Uncertain about crypto’s wild swings? Master historical volatility analysis to navigate these markets, identify risks, and make informed investment decisions.

The price of cryptocurrencies is notoriously volatile, with sharp and sudden swings in value. For traders and investors, this volatility may be both a boon and a bane presenting both substantial risks and potential for profit.

Historical volatility research is a valuable tool for managing risk, identifying market trends, and making well-informed investment decisions. It is one of the best strategies for maneuvering these markets.

This piece will examine historical volatility analysis in the context of cryptocurrency, including its definition, significance, uses, and constraints. After reading through, you will have a firm grasp on how to use historical volatility analysis to enhance your cryptocurrency trading and investing tactics.

“80% of cryptocurrency traders use technical analysis, including historical volatility analysis, to inform their investment decisions”

Key Takeaways

- Historical volatility (HV) measures past price fluctuations of a cryptocurrency. It helps assess risk and make informed investment decisions.

- Common methods to calculate HV include moving averages (MA), Bollinger Bands (BB), standard deviation (SD), Average True Range (ATR), and Historical Volatility Index (VIX for S&P 500 only).

- HV analysis helps with risk management like identifying potential risks, setting stop-loss orders, and understanding overbought/oversold conditions.

- HV is crucial for option trading as options are more valuable with higher volatility.

- Limitations of HV analysis include data quality, model assumptions, market regime changes, and overfitting.

What is Historical Volatility?

Historical volatility, also known as realized volatility, is a measure of the past price fluctuations of a cryptocurrency over a specific period of time. It is a statistical measure that quantifies the amount of uncertainty or risk associated with an asset’s price movements.

“The average daily volatility of Bitcoin is around 4.5%, making it a highly volatile asset”

Recommended reading: How to Understand Crypto Volatility Through Technical Analysis

How is Historical Volatility Calculated?

Historical volatility is typically calculated using the standard deviation of an asset’s price returns over a given time frame. The most common methods for calculating historical volatility include:

- Simple Moving Average (SMA): This method involves calculating the average price return over a specified time frame, usually using a simple moving average formula.

- Exponential Moving Average (EMA): This method calculates the average price return over a specified time frame, using an exponential moving average formula that gives more weight to recent price movements.

- Standard Deviation (SD): This method involves calculating the standard deviation of an asset’s price returns over a specified time frame, usually using a formula that takes into account the mean and variance of the returns.

What is the Formula for Calculating Historical Volatility?

The formula for calculating historical volatility using the standard deviation method is:

HV = √(Σ[(xi – μ)^2 / (n – 1)])

Where:

HV = Historical Volatility

xi = individual price returns

μ = mean of the price returns

n = number of observations (i.e., the number of data points)

Σ = summation symbol, indicating the sum of the squared differences between each price return and the mean

What is the Unit of Measurement for Historical Volatility?

Historical volatility is usually expressed as a percentage and represents the annualized standard deviation of an asset’s price returns. For example, if the historical volatility of Bitcoin is 80%, it means that the price of Bitcoin has fluctuated by an average of 80% over the past year.

How is Historical Volatility Interpreted?

Historical volatility is interpreted as a measure of the uncertainty or risk associated with an asset’s price movements. A higher historical volatility indicates that the asset’s price has been more volatile in the past, while a lower historical volatility indicates that the asset’s price has been more stable.

For example, if the historical volatility of Bitcoin is 75%, it suggests that the price of Bitcoin has been highly volatile in the past, with large price swings occurring frequently. On the other hand, if the historical volatility of a stablecoin is 5%, it suggests that the price of the stablecoin has been relatively stable, with smaller price movements occurring infrequently.

