The Busha Card gives you several ways to spend your crypto digitally by converting it to fiat instantly through a virtual USDC-linked Mastercard. It’s designed for users who want a seamless bridge between digital assets and everyday spending, from online shopping to paying bills, without the delays or complexities often tied to traditional banking systems.

As crypto adoption grows across Africa, access to reliable spending solutions has become increasingly important. Many users now seek cards that simplify how they use their crypto holdings, not just for trading, but for real-world payments.

The Busha Card responds to this need by offering an easy, fast, and secure way to convert crypto into spendable value, giving users more control and flexibility over their digital funds.

In this review, we’ll explore what the Busha Card offers, including its setup process, supported assets, fees, and user experience. We’ll also highlight where it performs best, and where it may fall short, to help you assess if it fits your spending habits and financial goals.

Additionally, we’ll compare it with 7 strong alternatives such as the Binance Card, Bitnob Card, and others that provide similar or broader crypto-to-fiat capabilities. This comparison will help you identify which card aligns most closely with your lifestyle and budget.

By the end of this review, you’ll understand the Busha Card’s full potential, its advantages, possible drawbacks, and how it stacks up against competing crypto cards in 2025.

Key Takeaways

- The Busha Card enables seamless USDC spending through a virtual Mastercard with zero transaction fees.

- It’s ideal for crypto users in Nigeria, Ghana, and Kenya who primarily make online payments or subscriptions.

- Users can create up to 10 virtual cards with no transaction or monthly fees.

- Its biggest limitation is the lack of physical card access and support for in-person or ATM transactions.

- The review covers seven credible alternatives offering different benefits for global or niche users.

- The Binance Card emerges as the best alternative for users seeking worldwide acceptance and crypto rewards.

- The card integrates smoothly with platforms like PayPal and Wise, expanding its global usability.

What is Busha Card?

The Busha Card is a virtual USDC-powered Mastercard that allows users to spend cryptocurrency directly, just like traditional money.

Issued by Busha, one of Africa’s most trusted and fast-growing crypto platforms, the card simplifies digital payments by converting USDC (USD Coin) into fiat currency instantly at the point of purchase. This makes it an efficient bridge between crypto ownership and everyday financial use.

Busha, established in Nigeria, has built a strong reputation for providing secure crypto trading, savings, and payment solutions tailored to the African market. The Busha Card extends this mission by offering users a practical tool for real-time spending.

It’s issued directly through the Busha app, allowing users to manage their wallet, monitor balances, and control transactions all in one place.

The card primarily targets crypto users in Nigeria and other African countries who want a faster, easier way to spend their digital assets. Whether you’re paying for streaming subscriptions, online courses, e-commerce purchases, or app services, the Busha Card offers a seamless experience that removes the friction of manual conversions or third-party exchanges.

Unlike traditional debit or credit cards linked to bank accounts, the Busha Card connects directly to your crypto wallet balance, offering instant USDC-to-fiat conversion for every transaction. This eliminates the need for long withdrawal processes and makes it ideal for users who prefer to keep their value in crypto but still need spending flexibility.

Currently available as a virtual card, it supports all online platforms and merchants that accept Mastercard payments globally.

With its stablecoin integration, secure digital issuance, and broad acceptance, the Busha Card represents a modern, efficient way for African crypto holders to participate in the global economy, using digital assets for real-world payments without geographical or currency limitations.

Quick Facts Table

| Category | Details |

| Card Network | Mastercard |

| Card Type | Virtual Prepaid Crypto Card (USDC-linked) |

| Issued By | Busha (Nigeria-based crypto platform) |

| Annual Fee | None |

| APR Range | Not applicable (Prepaid card, no credit line) |

| Welcome Offer | None currently offered |

| Rewards Rate | Up to 5% cashback on voucher purchases and 2% on airtime/data via Busha Spend |

| Foreign Transaction Fees | None (USDC is converted directly to fiat at point of sale) |

| Credit Check Required | No |

| Personal Guarantee Required | No |

| Minimum Requirements | Busha account + basic KYC (ID, selfie, proof of address) |

| Application Timeline | Instant digital issuance after KYC approval |

| Supported Regions | Nigeria, Kenya, Ghana |

| Supported Currency | USDC (USD Coin) |

| Spending Type | Online and mobile payments (virtual Mastercard) |

| Conversion | Instant USDC-to-fiat conversion at checkout |

Key Features of the Busha Card

The Busha Card is designed with convenience, cost-efficiency, and regional relevance in mind, making it a strong option for crypto users who want to spend their digital assets with ease.

Here’s a detailed look at its key features:

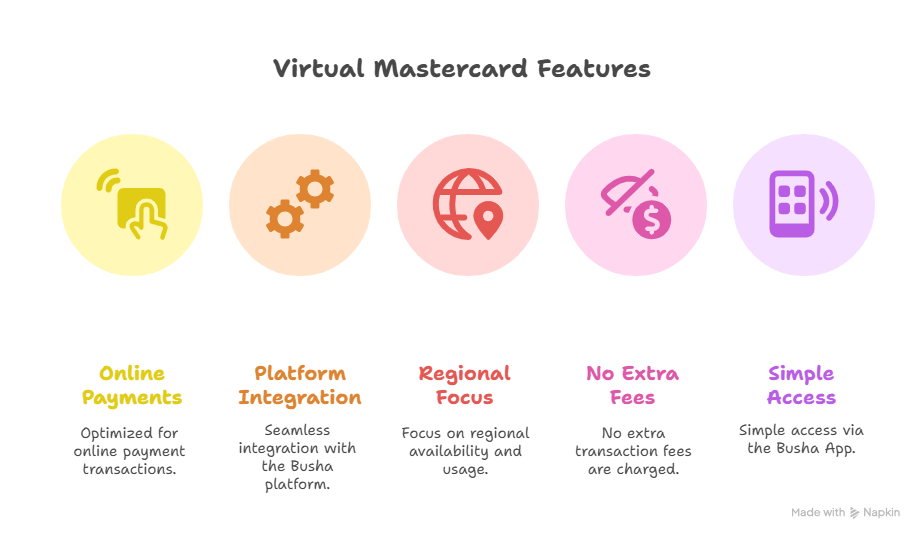

Virtual USDC-Linked Mastercard

The Busha Card is a virtual Mastercard that connects directly to your USDC balance on the Busha platform.

This setup enables instant crypto-to-fiat conversion, allowing you to make online payments for goods and services without delays or manual conversions. The card is optimized for fast, secure online payments, making it ideal for e-commerce and digital subscriptions.

Optimized for Online Payments

The card is built specifically for online transactions, supporting everything from global shopping platforms to streaming services. While it does not currently support in-store or physical POS payments, its seamless online functionality makes it highly practical for digital spending.

Platform Integration

One of the notable features of the Busha Card is its integration with major global platforms, including PayPal and Wise. This expands your ability to fund accounts, send money, and make payments across borders with ease—all from your USDC balance.

Regional Focus and Availability

The Busha Card is tailored for users in Africa, with a primary focus on Nigeria, Kenya, and Ghana. Its availability in these countries aligns with the growing demand for crypto-based financial tools that address local limitations in international payments.

No Extra Transaction Fees

Another significant benefit is that the card charges no additional transaction fees. This makes it cost-effective for users who want to make multiple online purchases or subscriptions without worrying about hidden charges. It’s a straightforward crypto-spending solution with transparent pricing.

Simple Access via the Busha App

Managing your Busha Card is done entirely through the Busha app, where users can activate their card, view transaction history, and monitor their USDC balance. This seamless integration ensures a smooth experience from funding to spending.

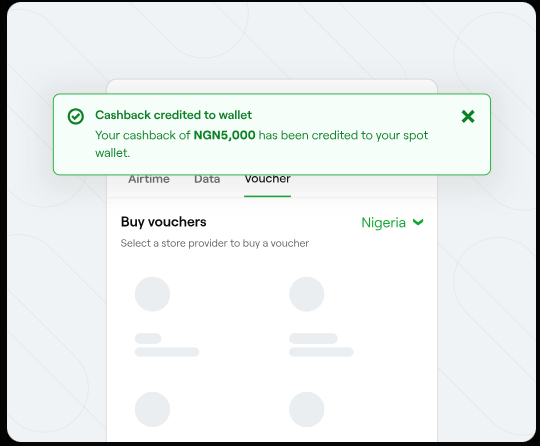

Rewards Program

Alt text: Cashback page on the Busha platform

The Busha Card includes a straightforward and user-friendly rewards program designed to give users additional value each time they transact through Busha Spend — the platform’s integrated payment service.

While it’s not a traditional credit card points system, it provides instant cashback that encourages regular use and easy tracking.

The rewards program is directly tied to spending activity within the Busha app. Users who make payments for eligible products and services, such as airtime, mobile data, or vouchers, automatically receive cashback rewards.

These rewards are credited instantly after each qualifying transaction, making it easy to see earnings accumulate in real time.

There’s no enrollment process — once your Busha Card and Busha Spend accounts are active, you’re automatically eligible to earn rewards.

Rates

The cashback rates are simple and transparent:

- 2% cashback on all airtime and data purchases

- 5% cashback on all voucher purchases

These rates are competitive for a crypto-linked payment service, offering tangible returns on everyday spending without the need for staking or locking up assets.

Redemption

Cashback rewards are deposited directly into the user’s Naira wallet within the Busha app. From there, they can be withdrawn, saved, or reused for new transactions, all without fees or waiting periods. The rewards system is fully digital, and users can track both spending and cashback history in real-time through the in-app dashboard.

Limits and Controls

The Busha Card operates under a structured verification system that determines transaction limits and access levels, ensuring both security and compliance with regional financial regulations.

These limits are based on the user’s KYC (Know Your Customer) verification level and apply to both crypto and fiat transactions conducted through the Busha app.

Verification Levels and Transaction Limits

Level 1:

- Deposits: Unlimited crypto and fiat deposits

- Withdrawals: Not permitted for either crypto or fiat

This level provides basic access for users who have completed minimal verification, suitable for exploring the platform but without full transactional privileges.

Level 2:

- Deposits: Up to ₦10,000,000 per month

- Withdrawals: Up to ₦10,000,000 per month

At this level, users gain full functionality for everyday crypto and fiat transactions, ideal for moderate spending and card usage.

Level 3:

- Deposits: Up to ₦500,000,000 per month

- Withdrawals: Up to ₦500,000,000 per month

This tier is tailored for advanced users or businesses with high-volume transaction needs, granting the highest operational flexibility.

Card Controls

Users maintain complete control of their Busha Card directly from the mobile app. Key management options include:

- Setting spending limits to manage budgets effectively

- Freezing or unfreezing the card instantly for security

- Viewing transaction history and cashback earnings in real time

These built-in controls enhance transparency and safety, giving users confidence when transacting. Combined with Busha’s tiered verification limits, the system ensures secure, compliant, and flexible use of the Busha Card for both individual and business purposes.

