A Central Bank Digital Currency (CBDC) is the digital form of a country’s fiat currency issued and backed directly by its central bank. Unlike cryptocurrency, CBDCs are fully centralised, government-controlled, and designed to function as digital legal tender. As of 2025, 137 countries representing 98% of global GDP are exploring a CBDC, with 49 active pilot projects and 3 countries having fully launched one.

Key Takeaways

- 137 countries and currency unions representing 98% of global GDP are exploring CBDCs in 2025, up from just 35 in May 2020. There are 49 active pilot projects and 72 countries in the advanced phase.

- Three countries have fully launched CBDCs: the Bahamas (Sand Dollar), Jamaica (JAM-DEX), and Nigeria (eNaira). China’s e-CNY pilot is the largest, with approximately $986 billion in transaction volume.

- India’s e-rupee is the second-largest pilot, with circulation rising 334% to the equivalent of $122 million by March 2025. The US is the only major economy to formally block retail CBDC development.

- In January 2025, President Trump signed an executive order halting all US retail CBDC work. The House passed the Anti-CBDC Surveillance State Act in July 2025.

- The primary debate around CBDCs centres on privacy: 41% of all public responses to the European Central Bank’s consultation focused on privacy concerns.

- Cross-border wholesale CBDC projects have more than doubled since 2022, with 13 active initiatives including Project mBridge connecting China, Thailand, the UAE, Hong Kong, and Saudi Arabia.

What Is a Central Bank Digital Currency (CBDC)?

Source: Shutterstock

A Central Bank Digital Currency is the digital form of a country’s fiat currency that is also a direct claim on the central bank. Instead of printing paper notes, the central bank issues electronic tokens or accounts backed by the full faith and credit of the government. A CBDC is not a cryptocurrency, it is not decentralised, and it is not anonymous. It is essentially digital cash: the same value, the same legal tender status, but existing only in electronic form.

To understand why this matters, consider how money works today. Physical cash (banknotes and coins) is central bank money: it is a direct liability of the central bank with no default risk. But the vast majority of money most people interact with is commercial bank money, the digits in your bank account that represent a promise by your bank, not the central bank. If your bank fails, that money is at risk. A CBDC would give the public access to digital central bank money for the first time, combining the safety of physical cash with the convenience of digital payment.

The concept of a CBDC emerged as cash use declined globally, private digital payment platforms grew in dominance, and cryptocurrencies demonstrated both the demand for digital money and the risks of unregulated digital currencies. Central banks recognised they needed to provide a public digital option or cede the future of money to private actors.

What Are the Different Types of CBDCs?

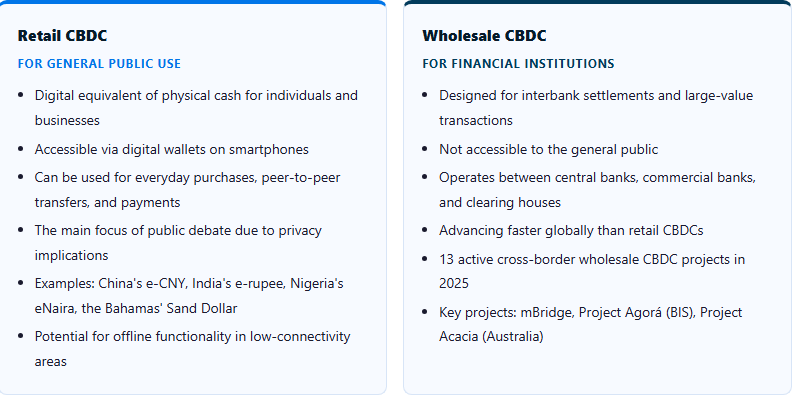

There is no single CBDC design that fits all economies. Countries are pursuing different models based on their monetary systems, financial infrastructure, and policy goals. The most fundamental distinction is between retail and wholesale:

Examples of Wholesale CBDCs are The Bank of Canada’s Project Jasper, The Bank of England’s RTGS Renewal Programme, The Monetary Authority of Singapore’s Project Ubi.