“Historical volatility analysis can improve trading performance by up to 20%”

Recommended reading: Crypto Volatility Analysis: A Complete Guide

Methods of Historical Volatility Analysis

Historical volatility analysis uses various methods to calculate and analyze the historical volatility of an asset. There are several methods that can be used, each with its own strengths and weaknesses. Here are some of the most common methods of historical volatility analysis:

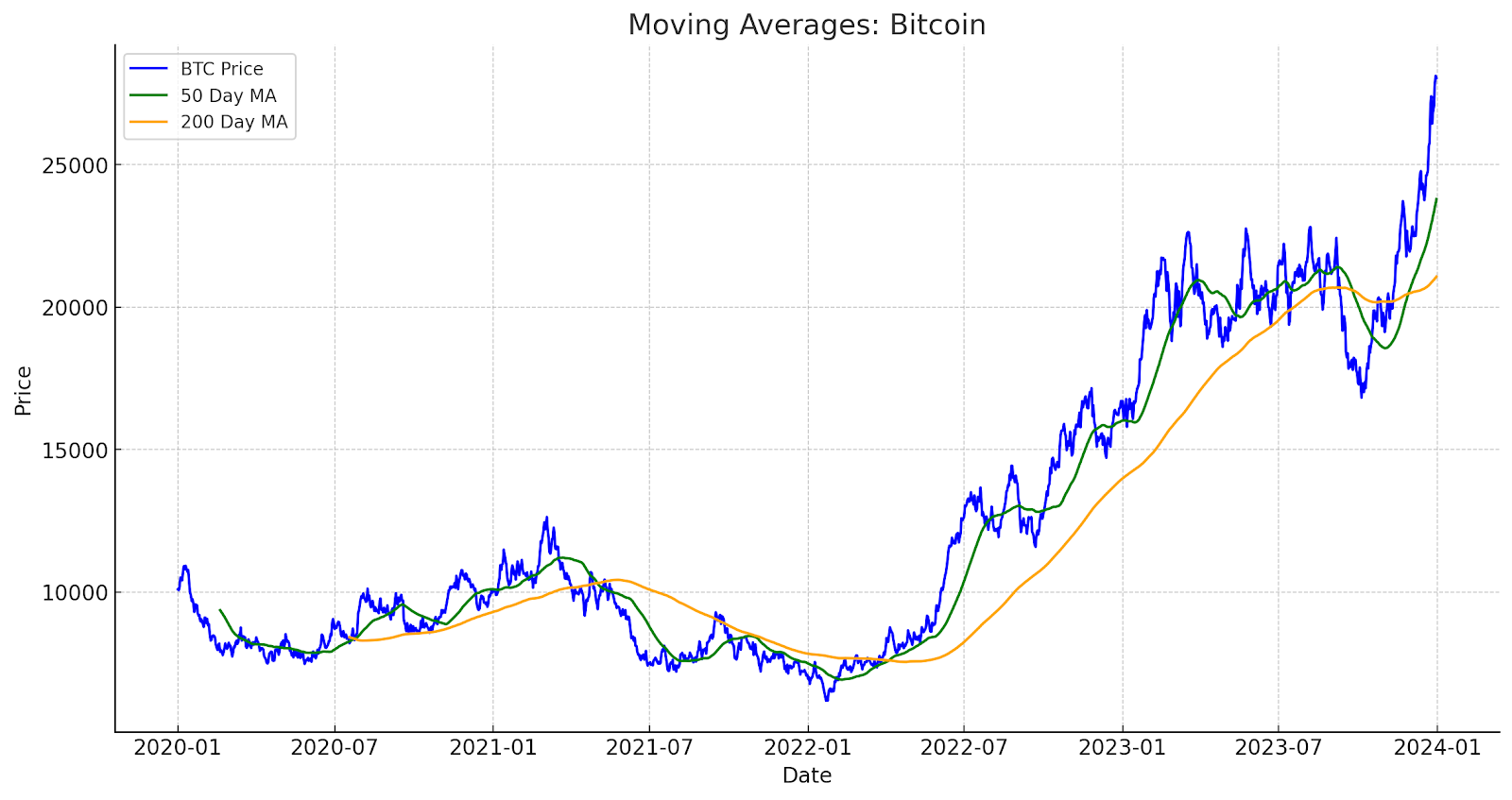

Moving Averages (MA)

Chart displaying the 30-day rolling volatility for Bitcoin and Ethereum.