Technology Integration

The Busha Card is built on a strong technological framework that connects crypto finance with real-world usability. Its design emphasizes seamless integration across devices, apps, and payment networks — allowing users and businesses to transact efficiently and securely.

Mobile App Integration

The Busha Card operates entirely through the Busha mobile app, available on both the Apple App Store and Google Play Store.

Within the app, users can manage their USDC balance, fund their card, monitor transactions, and redeem cashback rewards. The interface provides a unified dashboard for crypto spending, saving, and investing, ensuring that card management feels as intuitive as using a traditional banking app.

All transactions are synchronized in real time, giving users instant visibility into spending activity and wallet balances.

API and SDK Suite

Busha offers a robust API and SDK suite that enables developers and businesses to integrate digital asset payments directly into their systems. Through these APIs, companies can accept and manage crypto transactions, facilitate crypto-to-fiat conversions, and even embed Busha’s payment infrastructure into their applications.

This technology allows for the creation of custom financial experiences, including issuing digital dollars, automating liquidity management, and supporting cross-border payments, all through a secure and developer-friendly interface.

Busha Prime and Exchange Integration

For enterprises and merchants, Busha Prime enhances cross-border payment capabilities, providing access to multiple fiat corridors including the US, UK, EU, Africa, and Asia. Businesses can leverage this infrastructure to execute large transactions or manage global financial operations efficiently.

Meanwhile, the Busha Exchange integrates seamlessly with the card, enabling users to buy, sell, or swap crypto instantly and fund their Busha Card without leaving the platform.

Security Features

Security is a core part of the Busha Card experience, with multiple safeguards designed to protect users’ funds, data, and transactions. The platform implements strong verification, encryption, and monitoring systems to ensure safe crypto-to-fiat payments at all times.

Two-Factor Authentication (2FA)

Busha employs two-factor authentication (2FA) to secure user accounts and prevent unauthorized access. Every login or sensitive transaction requires an additional verification step, typically through an authentication app or SMS, ensuring that only the account owner can authorize actions on their Busha account and card.

KYC Verification and Tiered Access

All users must complete Know Your Customer (KYC) verification before accessing Busha Card services. This process helps confirm identity, prevent fraud, and comply with financial regulations. Each KYC level defines specific transaction limits, providing an extra layer of control and accountability.

Encryption and Data Protection

User information and transaction data are protected with bank-grade encryption protocols, ensuring that sensitive details remain secure during transfers and storage. Busha’s infrastructure follows global data security standards to maintain privacy and integrity.

Card Controls and Monitoring

Within the Busha mobile app, users can freeze or unfreeze their card instantly if suspicious activity is detected. The app also provides real-time transaction alerts, allowing users to track spending and detect anomalies early.

Vulnerability Disclosure and Support

Busha encourages responsible reporting of potential security issues. Users or developers who identify a vulnerability can reach out through the Help Centre, where the Busha Security Team reviews and addresses reports promptly.

Additional Benefits

The Busha Card offers more than just crypto spending convenience; it combines practical features and financial advantages that make it a valuable tool for everyday use. From zero transaction fees to wide merchant access, the card enhances the overall digital payment experience for users across Africa.

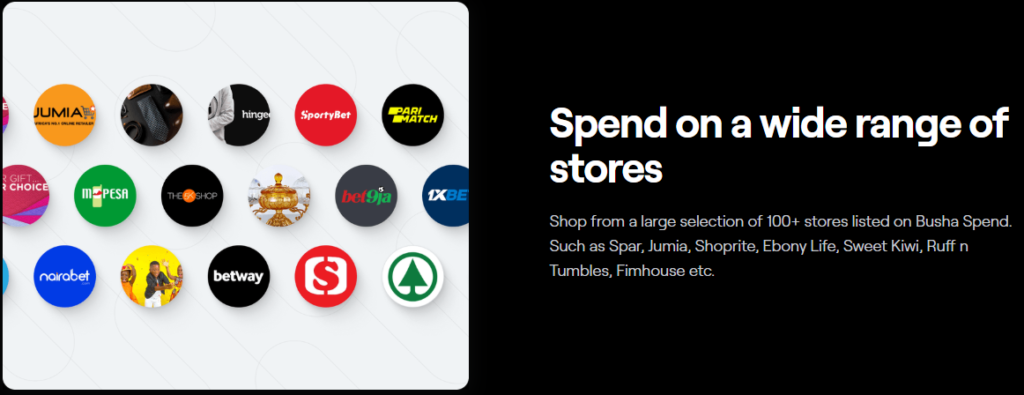

Wide Merchant Access

With Busha Spend, users can shop from over 100 partnered stores, including popular brands such as Spar, Jumia, Shoprite, Ebony Life, Sweet Kiwi, Ruff ’n’ Tumble, and Filmhouse. This extensive network allows cardholders to use their crypto assets for groceries, entertainment, dining, fashion, and more, directly from their Busha wallet.

Instant, Fee-Free Spending

Transactions on Busha Spend are processed instantly and come with zero conversion charges or transaction fees. Users can spend crypto assets such as USDC, Bitcoin, and Ethereum seamlessly without worrying about additional costs or delays, making the Busha Card a cost-effective payment option.

Extensive Asset Support

Busha supports over 45 digital assets, giving users the flexibility to choose which cryptocurrencies to fund their card or wallet. This broad range ensures users can diversify how they manage and spend their holdings.

