platform spending. Note: Binance Card availability varies by country and regulatory constraints.

Pricing

Cashback up to about 2% commonly advertised. Fees and availability depend on region; Binance restricts US availability but has a wide reach elsewhere.

Pros

- Tight integration with Binance balances and easy funding.

- Accepts many tokens and stablecoins for payments.

- Good for users already active on Binance.

Cons

- Not available in all regions, notably restricted in the US for parts of the program.

- Lower cashback ceiling than some token-staking programs.

Why choose over BlockCard

Choose Binance if you already use Binance heavily and want seamless spending from exchange balances with modest cashback.

Revolut Crypto Card: Issuer: Revolut (bank/fintech)

Best for

People who want a full fintech bank experience with optional crypto spending.

Key differentiators

Revolut blends bank-like features, multi-currency accounts, and optional crypto trading into one app. You can spend crypto balances through the Revolut card, which auto-converts crypto to the needed fiat. Revolut is built for travelers and those who want an all-in-one money app with crypto as an add-on.

Pricing

Revolut uses a tiered subscription model. Base accounts often have no annual fee, with paid plans that reduce exchange fees and increase allowances. Crypto trading fees depend on plan and volume. Card fees and ATM allowances vary by plan.

Pros

- Full fintech banking features with built-in multi-currency and card controls.

- Easy travel-friendly features and fiat account rails.

- Optional crypto spending without separate crypto-card onboarding.

Cons

- Crypto functionality is not as focused as pure crypto-card issuers.

- Some features depend on subscription tiers.

Why choose over BlockCard

If you want a broader banking app that includes crypto as part of everyday finance, Revolut gives a tighter bank-like experience.

Comprehensive Comparison Table

| Card Name | Annual Fee | Rewards Rate | Welcome Bonus | Credit Check Required | Best For (Use Case) | Key Feature | Major Limitation | Overall Rating (out of 5) |

| BlockCard (Unbanked/Ternio) | $0 annual; $5 monthly if you don’t meet the $750/mo spend waiver | Up to ~6% crypto cashback (tiered / token-linked) | Typically none disclosed | No | Crypto holders who want a Visa debit-style card with token rewards | Tokenized, tiered cashback; instant virtual card | Rewards and value tied to native token / staking complexity | 3.8 |

| Coinbase Card | $0 (no annual fee) | Up to 4% back (paid in crypto; varies by holdings) | Varies by region / promotions | No (not a credit product) | Users who want simple, exchange-backed crypto rewards | Direct Coinbase account integration and crypto rewards in mainstream assets | Reward ceiling lower than some staking models | 4.0 |

| Crypto.com Card | $0 base; premium card tiers require CRO staking or subscription | Up to 5–6% back (tiered; top tiers require CRO stake or subscription) | Region dependent; promo offers occasionally | No | Power users who want high tiered rewards and travel perks | High tier benefits (lounge access, subscription rebates) when staking CRO | Requires staking / lockups for best perks | 4.1 |

| BitPay Card | $0 annual (historically); low predictable fees | Modest cash back on some merchants (varies) | Rare/none | No | Low-friction spend-from-wallet card for US users | Simple wallet-to-card mechanics and predictable fees | Lower or no tokenized reward upside | 3.6 |

| Wirex | $0 base; paid plans exist for higher benefits | Up to 8% Cryptoback on top paid tier; base rates lower | Occasional promos | No | Users seeking steady cryptoback and travel-friendly features | Cryptoback rewards and fee-tiered subscription plans | Cryptoback rewards and fee-tiered subscription plans | |

| Nexo Card | $0 annual; no monthly fee | 0.5–2% (varies by loyalty tier; NEXO token or BTC options) | Usually none | No (debit/credit hybrid mode differs) | Users who want credit-like flexibility without selling holdings | Asset-backed credit mode that lets you spend without immediate liquidation | Using credit mode incurs interest; complexity in modes | 4.0 |

| Binance Card | $0 annual | Up to ~2% cashback (typical) | Occasionally promoted | No | Active Binance users who want to spend exchange balances | Native exchange balance spend; easy funding from Binance wallet | Availability restricted in some regions (eg US limits) | 3.7 |

| Revolut (crypto-enabled) | $0 base; subscription tiers with fees | Crypto trading rewards / plan-dependent perks | Varies by plan | Possible identity checks (banking product) | Users who want bank-like app plus optional crypto | Multi-currency accounts, banking features plus crypto | Crypto feature set secondary to banking; regional restrictions | 4.0 |

| UPay.best Card | Varies: some tiers have activation/collateral fees (eg sample platinum shows activation ~100 USDT) | Varies by card/tier (reviews list tiered ATM and spending fees; rewards differ) | Varies by promotion | No (debit/collateral model) | Users seeking collateralized card options and multi-fiat support | Collateralized instant spending and multi-fiat support | Newer player; regional licensing and transparency differ vs large incumbents |

How to Choose: Decision Framework

Here’s the thing. Choosing a crypto card isn’t about finding the “best” one overall—it’s about finding what fits how you actually spend, move money, and manage assets. Below is a practical decision framework that helps you match your lifestyle, business model, or financial priorities to the right card.

Spend Crypto Easily Without Staking or Credit Checks: Coinbase Card and BitPay Card

If your goal is simplicity, both the Coinbase Card and the BitPay Card are strong options. They let you spend crypto directly without staking tokens or going through credit checks. You can fund them from your wallet, complete verification, and start spending almost immediately.