Moving averages (MA) are a foundational technical analysis tool used to smooth out price fluctuations and identify trends. They calculate the average price of an asset over a specific period (e.g., 50 days, 200 days). By analyzing multiple MAs with different lengths, we can assess historical volatility:StrengthsSimple to calculate and interpret.Identifies trend direction and potential volatility changes.A shorter MA crossing a longer MA (e.g., a 50-day MA crossing above the 200-day MA) can signal increasing volatility, often associated with breakouts or breakdowns.WeaknessesLacks precision in pinpointing exact volatility levels.Slow to react to sudden price changes, potentially missing short-term volatility spikes.Relies on past data, not necessarily predictive of future volatility.

Bollinger Bands (BB)

Bollinger Bands (BB) are a volatility indicator built upon a moving average. They consist of an upper and lower band surrounding a central MA (typically 20-day). The bands widen as volatility increases, indicating larger price deviations from the moving average. Conversely, narrowing bands suggest lower volatility.

Strengths

- Visually appealing and easy to interpret.

- Provides a dynamic range for volatility based on recent price movements.

- Price movements touching or exceeding the bands can signal potential trend reversals or increased volatility.

Weaknesses

- Prone to “whipsaws” during periods of high volatility, where prices repeatedly touch or breach the bands, generating false signals.

- Similar to MAs, it relies on historical data and may not predict future volatility changes.

Standard Deviation (SD)

Standard deviation (SD) is a statistical measure of dispersion from the mean. In historical volatility analysis, it calculates the average deviation of an asset’s price from its average price over a specific period. A higher SD indicates greater price fluctuations and vice versa.

Strengths

- Provides a quantitative measure of volatility, expressed as a percentage.

- Useful for comparing the volatility of different assets with similar price ranges.

Weaknesses

- Ignores the direction of price movements. A large SD can reflect either strong upward or downward trends, not necessarily increased risk.

- Sensitive to outliers – extreme price movements can significantly distort the SD value.

Average True Range (ATR)

The Average True Range (ATR) is a volatility indicator that considers not just closing prices but also the highs and lows within a period. It captures the overall market’s “range” or typical price movement over a chosen timeframe.

Strengths

- Less susceptible to outliers compared to SD.

- Accounts for price gaps that can occur between daily closing prices.

- Useful for identifying periods of expanding or contracting ranges, potentially indicating increased or decreased volatility.

Weaknesses

- Doesn’t provide a directional bias on price movements.

- Similar to MAs and BBs, it is backward-looking and may not predict future volatility shifts.

Historical Volatility Index (VIX)

The CBOE Volatility Index (VIX), often referred to as the “fear gauge,” is a volatility measure specific to the S&P 500 options market. The VIX reflects the market’s expectation of future volatility based on S&P 500 option prices.

Strengths

- A forward-looking indicator, providing insights into investor sentiment regarding future market volatility.

- Widely used by investors to gauge overall market risk and adjust portfolio allocations.

Weaknesses

- Not directly applicable to individual stocks or asset classes outside the S&P 500.

- VIX itself can be volatile, making it challenging to interpret precise

Applications of Historical Volatility Analysis in Crypto

The inherently volatile nature of cryptocurrency markets makes historical volatility (HV) analysis an essential tool for crypto traders. Here’s how HV analysis can be employed for strategic decision-making:

Risk Management

- Identifying Potential Risks: By analyzing historical volatility, traders can gauge the potential price swings of a cryptocurrency. High HV indicates a greater risk of sudden price movements, allowing traders to adjust their position sizes accordingly. For example, during periods of high volatility, a smaller position size helps mitigate potential losses.

- Setting Stop-Loss Orders: HV analysis helps determine appropriate stop-loss levels. Stop-loss orders automatically sell an asset when it reaches a specific price, limiting potential losses. By understanding the asset’s typical price range based on historical volatility, traders can set realistic stop-loss levels that avoid getting triggered by normal price fluctuations.

“65% of cryptocurrency investors use stop-loss orders, which can be informed by historical volatility analysis”

Trend Identification

- Identifying Trend Breakouts: When Bollinger Bands widen, it suggests increasing volatility, potentially signifying a breakout from a trading range. This can be a signal to enter a trade in the direction of the breakout.