No Credit Checks or Hidden Requirements

Since the Busha Card operates as a prepaid crypto card, there are no credit checks or complex approval processes. Anyone with a verified Busha account can start using it, making it accessible to a wider audience seeking simple entry into crypto-based payments.

Favorable Exchange Rates and Regulation

Busha offers some of the lowest USD–NGN exchange rates in the market and operates as a regulated financial service provider, ensuring transparency and compliance with local and international standards.

Fees and Pricing Structure

| Fee Type | Cost / Description |

| Annual / Monthly Fees | Free |

| Transaction Fees | Free |

| Cash Advance Fees | Not Applicable — The Busha Card is a virtual prepaid card and does not support cash withdrawals or advances. |

| Late Payment Fees | Not Applicable |

| Over-Limit Fees | Not Applicable |

| Foreign Transaction Fees | Free |

| Hidden or Uncommon Fees | None |

The Busha Card follows a clear and transparent pricing structure designed to make crypto spending simple and affordable. Since it functions as a virtual prepaid Mastercard linked to USDC, users avoid many of the traditional costs associated with credit or debit cards.

Below is a breakdown of the major fee categories and how Busha handles them.

Annual or Monthly Fees

The Busha Card has no annual or monthly maintenance fees. Users can create and maintain their virtual card at no cost, making it one of the most accessible crypto-to-fiat spending tools available in Nigeria, Kenya, and Ghana.

Transaction Fees

All online Mastercard transactions made with the Busha Card are free of charge. Whether you’re paying for subscriptions, shopping online, or purchasing digital vouchers, there are no hidden charges or extra deductions at checkout.

Cash Advance Fees

Because the Busha Card is a virtual card and not a credit instrument, cash advances are not supported, and therefore, no cash advance fees apply.

Late Payment Fees

The card operates on a prepaid basis, meaning users can only spend what’s available in their Busha USDC wallet. As such, there are no late payment fees or interest charges — a key advantage over traditional credit cards.

Over-Limit Fees

Since spending is limited to your available wallet balance, over-limit fees do not apply. Transactions exceeding your balance are automatically declined, keeping spending under control.

Foreign Transaction Fees

The Busha Card supports global online payments with zero foreign transaction fees. Currency conversion from USDC to fiat occurs instantly at the point of sale, ensuring transparent and fair exchange rates.

Hidden or Uncommon Fees

Busha maintains a no-hidden-fee policy. The only potential costs users may encounter are standard platform fees when purchasing USDC within the app and blockchain network fees when transferring crypto from external wallets.

Eligibility and Application Process

The Busha Card is designed for individuals and businesses seeking a simple way to convert crypto into fiat for online spending. The application process is fully digital, fast, and accessible through the Busha mobile app or website.

Below is a detailed overview of who can apply, what’s required, and how to get started.

Who Can Apply

The Busha Card is available to both individual users and registered businesses in Nigeria, Kenya, and Ghana.

Applicants must:

- Be at least 18 years old.

- Have a verified Busha account.

- Maintain a USDC balance or other supported crypto assets to fund the card.

Since the Busha Card operates on a prepaid model, there are no credit checks or minimum income requirements. This makes it accessible to crypto users of all backgrounds, from freelancers and entrepreneurs to everyday consumers, who want a flexible payment solution without banking restrictions.

Required Documents

To meet regulatory and security standards, users must complete Know Your Customer (KYC) verification. The following documents are required:

- Government-Issued ID: A valid national ID, passport, or driver’s license to verify your identity.

- Selfie Verification: A real-time facial capture that confirms the ID belongs to the applicant.

- Proof of Residence: A utility bill, bank statement, or tenancy document showing your current address.

Completing KYC unlocks full access to Busha’s services, including deposits, withdrawals, and card use.

Step-by-Step Application Guide

- Sign Up or Log In: Download the Busha app or visit the website to create or access your account.

- Navigate to “Card” Section: From the dashboard, tap “Request Virtual Card.”

- Submit KYC Documents: Upload your ID, selfie, and proof of residence for verification.

- Review and Confirm: Ensure all details are accurate before submission.

- Wait for Approval: Once verified, your virtual Mastercard will be issued instantly.

Approval Timeline

Most KYC verifications and card issuances are processed within minutes. However, in rare cases where additional checks are required, it may take up to 24 hours for approval.

What Happens After Approval

Once approved, your Busha virtual Mastercard appears in the app. You can immediately:

- Activate the card with one tap.

- Fund it with USDC from your Busha wallet or an external exchange like UEEx, Binance, or Coinbase.

- Start spending instantly, with all payments processed in real time and tracked through your Busha dashboard.

This streamlined process ensures a quick, secure, and hassle-free onboarding experience for every Busha Card user.

Pros and Cons of Busha Card

The Busha Card delivers a convenient, low-cost way for African crypto users to spend USDC (USD Coin) seamlessly online. While it offers many advantages for digital transactions, it also has a few limitations that users should consider before adopting it as their main payment solution.

Pros

Seamless USDC Spending

The Busha Card allows users to spend USDC instantly through a virtual Mastercard, making it easy to shop online, pay for digital subscriptions, or make international payments without manual conversions.

Zero Transaction and Maintenance Fees

There are no transaction, issuance, or monthly maintenance fees, meaning users can make payments freely without worrying about hidden charges — ideal for frequent online spenders or small business owners.