These cards are ideal for freelancers, traders, and casual crypto users who want predictable fees and low maintenance. Coinbase Card connects straight to your Coinbase balance, while BitPay integrates smoothly with its wallet. Both prioritize ease of use over complex reward structures, making them perfect for everyday spending.

Earn High Rewards with Token Staking: Crypto.com Card and BlockCard

If you’re comfortable staking native tokens, Crypto.com and BlockCard both offer higher reward potential. Cashback rates can reach 5–6% for top tiers, depending on how much CRO or TERN you lock in.

This setup works best for users who already hold or trade these tokens. You’ll benefit from strong rewards, exclusive perks, and access to premium benefits. However, remember that staking ties up funds and exposes you to token price fluctuations. For active crypto investors, though, these cards turn regular spending into an extra yield opportunity.

Spend Without Selling Your Crypto Holdings: Nexo Card and UPay.best Card

For users who prefer to keep their crypto invested, Nexo and UPay.best make that possible. They let you use your holdings as collateral for a credit line, so you spend fiat while your crypto stays intact.

This approach avoids triggering taxable events and gives you instant liquidity. It suits long-term holders, DeFi participants, and investors who see crypto as an asset, not just a payment method. You maintain exposure to potential market gains while gaining real-world spending power.

Manage Variable Cash Flow or Multiple Users: Wirex and Revolut

Wirex and Revolut stand out for users running small teams or businesses with fluctuating cash flow. Both platforms support multi-user management, spending limits, and built-in analytics for tracking expenses.

These features simplify accounting and financial control, especially for startups and remote teams. You can fund the account with crypto or fiat, issue cards to team members, and manage everything from one dashboard. They bridge the gap between consumer convenience and business-grade tools.

Operate Internationally or Travel Often: Wirex, Revolut, and Crypto.com

If you spend across borders, these cards offer the flexibility you need. They support multiple currencies, competitive exchange rates, and global merchant acceptance.

You can withdraw local cash, pay in different currencies, and earn rewards while traveling. For remote professionals, frequent travelers, or global businesses, they reduce friction between fiat and crypto spending. Plus, foreign transaction fees are often lower than what traditional banks charge.

Prefer a Traditional or Bank-Linked Experience: Revolut and Coinbase Card

Revolut and Coinbase Card combine the familiarity of traditional banking with crypto functionality. They partner with regulated banks, offer built-in fiat accounts, and keep compliance standards high.

You can deposit fiat, buy or sell crypto, and use one card for both worlds. This setup is ideal for users who want crypto access without leaving the structure of a trusted financial institution. It’s also useful for newcomers who value stability and transparent regulation.

Work in a Niche or Emerging Industry: UPay.best and BlockCard

For those in emerging Web3 sectors, these two cards offer flexibility. They support multiple tokens, stablecoins, and regional fiat options, making them versatile for different ecosystems.

If you’re earning from NFT sales, DeFi projects, or small crypto-based ventures, these cards let you spend income without converting through multiple exchanges. They serve as bridges between digital revenue streams and everyday transactions, keeping things simple for creators and small projects.

Final Verdict

BlockCard stands out as a simple, practical option for people who want to use their crypto for everyday spending without overcomplicating things. It works like a standard debit card but connects directly to your crypto wallet, letting you convert digital assets into fiat instantly. The setup is easy, the fees are transparent, and you can earn cashback rewards tied to your token tier.

It’s most appealing to users who already hold crypto and want a convenient way to spend it on regular purchases, from groceries to travel. The platform’s partnership with Visa also gives it broad merchant acceptance, which makes it easy to rely on as a daily card.

That said, BlockCard isn’t for everyone. If you’re looking for premium perks, travel rewards, or flexible staking options, Crypto.com or Nexo Card may serve you better. Those who want a simple, exchange-backed experience might prefer Coinbase Card, while users focused on global use cases and multi-currency control may find Wirex or Revolut more suitable.

Generally, BlockCard holds a steady middle ground in the market it’s not the flashiest, but it’s reliable and direct. Its biggest advantage is simplicity: no complex reward structures, no excessive fees, just straightforward crypto spending.

The top alternative worth considering is the Crypto.com Visa Card because it offers stronger reward potential, broader international reach, and a more developed ecosystem for users who want extra earning power. In short, BlockCard’s value lies in accessibility. It’s best for crypto users who care more about convenience and usability than chasing top-tier rewards or exclusive perks.

Frequently Asked Questions

1. Is BlockCard a legit crypto debit card?

Yes, BlockCard is a legitimate crypto debit card issued by Unbanked, a U.S.-based fintech company that complies with KYC/AML regulations.

2. Does BlockCard charge a monthly fee?

Yes, BlockCard charges a $5 monthly maintenance fee if you spend less than $750 per month using the card.

3. What cryptocurrencies does BlockCard support?

BlockCard supports over 15 cryptocurrencies, including Bitcoin (BTC), Ethereum (ETH), Litecoin (LTC), USDC, and Tether (USDT), which are all converted to TERN for spending.

4. Can I use the BlockCard for ATM withdrawals?

Yes, you can withdraw cash from ATMs using the physical BlockCard, but a $3 fee applies for domestic withdrawals and $3.50 for international ones.

5. Who is BlockCard designed for?

BlockCard is designed for crypto users who want to use their digital assets for everyday purchases without needing to convert to fiat manually.

6. Does BlockCard work internationally?

Yes, BlockCard can be used globally wherever Visa is accepted, but the physical card must be issued to a U.S. resident at this time.

7. How do I order a BlockCard?

To order a BlockCard, sign up at the Unbanked website, complete the KYC verification, and choose between a virtual card (free) or a physical card (starting at $10).