- Identifying Trend Reversals: Conversely, narrowing Bollinger Bands indicate decreasing volatility, potentially foreshadowing a trend reversal. This can be a cue to exit a losing position or prepare to short the asset if a downtrend is anticipated.

- Combining with Moving Averages: Using multiple Moving Averages with varying lengths can help identify changes in trend direction. A shorter MA crossing above a longer MA during increasing volatility (wider Bollinger Bands) strengthens a bullish breakout signal.

Mean Reversion

- Identifying Overbought and Oversold Conditions: HV analysis can be used in conjunction with technical indicators like the Relative Strength Index (RSI) to identify overbought or oversold conditions.

When combined with high historical volatility, an RSI reading above 70 might suggest an overbought cryptocurrency ripe for a correction. Conversely, an RSI reading below 30 during low historical volatility might indicate an oversold asset with potential for a rebound.

Note: Mean reversion is a statistical tendency, not a guarantee. Crypto markets are subject to unexpected news and events that can disrupt expected price movements.

Option Trading

Options contracts derive their value partly from the underlying asset’s volatility. Higher historical volatility translates to higher option premiums, as options become more valuable due to the increased chance of significant price movements.

- Implied Volatility vs. Historical Volatility: Options also have implied volatility, which reflects the market’s expectation of future volatility. By comparing historical volatility to implied volatility, traders can potentially identify inefficiencies in option pricing and develop option trading strategies to exploit them.

Limitations and Challenges of Historical Volatility Analysis

Here are some of the key limitations and challenges of historical volatility analysis:

Data Quality and Availability

One of the biggest limitations of historical volatility analysis is the quality and availability of data. Historical volatility analysis requires a large amount of high-quality data, which may not always be available. Additionally, the data may be subject to errors, biases, and inconsistencies, which can affect the accuracy of the analysis.

Model Risk and Assumptions

Historical volatility analysis relies on statistical models and assumptions, which can be flawed or incomplete. For example, the assumption of normality or lognormality of returns may not always hold true, and the model may not capture all the relevant factors that affect volatility.

Market Regime Changes and Non-Stationarity

Historical volatility analysis assumes that the market regime and volatility patterns remain constant over time. However, market regimes can change, and volatility patterns can shift, which can render the analysis invalid.

Overfitting and Curve-Fitting

Historical volatility analysis can be prone to overfitting and curve-fitting, where the model is too complex and fits the noise in the data rather than the underlying patterns. This can result in poor out-of-sample performance and inaccurate predictions.

Recommended reading: Bitcoin Technical Analysis: A Comprehensive Guide

Mitigating the Limitations and Challenges

While these limitations and challenges are significant, there are ways to mitigate them:

Data Quality and Availability

- Use high-quality data sources, such as reputable financial databases or exchanges.

- Clean and preprocess the data to remove errors and inconsistencies.

- Use data augmentation techniques to increase the size and diversity of the dataset.

“90% of cryptocurrency exchanges offer historical data for volatility analysis, making it easier for traders to access the data they need”

Model Risk and Assumptions

- Use robust and flexible models that can capture non-normality and non-stationarity.

- Validate the model using out-of-sample data and walk-forward optimization.

- Use ensemble methods to combine the predictions of multiple models.

Market Regime Changes and Non-Stationarity

- Use regime-switching models that can capture changes in market regimes.

- Use non-parametric methods that do not assume a specific distribution of returns.

- Monitor the performance of the model and re-estimate it regularly to adapt to changes in the market.

Overfitting and Curve-Fitting

- Use regularization techniques, such as L1 and L2 regularization, to prevent overfitting.

- Use cross-validation to evaluate the performance of the model on out-of-sample data.

- Use simple and interpretable models that are less prone to overfitting.

Conclusion

Historical volatility (HV) analysis is an effective instrument for maneuvering through the frequently turbulent waters of the cryptocurrency market. You can uncover trends, obtain important insights into possible hazards, and make well-informed investing decisions by studying the historical price fluctuations of an asset.

Although data quality and model assumptions are two of the constraints of HV analysis, you can greatly improve your research by intentionally addressing these problems with careful data collection and model selection.

")