Instant Issuance and Activation

After completing KYC verification, users receive their virtual card instantly via the Busha app. This eliminates waiting times and shipping delays associated with physical cards.

Multi-Card Flexibility

Busha supports up to 10 virtual cards per user, allowing better expense management. For instance, one card can be used for personal subscriptions like Netflix, while another can be dedicated to business-related expenses.

Integration with Payment Platforms

The card works seamlessly with major platforms like PayPal, Wise, and Google Pay, providing users with broader international usability and a more versatile payment experience.

Secure and Fully Digital Experience

The card is fully virtual and integrated into the Busha app, featuring real-time transaction monitoring, spending limits, and instant card freezing, offering enhanced safety for digital transactions.

Cons

No Physical Card or ATM Withdrawals

The Busha Card is virtual-only, meaning users cannot withdraw cash or make in-person payments at POS terminals or ATMs.

Online Use Only

Since it’s designed for digital transactions, it’s limited to online platforms that accept Mastercard, restricting use in physical retail environments.

Requires USDC Funding

Users must hold or purchase USDC (USD Coin) to fund the card. This adds an extra step for those who primarily hold other cryptocurrencies like Bitcoin or Ethereum.

Regional Availability Restrictions

Currently, the card is only available in Nigeria, Kenya, and Ghana, leaving users in other African countries unable to access the service.

User Reviews and Feedback Analysis

Here’s what users are saying about Busha Card:

Aggregate Rating from Multiple Sources

On Trustpilot, Busha has a rating of 3.5 – 3.8 out of 5 based on around 16-17 reviews.

Trustpilot

On the Google Play/app review side (through a review aggregator), the Busha mobile app has a higher average of 4.36, from many users, though more recent ratings show more mixed feedback.

Common Praise Themes

Ease of Use & User Interface

“My experience with Busha has been really smooth so far. Signing up was easy, and I like how simple the app feels compared to other platforms I’ve tried.” (Source: Trustpilot)

Another user on Trustpilot said:

“Great rates, easy to use as a beginner, and super simple. Was able to make transactions seamlessly in seconds”. (Source: Trustpilot)

Many users remark that the design is intuitive, especially for beginners.

Fast Transactions

Users often appreciate fast deposits/funding, trades, or withdrawals (when things work properly). For example, this user said:

“It’s incredible how easy it is to buy an asset of my choice with my local currency and see it immediately”. (Source: Trustpilot)

Good Customer Support (occasionally)

There are instances of praise for responsive support. For example, from an iOS user:

“Great support system … after over 12 hours … I contacted support and in less than 15 mins everything was sorted”. (Source: Apple).

Frequent Complaints

Delays in Deposits / Withdrawals & Missing Funds

A recurring issue: funds taking a long time to arrive or not reflecting. Some users say deposits “aren’t reflecting in accounts” and that withdrawals are delayed.

Someone said:

“Such a terrible crypto exchange…Such a terrible crypto trading platform. I am yet to recover my deposit from them”. (Source: Trustpilot)

Hidden or Unfavorable Rates

Several reviews indicate that selling crypto, especially major amounts, gives a rate much worse than the “market rate,” and that such discrepancies are disclosed only late.

For example:

“I sold 0.01305 BTC (~$1,475) … received ₦1.91M — that’s ₦1,298/$, way below the ₦1,600+ market rate.”. (Source: Trustpilot)

Verification & Account Restrictions

Users often report frustration with KYC / verification delays, being blocked, or being required to upgrade account levels before accessing withdrawal or trading features.

Support Responsiveness / Resolution Issues

Although some users get fast support, others report slow response times or unsatisfactory resolution when issues arise. Complaints include waiting for support for long hours.

Customer Service Feedback

- Positive examples: quick response for verification issues, especially from App Store users; users are impressed when support resolves deposit/withdraw issues.

- Negative feedback: when things go wrong (e.g., missing funds, withdrawn money not arriving), support is sometimes perceived as slow, or users say they were not kept informed or resolved quickly.

Top 7 Alternatives to Busha Virtual Card

Looking for alternatives to the Busha Virtual Card can make sense for many reasons. Maybe you want physical card access, broader merchant acceptance, better rewards, lower fees, or support in other countries.

Since Busha’s card is virtual, USDC-based, and region-limited (Nigeria, Ghana, Kenya), exploring other cards ensures you find something tailored to your payment habits, lifestyle, or business needs.

In this section, you’ll see alternatives spanning premium options. These alternatives include:

UPay Card

Best For: Users Focused on Global Payments

The UPay Card is built for crypto users. It lets you spend your crypto instantly as cash, and you can even get low-interest loans without selling your coins. It’s stronger in international usage and cost transparency.

Key Differentiators

- Offers virtual cards in USD or crypto options (depending on plan).

- Competitive fees for some markets (users claim reasonable rates vs some competitors).

- Appealing to those who want features beyond just USD virtual cards, e.g., some crypto integration.

Pricing

- Transaction fees generally are very low (1% fee + No FX)

- ATM withdrawals may incur 2%.

- No hidden fees claimed; transparency is a core selling point.

Pros

- Offers flexibility in terms of plan choices.

- Potentially lower costs for specific use cases.

- Useful for users looking for alternatives outside the major fintech names.

Cons

- Still expanding merchant partnerships.

- Reports that top-ups or card usage may stop unexpectedly after certain dates.

Why Choose Over Busha Card:

If you want a virtual card with some different merchant rules or features, UPay might look promising. Users who also care about low fees for international use and want a more global-oriented option will find UPAY as the best option.