Examples of Retail CBDCs are The Digital Yuan (e-CNY) issued by the People’s Bank of China,The Sand Dollar issued by the Central Bank of The Bahamas,The e-Krona project by Sveriges Riksbank, the central bank of Sweden.

What Are the Different CBDC Distribution Models?

Countries are also choosing between different distribution approaches. In a direct model, citizens hold CBDC accounts directly with the central bank. In an indirect (two-tier) model, commercial banks and payment providers distribute and manage CBDC accounts for their customers while the central bank maintains the backend infrastructure. Most countries, including China, are pursuing the two-tier model to preserve the role of commercial banks in the financial system. A hybrid model allows direct central bank claims but has private sector companies manage user-facing services.

How Do CBDCs Differ from Cryptocurrency and Stablecoins?

CBDCs are frequently confused with or compared to cryptocurrency and stablecoins. The differences are fundamental:

| Feature | CBDC | Cryptocurrency (e.g. Bitcoin) | Stablecoin (e.g. USDC) |

|---|---|---|---|

| Issuer | Government central bank | Decentralised protocol (no issuer) | Private company (Circle, Tether) |

| Control | Fully centralised; government oversight | Decentralised; no single controller | Centralised issuer; blockchain rails |

| Price stability | Fully stable (equals national currency) | Highly volatile | Pegged; minor de-peg risk |

| Privacy | Low; all transactions traceable by central bank | Pseudonymous to fully anonymous (varies) | On-chain transparency; issuer can freeze |

| Legal status | Legal tender in issuing country | Not legal tender in most countries | Not legal tender; regulated asset |

| Programmability | Yes; central bank can embed conditions | Limited at base layer (smart contracts via L2) | Yes; smart contract programmable |

| Supply limit | No cap; central bank controls issuance | Hard cap (e.g. 21M Bitcoin) | Determined by reserve backing |

Stablecoins occupy a middle ground. Like CBDCs, they aim for price stability by pegging to fiat currencies. But they are issued by private companies rather than governments and operate on public blockchains rather than centralised infrastructure. The stablecoin market reached $305 billion in 2025 and settled $52.9 trillion in transaction value. This scale is precisely why central banks accelerated CBDC development: privately issued digital dollars like USDC are effectively performing functions that central banks feel should remain in the public sector.

Read Also: Understanding Decentralised Finance (DeFi)

How Does a CBDC Actually Work?

Source: Shutterstock

A CBDC transaction works differently depending on the distribution model chosen, but the fundamental flow is straightforward. A user holds CBDC in a digital wallet, either an app provided by a commercial bank or directly through a government platform. When they make a payment, the CBDC transfers from their wallet to the recipient’s wallet. The central bank maintains the authoritative ledger of all CBDC balances and transactions, providing a complete and auditable record of every payment made in the system.

What Technology Do CBDCs Use?

CBDCs do not necessarily require blockchain technology. Many designs use more conventional centralised databases that can process transactions faster and at lower cost than public blockchains. Some designs incorporate distributed ledger technology to improve resilience and allow multiple authorised participants (such as regulated banks) to operate nodes. China’s e-CNY, for example, uses a tiered architecture with a centralised core ledger managed by the People’s Bank of China, with commercial banks managing customer-facing wallets.

Can CBDCs Work Offline?

Offline functionality is a major design priority for retail CBDCs, particularly in developing economies where internet access is unreliable. India’s e-rupee pilot is specifically testing offline payment capabilities, allowing users to pay with CBDC even without internet connectivity. The BIS Project Polaris has examined security and resilience in offline CBDC systems. Offline functionality is seen as essential for financial inclusion: if a digital currency requires internet access, it fails to serve the unbanked populations it is meant to reach.

Read Also: Crypto Is Not Regulated: Addressing the Misconception

What Are the Potential Benefits of CBDCs?

Improved Financial Inclusion

Approximately 1.4 billion adults globally remain unbanked. CBDCs could give these individuals access to safe, government-backed digital money using just a basic smartphone, without requiring a commercial bank account, a credit history, or physical access to a bank branch. This is a primary driver of CBDC development in emerging markets: the Bahamas, Jamaica, and Nigeria all specifically identified financial inclusion as a core goal. Juniper Research forecasts that by 2031, CBDCs will facilitate 7.8 billion payments globally, up from 307 million in 2024, with much of that growth in developing economies.