Binance Card (by Binance)

Best For: Crypto holders wanting wide global acceptance.

The Binance Card lets users spend crypto balances (often converted from stablecoins or other assets) seamlessly in many countries. It supports many currencies, includes rewards in crypto, and is backed by a large, established exchange.

Key Differentiators

- Offers 2% cashback on all your spending in Binance tokens or similar crypto.

- Multiple currency support and a wide merchant network.

- Integration with the Binance ecosystem (wallets, trading, etc.).

Pricing

- Annual fee: None

- Issuing fee: None

- Delivery fee: Free

- Crypto Conversion Fee: 1%

- Foreign Exchange Fee: 1-2%

- ATM Withdrawal Fee: 2 Free Monthly Withdrawals, thereafter 1.5 USD each

Pros

- Good merchant acceptance globally.

- Strong rewards/cashback for active users.

- Easy access if you already use the Binance exchange.

Cons

- Fees hidden in conversion rates can sometimes cut into “free” transaction claims.

- Regulatory or availability issues in some countries (restrictions may apply).

Why Choose Over Busha Card

If you travel often or need a card that works in many more countries and currencies than Busha, Binance may offer greater flexibility and rewards.

Bitnob Virtual Dollar Card

Best For: Frequent online payments & subscriptions globally

The Bitnob Virtual Dollar Card is a prepaid virtual card that enables users to spend in USD (or equivalent currency) using online platforms like Amazon, Netflix, or ASOS. It’s tailored for Africans who need to make regular international payments without relying on local currency restrictions.

Pricing

- Virtual card issuance: $1 for every newly issued card

- Top Up: $1 if the top-up is below $100, and 1% if the top-up is $100 or more

- Termination: $1 fee is charged for card termination; the remaining balance is returned to the user

- Card Declined: $1 for automatic termination after three failed transactions due to insufficient funds

- Cross Border Fees: A 2.5% + $0.5 fee applies for payments made to shops outside the US.

Pros

- Option to create different cards for different services

- Good online subscription support & USD-denominated payments help avoid local currency volatility

- Strong security controls (freeze, custom limits, etc.)

Cons

- Only virtual; no physical card or ATM withdrawals

- Dependent on the USD wallet and any funding delays or fees when converting to USD or bringing in crypto

Why Choose Over Busha Card

If you often pay for international USD-based digital services and want a virtual card already denominated in dollars, Bitnob may give you better exchange value and fewer conversion steps than Busha, which works with USDC-to-fiat conversions at each transaction.

Chipper Cash USD Virtual Card

Best For: Affordable international payments and streaming.

Chipper Cash provides a low-entry cost card for users to pay internationally (Amazon, Netflix, app subscriptions, etc.). It’s good if you don’t need huge limits but want decent reliability, low cost, and ease of setup.

Key Differentiators

- Budget effectively, only using the amount uploaded to your card

- Often good for streaming, subscription services, and small cross-border ecommerce.

- Widely accepted by global platforms.

Pricing

- Annual fee: minimal or none, depending on plan.

- Issuance fee: $3

- Decline Fee: ₦250

- Simplified Fee: A $0.90 flat fee will be charged on all successful USD card transactions.

- Monthly maintenance: around US$1 for some users.

Pros

- Very affordable entry and keeping costs low for regular users.

- Good UX, quick card issuance in many cases.

- Supporting frequent use for small transactions (streaming, apps).

Cons

- Low or moderate limits will restrict large spending.

- Sometimes recurring fees might apply depending on the plan.

Why Choose Over Busha Card:

If your spending is mostly small recurring digital purchases (subscriptions, streaming), Chipper is likely cheaper and simpler than Busha, particularly if you don’t use USDC.

AccessMore Virtual Cards

Best For: Users needing multi-currency virtual cards from a traditional bank

Access Bank’s AccessMore Virtual Card allows users to generate virtual cards in multiple currencies (Naira, USD, Euro, GBP) and use them for online purchases. It combines bank trust with virtual card flexibility.

Key Differentiators

- Multiple currency variants for virtual cards (e.g., USD, GBP, Euro, Naira) so you can match card currency with merchant or payment region.

- Inbuilt into a major bank’s app (Access Bank / AccessMore), meaning easier support and perhaps more stable regulatory compliance.

Pricing

- Issuance cost dependent on currency: e.g., Naira virtual card ~ N1,075 (including VAT) for Access Bank AccessMore.

- Quarterly maintenance for cards: small fees for Naira, USD, GBP, Euro variants.

Pros

- Multi-currency reduces foreign transaction conversion fees by allowing you to match the payment’s currency to the region where the transaction originates.

- Virtual in nature means no shipping or physical card delays

- Good oversight via bank-regulated infrastructure

Cons

- The issuance fee or maintenance fees may apply, depending on the currency

- Some features, like a virtual card in foreign currency, may have usage or funding restrictions

Why Choose Over Busha Card:

If you frequently pay in different currencies (not only USD/USDC) or want bank-based backing, AccessMore’s multi-currency virtual cards may be more convenient than Busha’s USDC-centric model.

Vesti Virtual Dollar Card (by Vesti)

Best For: High-volume international spenders needing large limits.

Vesti’s card is ideal if you often make large purchases or manage cross-border subscriptions. It has higher monthly spending limits compared to many virtual USD cards, and the creation fee is modest. Many users appreciate its speed and reliability.

Key Differentiators

- High monthly spending limits (e.g., up to US$10,000/month) for many users.

- No ongoing maintenance fees in many cases.

- Good security and controls via the app (e.g., ability to delete/invalidate cards).

Pricing

- Creation/issuance fee: $10 (varies)

- Maintenance fee: often none.

- Exchange/funding fees: depend on how you top up (bank transfer, wallet) and the rates applied.

Pros

- Great for large purchases (ads, tuition, business expenses).

- Few recurring fees.

- Well-suited for people who need reliability and good service.

Cons

- The initial fee is higher than the very cheapest virtual cards.

- Depending on the region, funding and exchange rates may add cost.

Why Choose Over Busha Card:

If you need higher transaction limits and want to pay for expensive international subscriptions or business tools, Vesti gives you capacity that Busha likely cannot match.

GeePay (Raenest)

Best For: Freelancers needing multi-currency virtual cards.

GeePay issues virtual cards in USD (and some other currencies) aimed at gig workers and small businesses. It supports receiving payments from abroad, issuing invoices, etc., which makes it more business-oriented or freelancing-oriented.

Key Differentiators

- Multi-currency wallet and virtual cards in USD, GBP, and EUR in some instances.

- Low creation fee (~US$2-3) and no or low maintenance based on plan.

- Designed with business tools: invoice management, payout options.

Pricing

- Creation fee: $3 (one-time fee)

- Virtual dollar card funding: $0.5 per funding transaction

- Transaction charges: $0.5 per transaction

- Cross-border fee (payments on a non-US website): 0.9% (charged by Mastercard)

- Card maintenance: Free

- Withdrawal from card to wallet: Free

- Monthly service: Free

Pros

- Great flexibility in currency options, beneficial for those paid in USD/GBP/EUR.

- Low overhead for business/freelancers.

- Useful support for international payments and payout options.

Cons

- Exchange rate spreads / conversion margins can be unfavourable at times.

- Some features are restricted unless higher tiers of verification are completed.

Why Choose Over Busha Card:

If your income is from abroad, or you need virtual cards in different currencies and tools for business invoicing, GeePay may serve you better than Busha, which is more focused on USDC spending in specific locales.

Comprehensive Comparison Table

| Card Name | Annual Fee | Rewards Rate | Welcome Bonus | Credit Check Required | Best For (Use Case) | Key Feature | Major Limitation | Overall Rating (out of 5) |

| Busha Virtual Card | $0 | None | None | No | Seamless USDC spending across Africa | Virtual Mastercard for USDC payments (Nigeria, Ghana, Kenya) | No physical card or ATM withdrawals | 4.0 |

| Binance Card (by Binance) | $0 | Up to 2% cashback in crypto | None | Yes (KYC via Binance) | Crypto holders wanting wide global acceptance | Spend crypto worldwide with instant conversion | Not available in all countries; conversion fees may apply | 4.5 |

| Bitnob Virtual Dollar Card | $0 (issuance $1/card) | None | None | No | Frequent online USD payments & subscriptions | USD-denominated prepaid card for global use | No physical card; dependent on USD funding | 4.1 |

| Chipper Cash USD Virtual Card | $1 monthly | None | None | No | Affordable international payments & streaming | Budget-friendly USD card for small online purchases | Low spending limits | 3.8 |

| UPay.best Card | $0 | None | None | No | Users focused on global payments | Supports crypto-to-cash payments and low FX fees | Merchant acceptance still expanding | 4.2 |

| AccessMore Virtual Card (Access Bank) | ₦1,075 (~$0.70) issuance | None | None | Yes (bank KYC) | Multi-currency online transactions | Generate Naira, USD, GBP, or Euro virtual cards | Limited foreign currency top-up channels | 4.0 |

| Vesti Virtual Dollar Card | $10 issuance | None | None | No | High-volume international spenders needing large limits | High transaction limits (up to $10,000/month) | High initial setup fee | 4.4 |

| GeePay (Raenest) | $3 issuance | None | None | No | Freelancers & small businesses handling foreign payments | Multi-currency (USD/GBP/EUR) with invoicing and payouts | Exchange rate spreads can reduce value | 4.3 |

How to Choose: Decision Framework

Selecting the right virtual or crypto card goes beyond fees—it’s about matching your business goals, spending habits, and financial structure with the right tool.

Below is a practical decision framework that helps you identify which card fits your unique needs.

Business Size Considerations

For individual freelancers or small startups, simplicity and cost-efficiency are key. Cards like Busha Virtual Card, Chipper Cash, or Bitnob are ideal, offering low entry barriers, minimal fees, and straightforward funding.

For example, a small e-commerce seller in Lagos who needs to pay Shopify or Canva subscriptions can use Busha’s virtual Mastercard without worrying about monthly fees or minimum balances.

However, growing SMEs or established companies often require higher transaction limits and structured financial controls. Vesti Virtual Dollar Card offers up to $10,000 in monthly limits—ideal for businesses managing larger advertising budgets or cross-border supplier payments.

Similarly, GeePay (Raenest) suits small agencies or freelancers working with international clients since it supports multi-currency payments and invoicing, making it easier to manage funds in USD, GBP, or EUR.

Industry-Specific Needs

Different industries demand different financial functionalities. Tech startups and crypto-driven businesses may lean toward Busha, Binance, or UPay.best due to their crypto integration. For example, a blockchain consultancy firm that earns in USDC could seamlessly use Busha to cover SaaS costs in USD without conversion losses.