Faster and Cheaper Payments

Traditional international wire transfers can take 2 to 5 business days and cost 5 to 7% in fees. Cross-border wholesale CBDC projects like mBridge could reduce these costs by an estimated $45 billion annually by 2031. Retail CBDCs enable near-instant settlement of domestic payments, reducing or eliminating the current 1 to 3-day settlement cycle for many transaction types. This is particularly valuable for businesses managing cash flow and for individuals sending remittances.

Greater Monetary Policy Precision

CBDCs give central banks new tools for monetary policy implementation. Programmable money could theoretically allow direct stimulus transfers to citizens, negative interest rates enforced on large CBDC balances, or targeted support for specific economic sectors. The ECB has noted that CBDCs could allow more direct transmission of monetary policy than the current system, where central bank decisions must flow through commercial banks before reaching the real economy.

Reduced Financial Crime

Because every CBDC transaction is traceable on the central bank’s ledger, CBDCs could significantly reduce money laundering, tax evasion, and illicit financing. This is a benefit frequently cited by governments, though it is precisely this traceability that generates the strongest privacy objections from civil liberties advocates and citizens.

Payment System Resilience

Having an alternative, government-run digital payment system reduces dependency on private payment infrastructure. If a major commercial bank or payment network fails, a CBDC network could continue to function, ensuring that basic commerce can continue during financial system disruptions.

What Are the Risks and Concerns Around CBDCs?

The development of CBDCs is not without significant controversy. Several categories of risk have generated substantial public debate and, in the US case, formal legislative opposition:

Financial Privacy and Surveillance

This is the most debated risk. Because CBDCs create a complete digital record of every transaction accessible to the central bank and potentially to government agencies, they raise serious concerns about financial surveillance. During the ECB’s public consultation process, 8,200 comments centred on privacy, representing 41% of all public responses. Critics point out that physical cash allows people to transact with complete anonymity; a CBDC-only world would eliminate that privacy entirely.

The concern is not merely theoretical. Governments could potentially use CBDC transaction data to identify political dissidents, monitor suspected criminals without judicial warrants, or enforce ideologically motivated financial restrictions. The US House’s Anti-CBDC Surveillance State Act, passed in July 2025, explicitly cited “programmable money” and the example of China’s digital yuan as demonstrations of how CBDCs could be used as instruments of state control.

Bank Disintermediation

If citizens can hold deposits directly with the central bank through CBDCs, they may choose to withdraw money from commercial banks, particularly during periods of financial stress when people might prefer the safety of central bank money. This “digital bank run” risk could reduce the deposits available for commercial banks to lend, tightening credit conditions throughout the economy. Most CBDC designs include limits on individual CBDC holdings to mitigate this risk.

Programmability Misuse

CBDCs can be programmed with conditions that physical cash cannot carry. This capability could be used for legitimate purposes (such as ensuring emergency aid payments are spent on food rather than alcohol), but it could also be misused to restrict what citizens can buy, add expiry dates to funds to force spending, or penalise socially disfavoured behaviours. The potential for programmable restrictions is among the most cited concerns from civil liberties organisations.

Cybersecurity and System Vulnerabilities

A centralised CBDC system represents a single, high-value target for cyberattacks. If the central bank’s CBDC infrastructure were compromised, the consequences could be catastrophic for the entire domestic financial system. This is why resilience and cybersecurity are top priorities in the design of all major CBDC pilots, but centralised systems are inherently more vulnerable than the distributed architecture of public blockchains.