Meanwhile, creative professionals or media businesses—often managing subscriptions to platforms like Adobe, Netflix, or Spotify—might find Chipper Cash or Bitnob more convenient due to their simplicity and affordability for digital service payments.

Cash Flow Situations

If your business operates with tight cash flow or irregular income, flexibility and transparency are vital. UPay.best and GeePay offer strong advantages here. UPay charges low, predictable fees and supports crypto as collateral, allowing users to access funds without liquidating holdings.

GeePay, on the other hand, enables easy withdrawal of funds and free maintenance, helping freelancers or micro-entrepreneurs avoid unexpected deductions.

International vs. Domestic Use

Your geographic spending pattern matters greatly. If most of your payments are domestic within Africa, Busha, AccessMore, and Chipper Cash are excellent options. They support African markets (Nigeria, Ghana, Kenya) and provide better local customer support and funding options.

However, for global spending or frequent international travel, Binance Card, Vesti, and UPay.best take the lead. The Binance Card offers worldwide acceptance and crypto cashback, while UPay supports global merchants with minimal FX costs. Vesti’s high limit also makes it suitable for large-scale payments to international vendors or institutions.

Technology Requirements

Your business’s tech maturity should guide your card choice. Fintech-savvy users who already use wallets, DeFi platforms, or crypto exchanges will find Busha, UPay.best, or Binance Card highly compatible with their workflows. These platforms offer instant issuance, API integration for developers, and real-time balance management through mobile dashboards.

Businesses that prefer traditional banking stability and straightforward digital interfaces will appreciate AccessMore, which integrates virtual card creation directly within a bank’s secure mobile app. Similarly, Chipper Cash offers one of the smoothest app experiences for beginners unfamiliar with crypto tools.

Security and Compliance Needs

Compliance, regulation, and fraud prevention should never be overlooked. AccessMore (by Access Bank) is a strong choice for organizations that prioritize regulatory oversight and bank-grade security. Its cards are directly issued under Nigeria’s banking framework, making them reliable for corporate governance and accounting transparency.

Binance Card and Busha ensure crypto users benefit from KYC/AML-compliant frameworks—important for businesses in fintech or international commerce.

Growth and Scalability

As your business expands, scalability becomes critical. Vesti and GeePay are standout choices for this, providing higher limits, business invoicing tools, and cross-border payment features that evolve with user needs.

Busha, Bitnob, and Chipper Cash are better suited to smaller-scale or early-stage operations, as they prioritize affordability and speed over large transaction capabilities. Still, for businesses planning to scale into the crypto economy, UPay.best offers a future-ready solution that supports hybrid fiat-crypto spending models without changing platforms.

Final Thoughts

Despite the negative reviews regarding limited offline use and regional restrictions, the Busha Card remains a practical option for crypto users seeking to spend USDC online without hassle. It provides seamless integration between digital wallets and real-world payments, allowing users in Nigeria, Ghana, and Kenya to fund and use their virtual Mastercard instantly.

With no issuance or transaction fees, it’s an affordable tool for individuals and small businesses looking to make online purchases, manage subscriptions, or pay for global services directly from crypto holdings.

The Busha Card is best suited for users who already hold USDC and want a fast, fee-free way to spend online. Freelancers, digital entrepreneurs, or crypto-savvy consumers who primarily shop or pay for tools like Canva, Spotify, or Amazon will find its convenience and speed worthwhile.

Its focus on digital-only transactions makes it a perfect fit for those who rarely use ATMs or need physical cards, while its zero-maintenance structure ensures simple, transparent use.

However, users seeking in-person payments, ATM withdrawals, or broader country availability may find Busha’s limitations restrictive.

Businesses handling multi-currency transactions or requiring higher spending limits will benefit more from cards like Vesti or AccessMore, while users focused on international travel or global merchant acceptance will appreciate the Binance Card, which supports multiple cryptocurrencies and provides cashback on purchases.

Among the alternatives, the Binance Card stands out as the top recommendation due to its global reach, multi-currency flexibility, and integrated crypto ecosystem. It bridges the gap between crypto and fiat payments more comprehensively than Busha, making it ideal for anyone transacting beyond Africa or seeking added rewards.

Overall, the Busha Card occupies a solid middle ground in the crypto-payment market—reliable, affordable, and regionally efficient for online spending, yet not as versatile as global options.

For users in supported African regions seeking to convert and spend crypto effortlessly, it remains one of the most accessible and practical solutions. But for those demanding global usability, higher transaction power, or advanced reward systems, exploring the listed alternatives would deliver better long-term value and flexibility.

Frequently Asked Questions

Is Busha Wallet Legit?

Yes, the Busha Wallet is legitimate, operating under Nigeria’s securities regulations with a provisional license from the SEC, and is widely used without any recorded instances of fraud. It has strong security measures, KYC protocols, and positive user feedback on app stores.

How Long Does It Take To Verify Busha?

Verification for the Busha Card typically completes within 24–48 hours after submitting your required KYC documents (ID, selfie, proof of address). Once your documents are approved, your virtual card is issued almost instantly, and you can start using it right away.

How Long Does It Take To Receive BTC on Busha?

Receiving BTC on Busha is usually instant when it’s sent from another Busha user, thanks to in‑app transfers via username, email, or QR code.

How Does the Busha App Work?

The Busha app allows users to buy, sell, store, and spend cryptocurrencies—especially USDC—while also managing their Busha Card, tracking transactions, and performing secure wallet transfers, all from a single mobile platform.