“Monetary innovation should remain in the hands of the people, not the administrative state.”Congressman Tom Emmer, sponsor of the Anti-CBDC Surveillance State Act, July 2025

Where Are CBDCs in 2025: Global Status by Country?

| Country / Region | Status (2025) | CBDC Name | Key 2025 Development |

|---|---|---|---|

| China | Pilot (largest globally) | e-CNY (Digital Yuan) | ~$986B in transaction volume across 17 provinces; expanding cross-border use via mBridge project |

| India | Pilot (2nd largest) | e-Rupee (Digital Rupee) | Circulation rose 334% to $122M by March 2025; testing offline payments and cross-border pilots |

| European Union | Preparation phase | Digital Euro | ECB moved from investigation to preparation phase; emphasising privacy-by-design; no launch date confirmed |

| United States | Halted (retail) | Digital Dollar (blocked) | Trump executive order (Jan 2025) halted retail CBDC; Anti-CBDC Surveillance Act passed House (Jul 2025); wholesale research continues via Project Agorá |

| Nigeria | Launched | eNaira | One of three fully launched CBDCs; focused on expanding domestic adoption and financial inclusion |

| Bahamas | Launched | Sand Dollar | First CBDC ever launched (2020); expanding domestic reach and cross-island payment accessibility |

| United Kingdom | Design phase | Digital Pound (Britcoin) | Detailed blueprint expected 2026; Bank of England collaborating with MAS Singapore on standards |

| mBridge (Multi-country) | Active cross-border pilot | mBridge (wholesale) | Connects China, Thailand, UAE, Hong Kong, and Saudi Arabia for cross-border wholesale settlements |

Notable 2025 development: The US position is unique among major economies. While all G20 nations are engaged in CBDC research, the US is the only one to have formally prohibited retail CBDC development at the executive level. Supporters of private stablecoins argue this positions the US dollar-pegged stablecoin ecosystem (USDT, USDC) as the de facto global digital dollar, without the government surveillance concerns of a state-issued CBDC.

How Do CBDCs Affect Cryptocurrency?

The relationship between CBDCs and cryptocurrency is complex and frequently misunderstood. They are not substitutes for each other: they serve different purposes and are designed for different user needs.

Will CBDCs Replace Bitcoin or Ethereum?

No. CBDCs are digital versions of existing fiat currencies, not new forms of money. A digital euro is still a euro: it depreciates with inflation, it is controlled by the ECB, and it has no hard supply cap. Bitcoin’s primary value proposition is precisely the opposite: it is decentralised, censorship-resistant, inflation-resistant (capped at 21 million), and not controlled by any government. Users who hold Bitcoin specifically to escape centralised monetary control will not switch to a CBDC, which is the epitome of centralised monetary control.

Will CBDCs Reduce Demand for Stablecoins?

Retail CBDCs and stablecoins do occupy more overlapping territory. Both aim to provide a stable digital currency for payments and DeFi. The stablecoin market reached $305 billion in market cap in 2025 and settled $52.9 trillion in transaction value, much of it serving functions a retail CBDC would also cover. Some displacement of private stablecoins in domestic retail payments is likely if CBDCs are widely adopted, but stablecoins will retain advantages in cross-border DeFi, programmable finance, and markets where access to regulated CBDCs is not available.

Could CBDCs and Crypto Coexist?

Yes, and they likely will. The ECB has explicitly stated it does not intend the digital euro to replace cash, stablecoins, or cryptocurrencies, but to provide a public option alongside them. In practice, different instruments will serve different needs: CBDCs for domestic payments and government services, stablecoins for DeFi and cross-border DeFi transactions, and cryptocurrencies like Bitcoin for censorship-resistant value storage and international settlement. The regulatory clarity that CBDCs bring to the digital currency space may ultimately benefit the broader crypto ecosystem by legitimising digital money as a concept.

What Is the Future of CBDCs?

The World Economic Forum projects 24 CBDCs will be operational by 2030. The momentum is accelerating but unevenly distributed. Several trends will define the trajectory:

Cross-Border Integration Will Accelerate

Wholesale CBDC projects have more than doubled since 2022, driven partly by the geopolitical pressure from sanctions. Project mBridge connects China, Thailand, UAE, Hong Kong, and Saudi Arabia for wholesale settlements. Project Agorá connects seven major central banks. Cross-border CBDC infrastructure could potentially save $45 billion annually in international payment costs by 2031, providing strong economic incentive for continued development regardless of retail CBDC debates.

Privacy-by-Design Will Be a Competitive Differentiator

The privacy debate will shape which CBDC models succeed in democratic societies. The ECB is specifically building privacy-by-design into the digital euro architecture, recognising that without public trust on privacy, adoption will fail. CBDCs that can offer transaction privacy comparable to cash for small everyday purchases, while maintaining anti-money-laundering compliance for large transactions, are most likely to achieve broad acceptance. The US House’s Anti-CBDC Surveillance State Act demonstrates the political cost of ignoring this concern.

Programmability Will Be Both the Promise and the Peril

The most powerful and most controversial feature of CBDCs is programmability. The ability to embed conditions into money itself could enable entirely new forms of economic policy, targeted welfare distribution, and automated compliance. But the same capability also enables the restrictions on personal financial freedom that critics fear. How governments choose to use, or refrain from using, programmability will determine whether CBDCs are seen as useful infrastructure or as a surveillance threat.

Read Also: What Is Blockchain Technology?

Conclusion

Central Bank Digital Currencies (CBDCs) mark a significant evolution in finance. They promise to enhance efficiency, foster financial inclusion, and reshape the global financial landscape. However, their implementation is not without challenges, requiring careful management.

As we progress in the digital age, the role of CBDCs in our economy is an exciting development to observe. Their successful implementation hinges on robust technology, sound regulation, and international cooperation. The future of CBDCs is indeed a fascinating aspect of the digital economy.

Frequently Asked Questions

What is a Central Bank Digital Currency (CBDC)?

A Central Bank Digital Currency is the digital form of a country’s fiat currency issued and backed directly by the central bank. Unlike a bank deposit, a CBDC is a direct liability of the central bank itself, carrying no credit or liquidity risk to the holder. Unlike cryptocurrency, CBDCs are fully centralised, government-controlled, and not anonymous. They function as digital legal tender with the same value as physical cash.

How many countries are developing CBDCs in 2025?

As of 2025, 137 countries and currency unions representing 98% of global GDP are exploring a CBDC, up from just 35 in May 2020. Of these, 72 are in the advanced phase including development, pilot, or full launch. There are 49 active pilot projects. Three countries have fully launched a CBDC: the Bahamas (Sand Dollar), Jamaica (JAM-DEX), and Nigeria (eNaira). China’s e-CNY pilot is the largest globally, with approximately $986 billion in transaction volume.

What is the difference between a CBDC and cryptocurrency?

CBDCs and cryptocurrencies are fundamentally different. CBDCs are centralised, issued and controlled by a government’s central bank, and represent digital legal tender with no price volatility relative to the national currency. Cryptocurrency is typically decentralised, not issued or controlled by any government, and subject to significant price volatility. CBDCs are programmable and traceable by the issuing authority; most cryptocurrencies offer varying degrees of anonymity. CBDCs are designed to complement or replace physical cash; crypto operates independently of the traditional financial system.

What are the main risks of CBDCs?

The main risks of CBDCs include: financial privacy, since CBDCs create a complete digital record of every transaction accessible to the central bank; bank disintermediation, as citizens holding CBDCs directly with the central bank may reduce commercial bank deposits; programmability misuse, where governments could restrict what citizens can spend money on or add expiry dates to funds; cybersecurity vulnerabilities in centralised CBDC infrastructure; and bank run risk if citizens can rapidly convert commercial bank deposits to CBDCs during a financial crisis.

What happened with the US CBDC in 2025?

The United States became the only major economy to formally block retail CBDC development in 2025. In January 2025, President Trump signed an executive order halting all work on a US retail CBDC. In July 2025, the House of Representatives passed the Anti-CBDC Surveillance State Act, which prohibits the Federal Reserve from issuing, piloting, or implementing any CBDC for public use. However, the US continues to participate in wholesale cross-border payments research through Project Agorá, a collaborative initiative with six other major central banks.

What is the difference between retail and wholesale CBDCs?

Retail CBDCs are designed for general public use, functioning as a digital equivalent of physical cash for everyday transactions. Wholesale CBDCs are designed exclusively for use between financial institutions and central banks for interbank settlements and large-value transactions. Most public debate focuses on retail CBDCs because of their privacy implications. However, wholesale CBDCs are advancing faster globally: there are 13 active cross-border wholesale CBDC projects in 2025, more than double the number before 2022, driven largely by geopolitical pressure around sanctions and payment sovereignty.